US Inflation Just Broke 4% - and the Oil Price Is Falling on a Ceasefire That Hasn’t Been Signed

The May 2026 CPI and PPI reports, the Hormuz oil shock, the 23-year-low inventories underneath it, and where prices actually go from here.

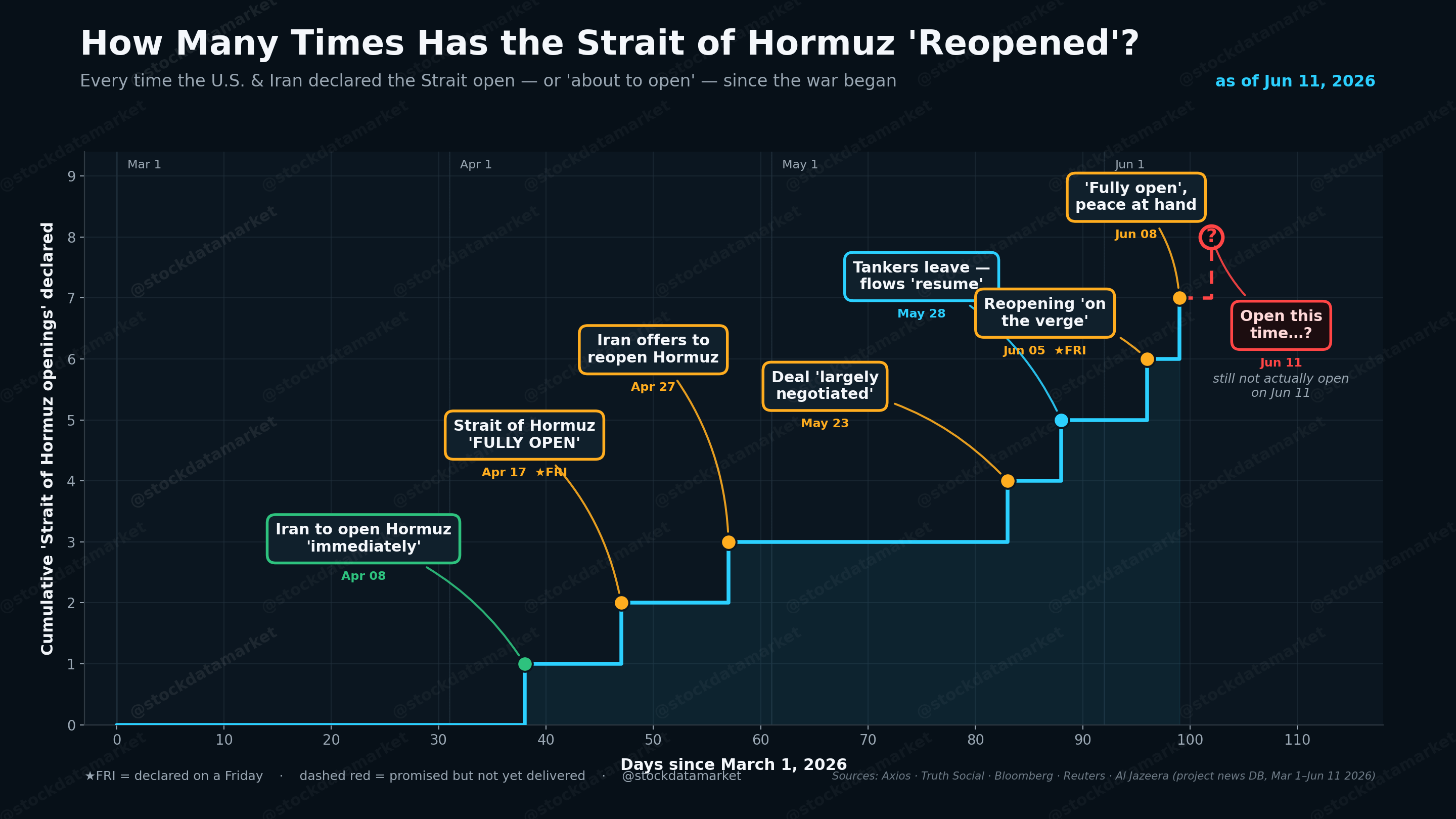

So another peace deal with Iran came today. We even had another Strait of Hormuz opening. But inflation is going up and up and up and up!