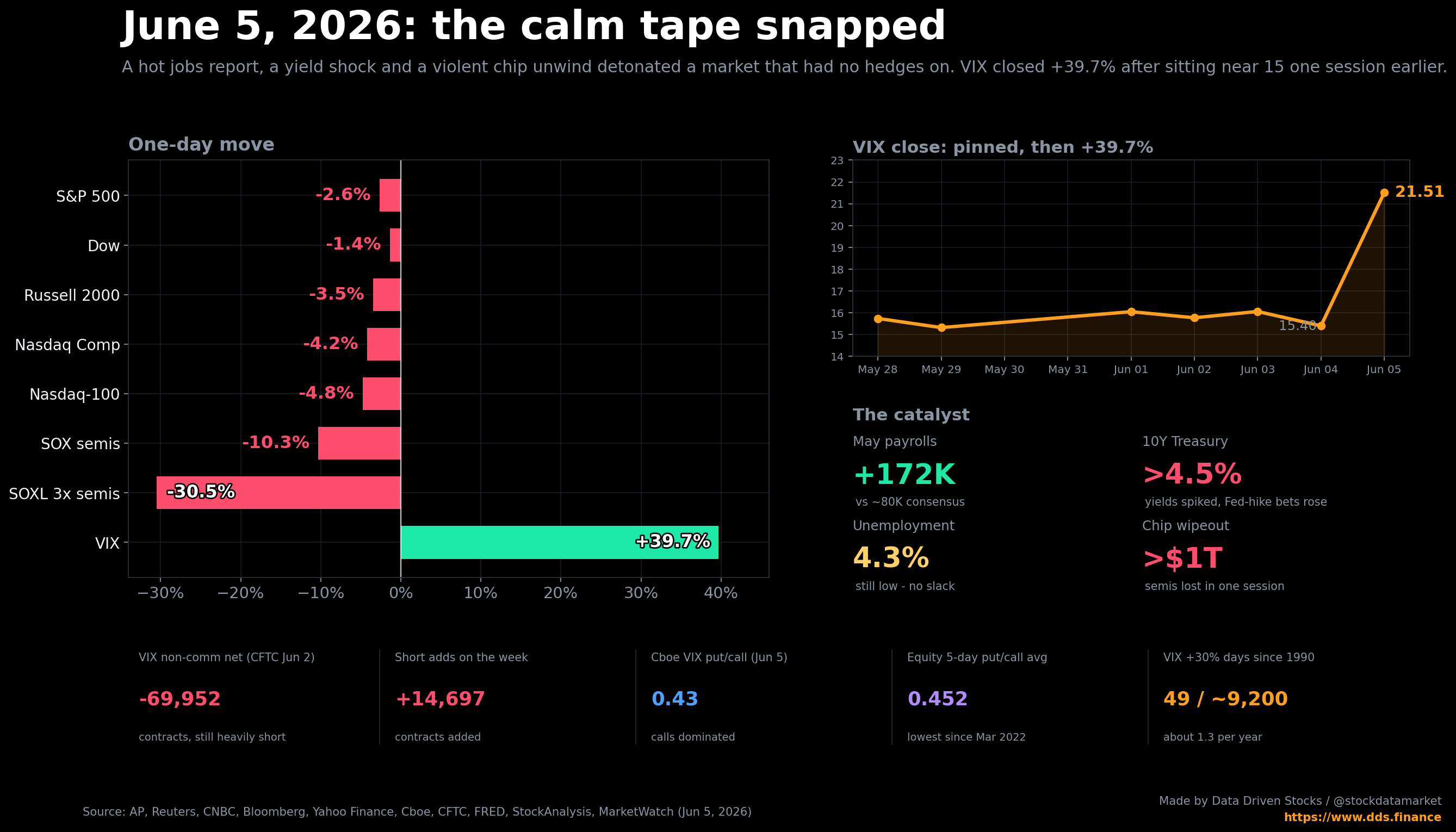

The Volatility Bomb Nobody Hedged: Why the Market Crashed on Friday, June 5, 2026 - and Why I Bought VIX Calls Two Days Early. Then after a S&P 500 -2.64%, Nasdaq -4.18%, VIX +39.7%

A hot jobs print, a yield shock and a violent chip unwind lit the fuse. But the real story is a market that spent weeks selling volatility into the calm, and then got squeezed the moment it mattered.