How Korean stock market is about to get destroyed - The Two Stocks That will eat Korea

KOSPI will tank more, way more - and memory market starts to normalize to pre-2026 levels

You have probably noticed something strange with KOSPI (Korean stock market). One of the best-performing stock markets on the planet this year has started behaving like a meme coin (-9.9% whole country index per day, then +8% next day), lurching up and down by ten percent in a single session, tripping circuit breakers, and yet still sitting on gains that would make a venture capitalist blush.

So let me try to answer the question everyone is actually asking. Are Samsung and SK hynix going to keep going up through 2026 and into 2027, or is this the part of the movie where the music stops?

To get there honestly, we have to look at the data. All of it. Because what happened to the KOSPI this year is not really a story about Korea. It is a story about how the entire global stock market quietly turned a single, boring, commodity component into the most important product in the world.

A melt-up, then the brakes

Start with the index itself, because the numbers are genuinely hard to believe. At the end of 2024 the KOSPI closed at 2,399. In April 2025, during the tariff panic, it briefly traded under 2,294, one of the cheapest moments for Korean equities in years. From that low it did not recover so much as detonate. On June 19, 2026 it printed an intraday high of 9,386, and on June 22 it set a record close of 9,115. That is nearly four times the April 2025 low, and roughly double where it started this year.

Then the same index that had been the envy of the world started shaking. On June 23, the KOSPI fell 9.99 percent in a single day, triggering a circuit breaker that halted trading on the Korea Exchange. The next sessions were a blur of violent swings, a 5.4 percent jump on one day and a 5.8 percent drop with another halt on June 26. By the time the dust settled at the end of that week, the index had given back a chunk of June but was still up around a hundred percent for the year. It was the fifth time in 2026 that the Korea Exchange had frozen trading mid-session, and the second time in a single week, something it had never done before.

A market does not move like this because of Korea’s domestic economy, which is, frankly, sluggish. The won has been weak, hovering near 1,540 to the dollar. Consumer spending is soft. This was never about Korea. It was about what two Korean companies make, and who is suddenly desperate to buy it.

More about how overbought (in terms of technical analysis) the Korean stock market is:

The thing AI actually runs on

Everyone knows artificial intelligence needs chips. Most people picture Nvidia. But an AI accelerator is useless without something to feed it data fast enough, and that something is memory. Specifically, high-bandwidth memory, or HBM, which is ordinary DRAM stacked vertically into towers and wired together through thousands of microscopic channels, then bolted right next to the processor.

Here is the part that broke the market. Each gigabyte of HBM eats roughly three times the wafer capacity of standard DDR5. So as Samsung, SK hynix and Micron shifted their fabs toward HBM to feed the AI build-out, they pulled wafers away from the ordinary memory that goes into your laptop and your phone. The result was a supply shock in a product almost nobody thinks about. DRAM contract prices rose 45 to 50 percent in the fourth quarter of 2025, then a record 90 to 95 percent in the first quarter of 2026, then another 58 to 63 percent in the second quarter. Samsung disclosed that its average memory selling price in the first quarter was about 146 percent higher than its full-year 2025 average. This is not a price increase. It is a regime change.

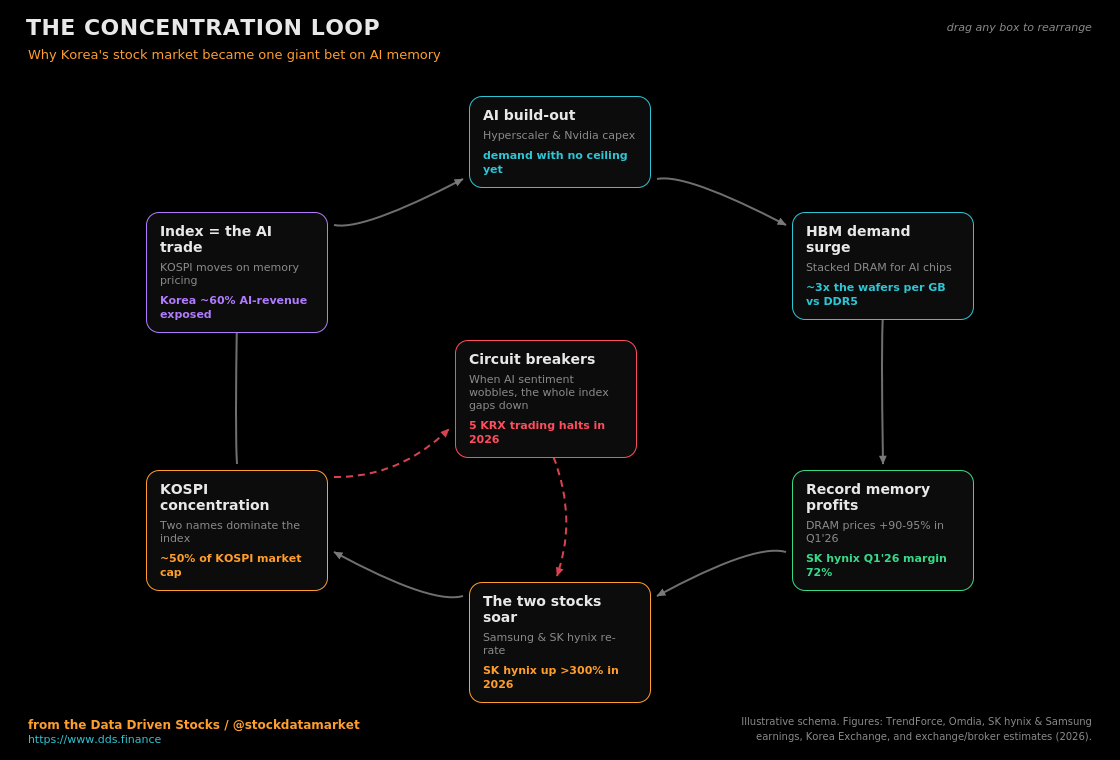

The cleanest way to see why this feeds straight back into the stock market is the loop below. AI capex drives HBM demand, HBM demand drives record memory profits, those profits send the two stocks vertical, the two stocks come to dominate the index, and the index becomes a pure proxy for AI sentiment. When that sentiment wobbles, the whole thing gaps down at once, which is exactly what a circuit breaker is for.

One quarter that beat an entire year

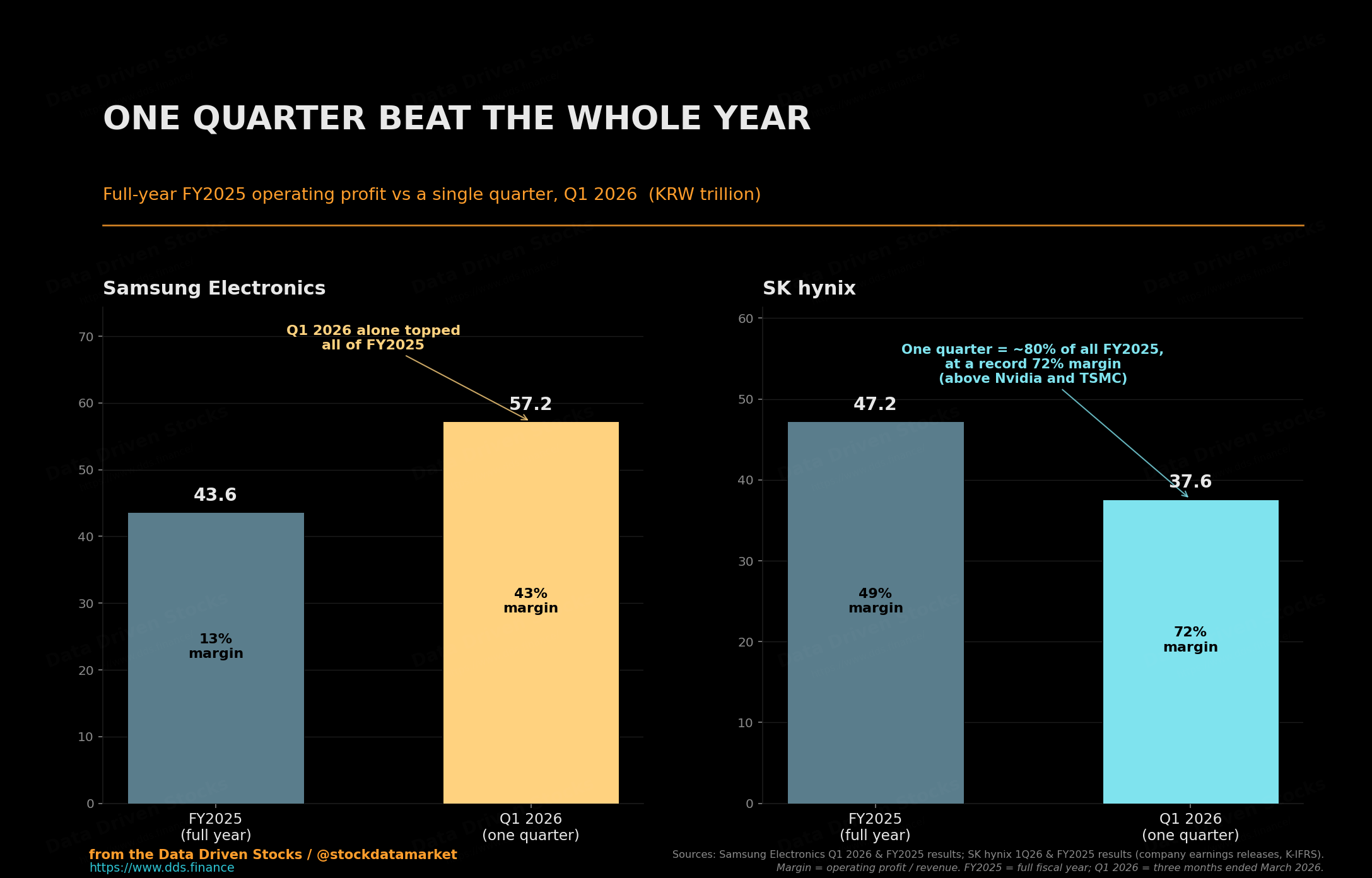

If you want to understand why investors lost their minds, look at a single number. SK hynix earned more operating profit in the first quarter of 2026 than Nvidia did as a share of its revenue. Its operating margin hit 72 percent, an all-time record for the semiconductor manufacturing industry, higher than Nvidia’s roughly 65 percent and higher than TSMC over the same stretch. Revenue was 52.58 trillion won, the first time the company had ever crossed 50 trillion in a quarter, up 198 percent from a year earlier. Net income was 40.3 trillion won, a 77 percent net margin. For a business that lost money two years ago, this is surreal.

Samsung’s first quarter was, in its own way, even more startling. The company posted 57.2 trillion won of operating profit in three months. That single quarter exceeded its entire operating profit for all of 2025, which was 43.6 trillion won. Almost all of it came from the chip division, where Samsung also became the first company to mass-ship the next generation, HBM4, in February, aimed at Nvidia’s Vera Rubin platform. Within four months of launch, Samsung’s HBM4 had passed a billion dollars in sales.

There is a reason this matters more than a normal earnings beat. Memory makers have enormous operating leverage, which is a polite way of saying that when prices rise, almost all of the extra revenue falls straight to the bottom line, and when prices fall, the same thing happens in reverse. Goldman Sachs estimates Korean corporate earnings will grow about 300 percent in 2026, which it calls the strongest annual profit expansion in any Asian market since the recovery from the 1999 financial crisis. That is the engine under the index.

Two companies, two completely different bets

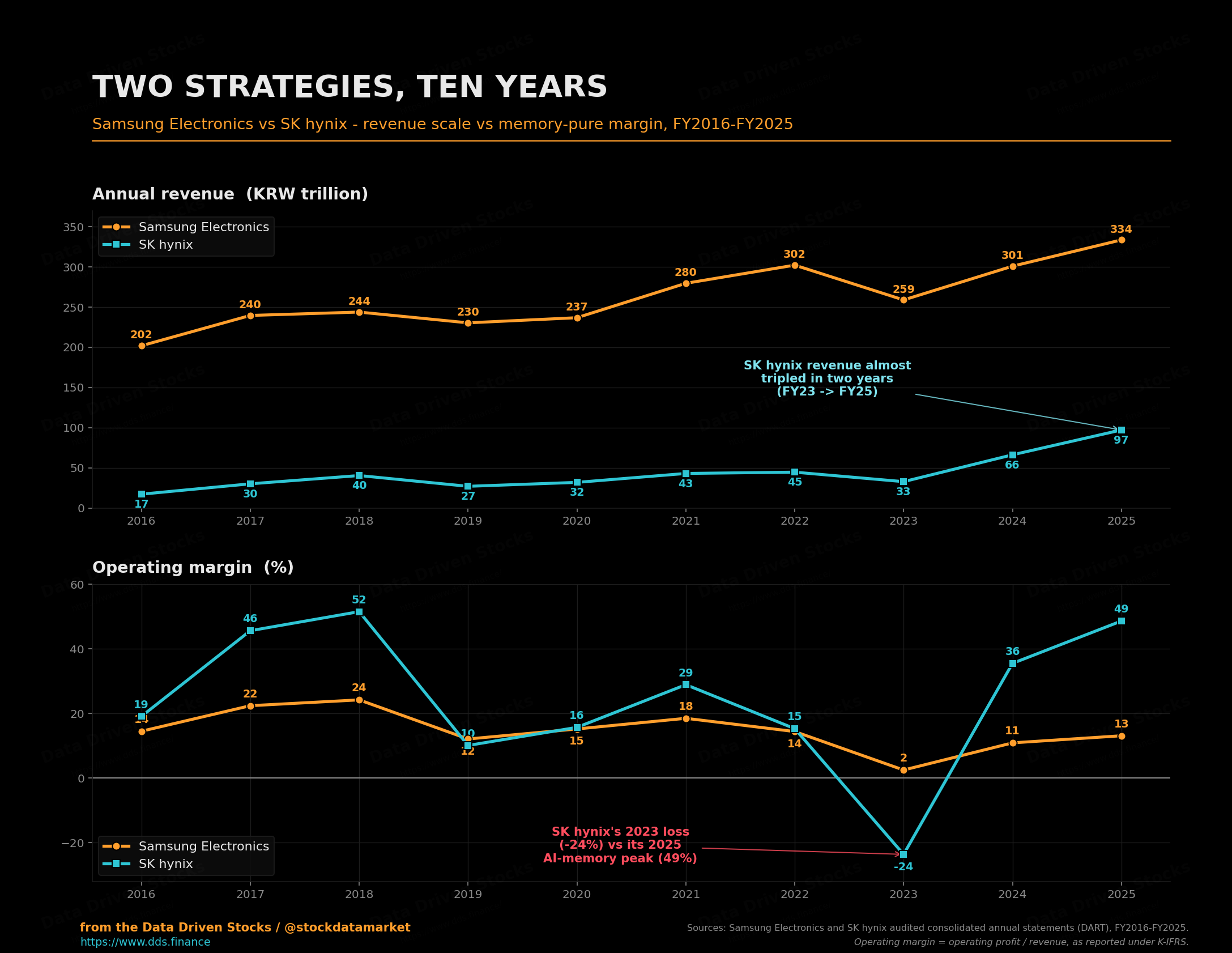

It is tempting to lump Samsung and SK hynix together as “the Korean chip stocks,” but they have spent the last decade making opposite wagers, and 2026 is the year both paid off at the same time.

Samsung is a sprawling giant. Its annual revenue has hovered between about 200 and 334 trillion won for ten years, anchored by phones, displays, appliances and foundry work in addition to memory. That diversification kept its operating margin relatively stable, mostly in the teens and low twenties, and crucially kept it out of the red even in 2023 when memory cratered. SK hynix made the opposite choice. It is essentially a pure-play memory company, which is why its results read like a seismograph. Its margin hit about 52 percent in 2018, collapsed to negative 24 percent in 2023 when DRAM prices crashed, and then roared back to 49 percent in 2025. Its revenue nearly tripled in two years, from 32.8 trillion won in 2023 to 97.1 trillion in 2025.

That difference is the whole investment debate in one chart. SK hynix is the cleaner, sharper bet on AI memory, with nothing to dilute the upside and nothing to cushion the downside. Samsung is the hedged version, with real businesses that can offset a memory downturn but also dilute a memory boom. In a year like 2026, the pure bet wins by a mile, which is why SK hynix is up well over 300 percent in 2026 against roughly 190 percent for Samsung, and why, on June 22, SK hynix briefly overtook Samsung to become the most valuable company in Korea for the first time in more than 25 years. The crown lasted exactly one day before both stocks fell more than 12 percent and Samsung took it back.

Two crowns, two companies

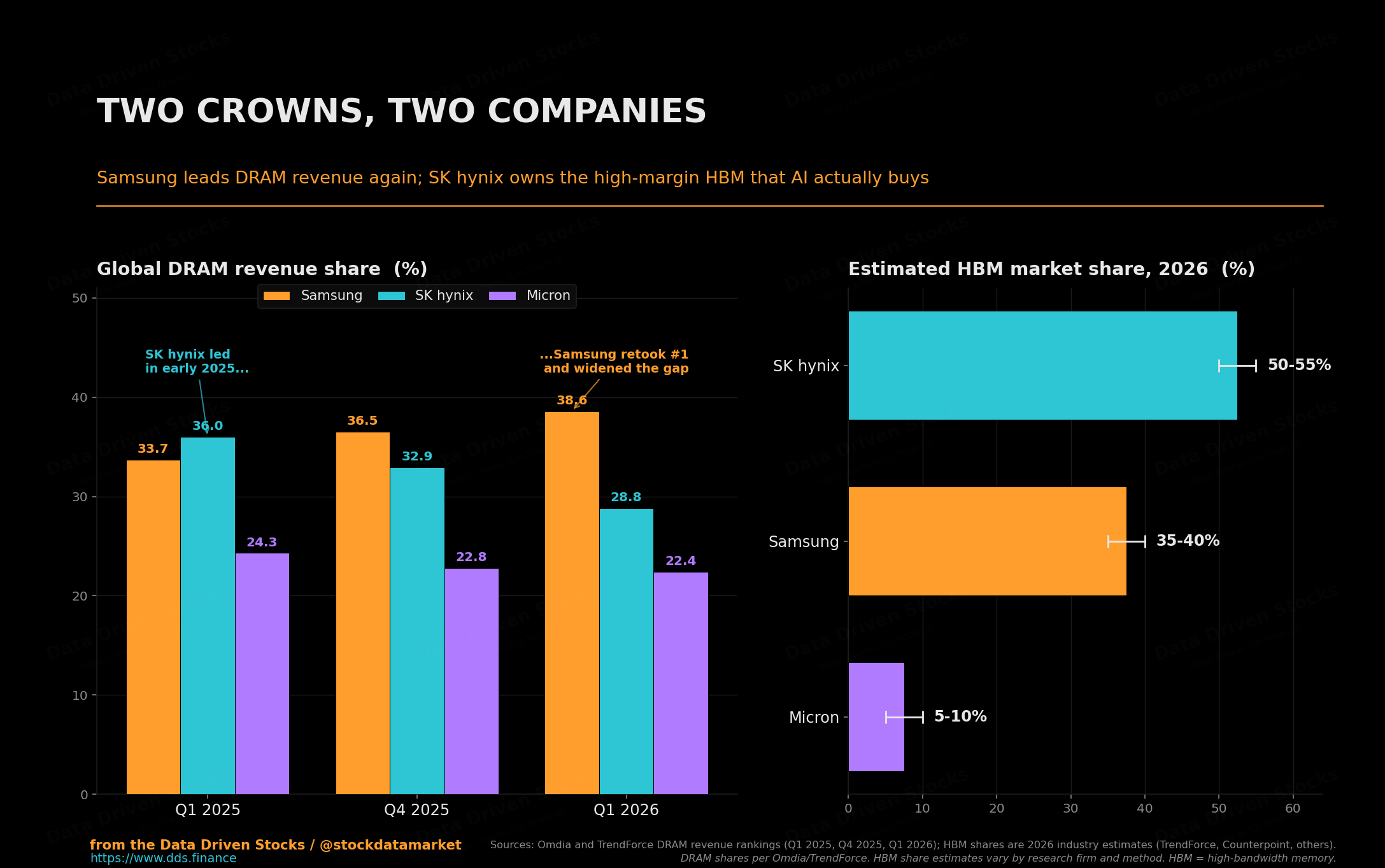

Here is the wrinkle that most headlines miss. Samsung and SK hynix are not even winning the same race. On overall DRAM revenue, Samsung is back on top. It led DRAM with a 38.6 percent share in the first quarter of 2026, ahead of SK hynix at 28.8 percent and Micron at 22.4 percent, after retaking the lead from SK hynix late in 2025. Global DRAM revenue hit a record 97 billion dollars in that quarter alone.

But the crown that AI actually cares about is HBM, and there SK hynix is the clear leader. Estimates of its exact share vary by source and method, ranging from the low fifties to above sixty percent for 2025, but every tally puts it first by a wide margin, with most pointing to roughly 50 to 55 percent of the market in 2026, Samsung around 35 to 40 percent, and Micron in the single digits to low teens. SK hynix also holds an estimated two-thirds of the orders for Nvidia’s next-generation Rubin platform. So Samsung wins the volume crown and SK hynix wins the margin crown, which is why the same quarter can hand the revenue lead to one company and the profitability lead to the other.

There is a fascinating tell buried in SK hynix’s behavior. In late June it began delaying the conversion of some HBM3E production lines, choosing instead to keep churning out conventional DDR5. Why would the HBM leader slow its HBM ramp? Because with DDR5 operating margins now approaching 90 percent, ordinary memory has become so profitable, per unit of wafer, that it rivals the company’s flagship product. When the most boring chip in your catalog is printing 90 percent margins, you do not rush to retool the factory.

Somebody has to pay for all this

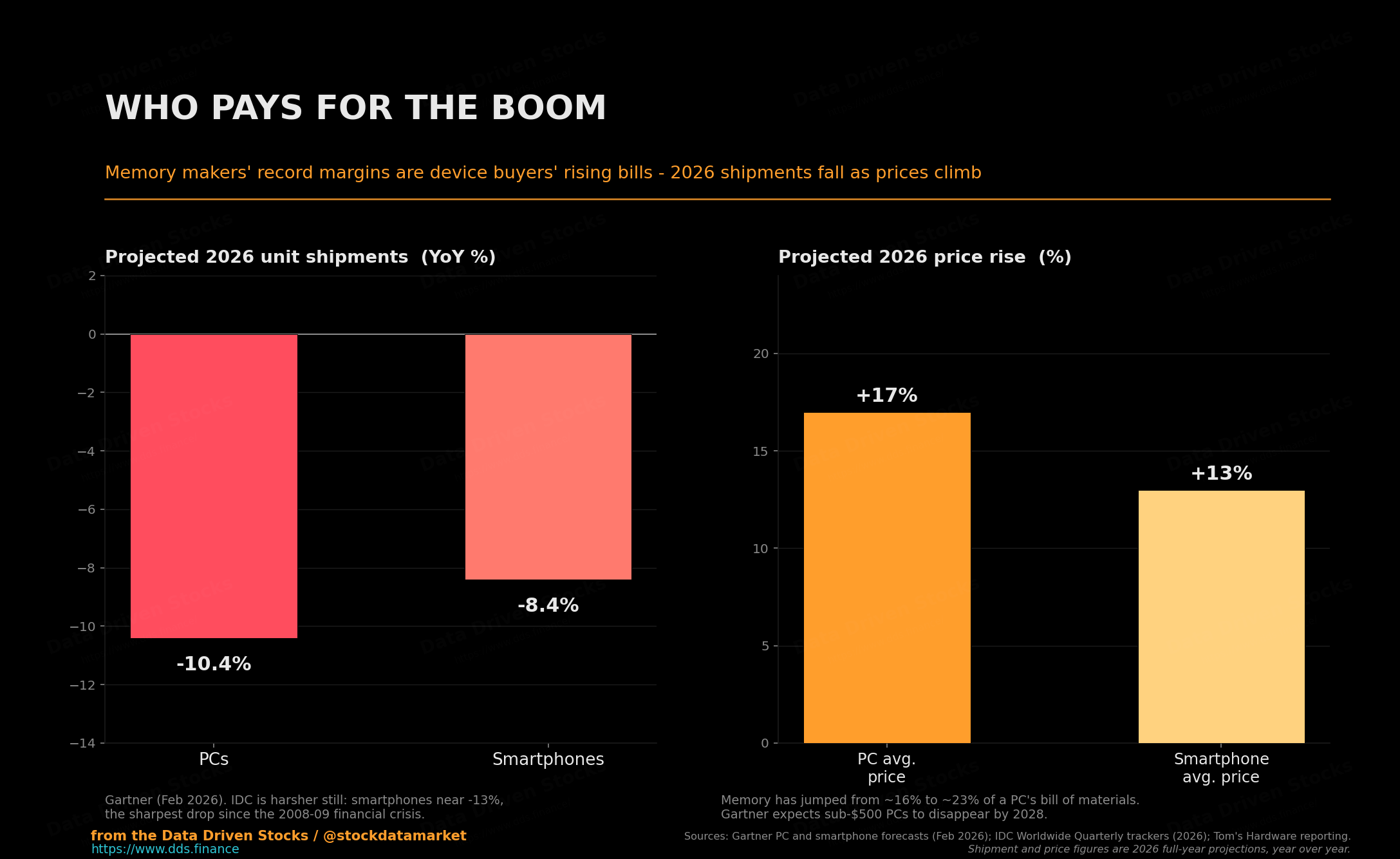

Record margins for three companies are record costs for everyone else. The bill for the AI memory boom is landing squarely on the people who buy laptops and phones, and the numbers are brutal.

Gartner projects that PC shipments will fall about 10.4 percent in 2026 and smartphone shipments about 8.4 percent, while average PC prices rise around 17 percent and smartphone prices around 13 percent. IDC is even gloomier, putting the smartphone decline near 13 percent, which would be the sharpest drop since the 2008 financial crisis. Memory has jumped from roughly 16 percent of a PC’s bill of materials to about 23 percent, and Gartner expects the sub-500-dollar PC to essentially disappear by 2028. The distortion has gotten so extreme that, by one Counterpoint reading, the spot price of old DDR4 memory briefly exceeded the contract price of cutting-edge HBM3e.

This is the uncomfortable truth under the rally. What is profit for Samsung, SK hynix and Micron is cost for Dell, HP, Apple and you. It is also, oddly, a problem for Samsung itself. Its mobile division, which has to buy memory like everyone else, has warned it could post its first-ever annual loss, squeezed by the same component inflation its own chip division is causing. Samsung is the rare company that is simultaneously the biggest winner and a genuine victim of the thing it created.

Why the index keeps convulsing

Now we can explain the circuit breakers. Samsung and SK hynix together have grown to more than half of the entire KOSPI’s market capitalization, up from around a quarter of the index just two years ago. By most accounts the two of them have driven roughly 70 percent of the index’s 2026 gains. When two stocks are that large a share of an index, the index stops being a market and becomes a leveraged bet on those two names, which in turn are a leveraged bet on AI memory pricing, which in turn is a leveraged bet on global AI capex sentiment.

So when sentiment cracked on June 23, after a sharp AI selloff in the United States dragged the Nasdaq down 2.2 percent and the Philadelphia Semiconductor Index down 8 percent, there was nothing to cushion the KOSPI. Billions of dollars of foreign capital left in a single session, with foreigners selling a net 5.8 trillion won of Korean shares while local retail investors bought a record 11.1 trillion won, betting the AI story stayed intact. The selling was amplified by a peculiar local feature of this rally: the explosion of leveraged single-stock ETFs that let retail investors make double-or-nothing bets on SK hynix, some of which had traded at enormous premiums to their underlying value before unwinding violently. The breadth had been a warning all along. As one strategist put it, the index rose 12 percent over six sessions in early June while breadth was negative every single day, which is exactly what happens when a handful of names are the entire market.

So will they keep going up?

This is the question, and the honest answer is that the bull case and the bear case are both unusually strong, which is precisely why the stock keeps moving ten percent a day.

The bull case rests on supply, and it is formidable. This is not a hype cycle running on promises; it is a physical shortage running on wafers. Goldman Sachs raised its 2026 DRAM supply-demand gap estimate to about 4.9 percent and called it the most severe memory shortage in fifteen years. New fabs take eighteen months or more to reach volume, so the only near-term way to add supply is incremental process upgrades inside existing factories. Barclays expects bit demand to keep accelerating past 35 percent growth in 2027 while wafer capacity lags well behind. SK hynix’s chairman has said the wafer shortage could persist to 2030, and the company is locking in multi-year visibility through long-term agreements, including a three-year DDR5 deal with Microsoft and roughly 20 percent HBM3e price increases secured for 2026. In June, Nvidia’s Jensen Huang appeared alongside SK Group’s chairman in Seoul to declare the AI build-out would continue and to call SK hynix Nvidia’s largest memory partner. Goldman maintained its KOSPI target of 12,000, about 36 percent above where the index sat, even after the June crash, calling that drop a valuation correction rather than a break in the demand story. Looking further out, Goldman has sketched a 2028 in which Samsung and SK hynix together earn more than 1,000 trillion won in annual operating profit. If even half of that lands, today’s prices are not expensive.

The bear case rests on everything else. Memory is the most cyclical business in technology, and every supercycle in its history has ended with overcapacity, because the cure for high prices is high prices. The same fabs being built to relieve the shortage in 2027 and 2028 are the seeds of the next glut. Valuations have already re-rated enormously, so a lot of good news is priced in, and the AI memory trade is now a three-supplier race rather than a two-horse one, with both Samsung and Micron certified for Nvidia’s HBM4. If Samsung gains HBM share faster than expected, SK hynix could see its premium multiple compress back toward ordinary memory math. The macro backdrop turned hostile almost overnight, with one major bank flipping to forecast three Federal Reserve rate hikes in 2026 on worsening inflation. The consumer side of memory is already in a recession of its own making. And the concentration itself is a structural fragility: a market that is half two stocks will keep tripping its own circuit breakers on any bad day in AI, regardless of fundamentals. Counterpoint pegs the earliest real inflection in the shortage at late 2027, and Intel’s chief executive has bluntly said there is no relief until 2028, which is bullish for prices but also a reminder of how far out the cycle’s turn now sits.

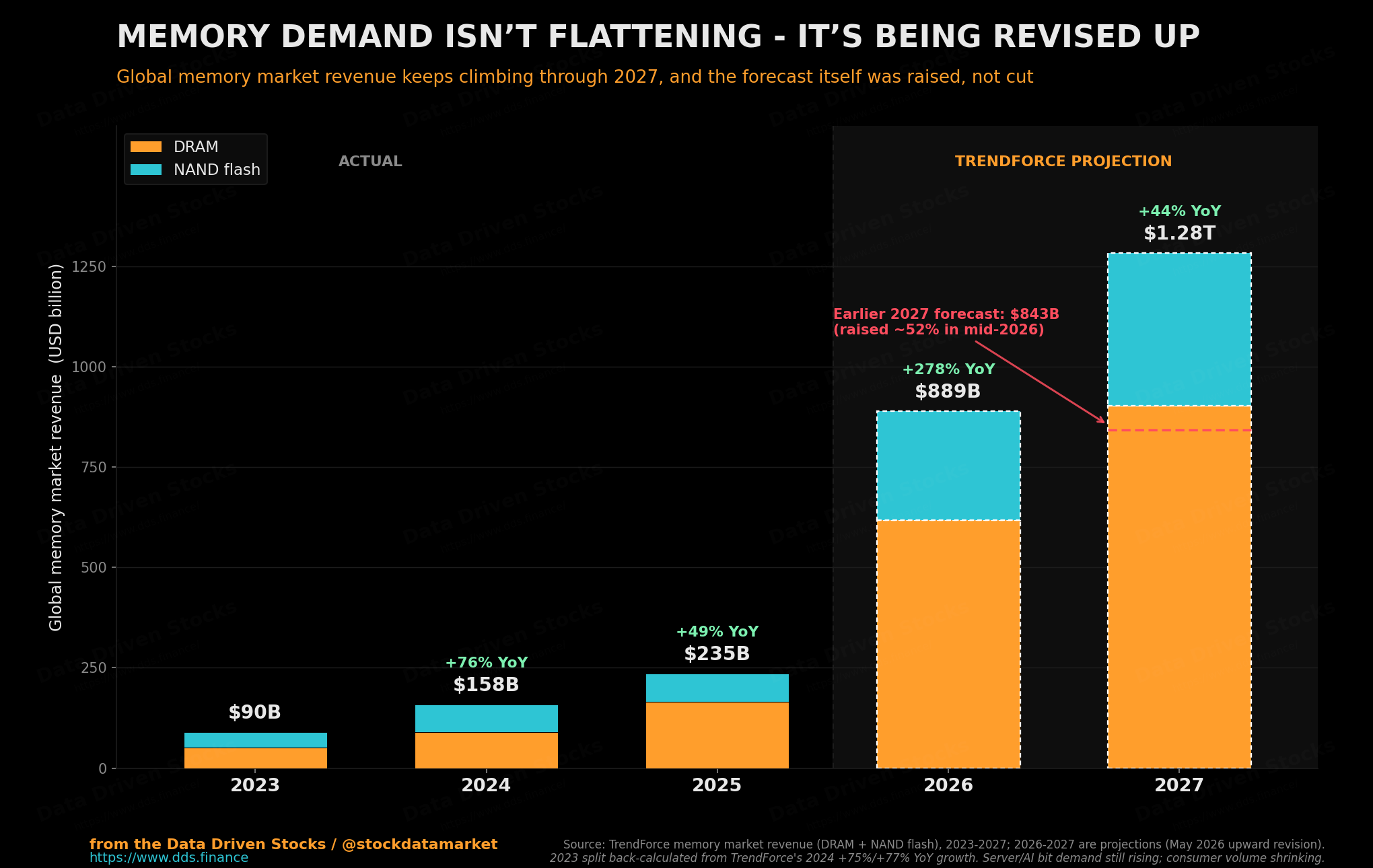

There is one more number the bulls tend to skip past, and it is buried in the demand forecasts themselves. The market did something genuinely explosive in 2026: TrendForce projects total memory revenue more than tripling in a single year, from around 235 billion dollars in 2025 to roughly 889 billion in 2026. The catch is what comes next. The same forecasters have the market growing only about 44 percent in 2027, which is slower than 2024, at roughly 76 percent, and no faster than 2025. So the shape is not a demand curve bending ever upward. It is a one-year spike followed by a sharp normalization, a deceleration from nearly 280 percent growth straight down to the low forties. The absolute market still gets bigger, and physical bit demand is still rising, but the rate of growth, which is the thing that actually re-rated these stocks, is already projected to stall back toward its pre-boom pace as soon as next year.

The verdict

Put it together and a picture emerges that is more useful than a simple yes or no. The earnings are real, not promotional, and the shortage driving them is physical and likely to persist through at least 2027. On that basis, the upward bias in Samsung and SK hynix earnings is probably intact into 2027, even as the breakneck pace of growth is already projected to cool, and the most credible analysts still see meaningful upside in the shares from here. That is the part of the bull case that is hard to argue with.

But the stocks and the index they dominate are now a single, highly leveraged expression of global AI sentiment, with almost no diversification left to absorb a shock. So even if the destination is higher, the path will be the opposite of smooth. Expect more days like June 23, where nothing fundamental changes and the index still falls ten percent because a server farm announcement in California spooked everyone at once. The supercycle is not obviously over. What ended on June 22 was the illusion that a market this concentrated could keep going straight up without occasionally slamming into its own brakes.

If you are watching the open in Seoul right now, that is the frame to hold. The question is no longer whether AI needs memory. It clearly does, more than the world can currently make. The question is whether you can stomach owning the most volatile expression of that fact, in a market that has quietly become two stocks wearing a trench coat. The data says the boom has room to run. It also says the ride will try to throw you off.

Sources

Korea Exchange and Yahoo Finance, KOSPI Composite Index and Samsung Electronics (005930.KS) and SK hynix (000660.KS) daily price data, 2024 to June 2026. Federal Reserve Bank of St. Louis (FRED), South Korean won to US dollar exchange rate (DEXKOUS).

SK hynix, FY2025 and first-quarter 2026 earnings releases (revenue, operating profit, margin, net income, HBM revenue mix). Samsung Electronics, FY2025 and first-quarter 2026 earnings releases (revenue, operating profit, Device Solutions division, HBM4, capital expenditure).

TrendForce, DRAM and HBM industry analyses, 2025 to 2026, including first-quarter 2026 DRAM industry revenue and rankings, DRAM contract price increases, HBM market-share estimates, and the Samsung 146 percent average selling price disclosure. Omdia, first-quarter 2026 DRAM revenue rankings (Samsung 38.6 percent, SK hynix 28.8 percent, Micron 22.4 percent) and record quarterly DRAM revenue. Counterpoint Research, DRAM and HBM market-share and shortage-inflection commentary, including SK hynix’s HBM revenue lead. HBM share figures vary across research firms and methods and are presented here as estimates.

CNBC, reporting on the KOSPI’s 2026 rally, Goldman Sachs targets, foreign investor flows, and index concentration (May and June 2026). Goldman Sachs Research, “Korea’s Stock Market Is Forecast to Set Fresh Highs” and subsequent target revisions, including the 12,000 KOSPI target, 300 percent Korean earnings growth forecast, the 4.9 percent DRAM supply-demand gap, and the 2028 combined operating-profit projection. The Asia Business Daily and Seoul Economic Daily, Korean-market coverage of DRAM leadership and long-term earnings outlooks. Manulife Investment Management, KOSPI concentration estimates. BTIG and KB Financial Group, market-breadth and concentration commentary.

TechTimes, reporting on SK hynix overtaking Samsung, the June 23 circuit breaker and AI selloff, the DDR5-over-HBM4 line decision, and Federal Reserve rate-path revisions. Gartner and IDC, 2026 PC and smartphone shipment and pricing forecasts and memory bill-of-materials estimates. Tom’s Hardware, real-world DRAM pricing. Barclays, memory bit-demand and wafer-capacity growth forecasts. Nvidia and SK Group, June 2026 Seoul briefing remarks by Jensen Huang and Chey Tae-won.

We'll see what happens after SK Hynix ADR :)