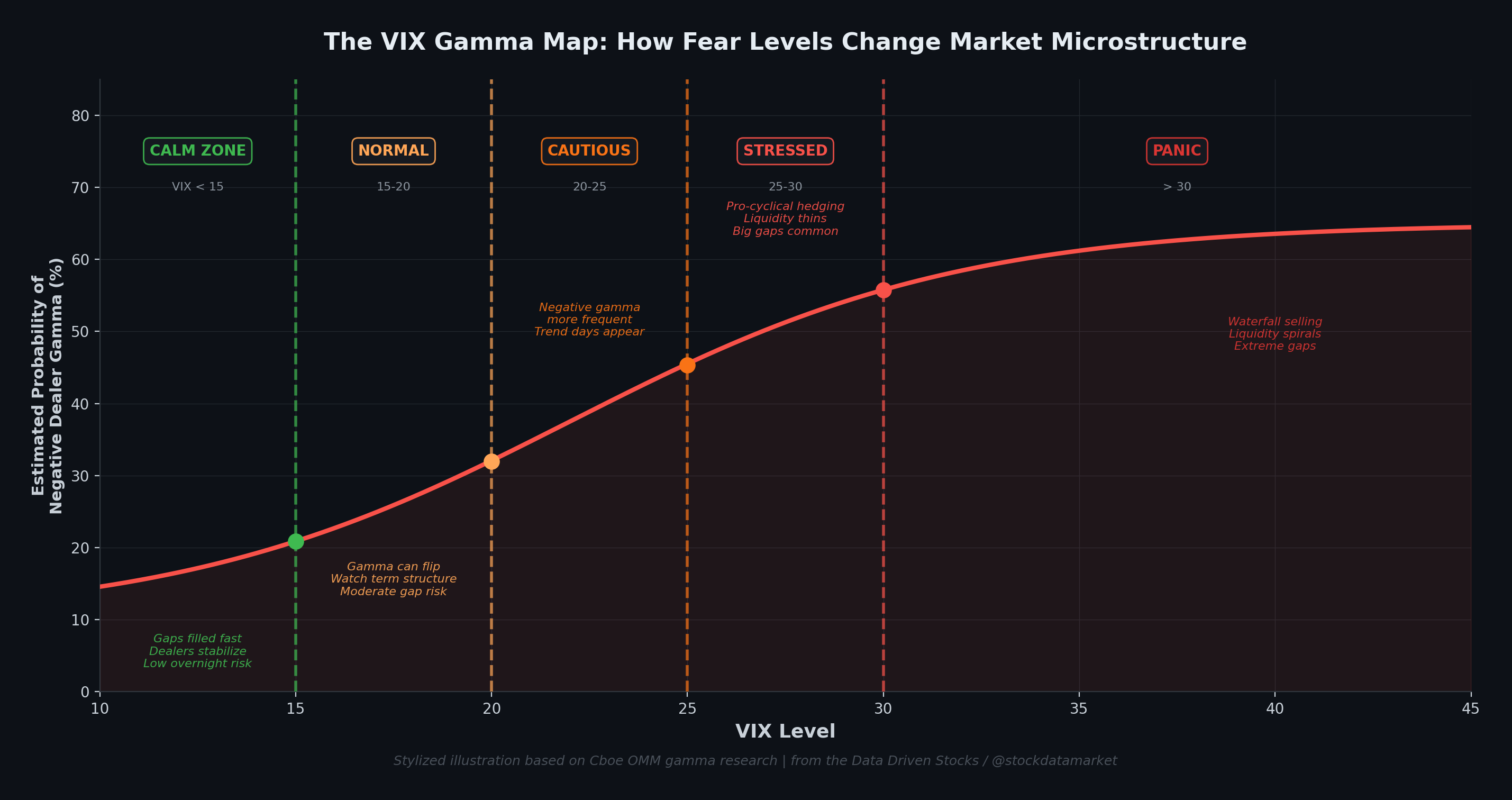

Why the S&P 500 Sometimes Gaps Up - And Sometimes Doesn’t

The VIX tells you more than you think about what happens at the open, midday, and close

Sometimes you see that the S&P 500 gaps down after a major draw down. But sometimes you see it does go down sharply near the close, only for the market to open…