The VIX: When Wall Street Starts Sweating (Part 2) - How to actually trade the fear gauge (without confusing it for a stock)

Now for Part 2: everyone sees VIX on CNBC… then tries to “buy VIX” like it’s Apple. Yeah, about that.

Part 1 was the “what even is VIX?” episode: a number backed out of SPX option prices that tells you how jumpy the market expects the next ~30 days to be. Not direction. Just how spicy the ride could get.

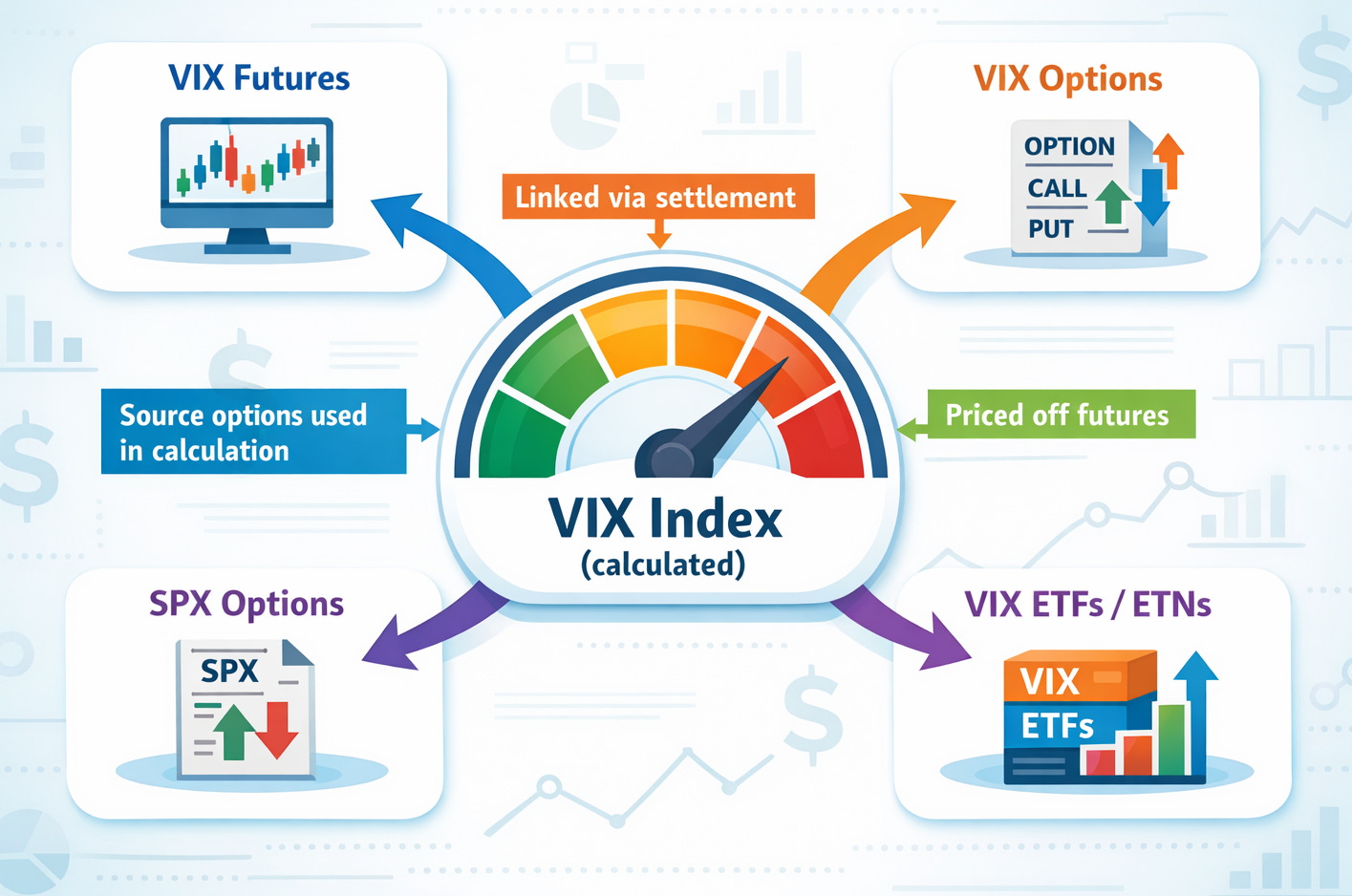

1) You can’t buy the speedometer (so you trade the parts around it)

The VIX is an index. It’s calculated from real‑time prices of options on the S&P 500 (SPX), and it’s designed to represent the market’s consensus view of expected 30‑day volatility.

That’s why you can’t trade the VIX directly: there’s no share of “VIX” sitting on an exchange you can take delivery of. Even the issuers of popular volatility ETFs spell it out in plain English: “The VIX is not directly investable.”

So how do people “trade VIX” in the real world?

They trade instruments whose value is linked to volatility expectations, mainly:

VIX futures, which are literally futures on where the VIX is expected to be at a future date.

VIX options, which are options on volatility (but with their own rules, settlement quirks, and pricing behavior).

VIX‑linked ETPs (ETFs/ETNs) like VIXY, UVXY, SVXY, VIXM, VXX, which mostly hold a rolling basket of VIX futures rather than “spot VIX.”

And if you want the “closest” practical thing to trading the VIX calculation itself, you go to the source: SPX (or XSP) options. Because VIX is built from those options in the first place.

2) VIX futures: renting fear by the month (and why they don’t mirror spot VIX)

A VIX future is the market’s best guess of what the VIX will be at that contract’s expiration. Cboe says it directly: VIX futures reflect the market’s estimate of the value of the VIX Index on various future expiration dates.

That sentence is the whole game.

Spot VIX is “what implied vol is priced at right now.”

A VIX future is “what implied vol might be then.”

So the two can move together, but they’re not glued together tick‑for‑tick.

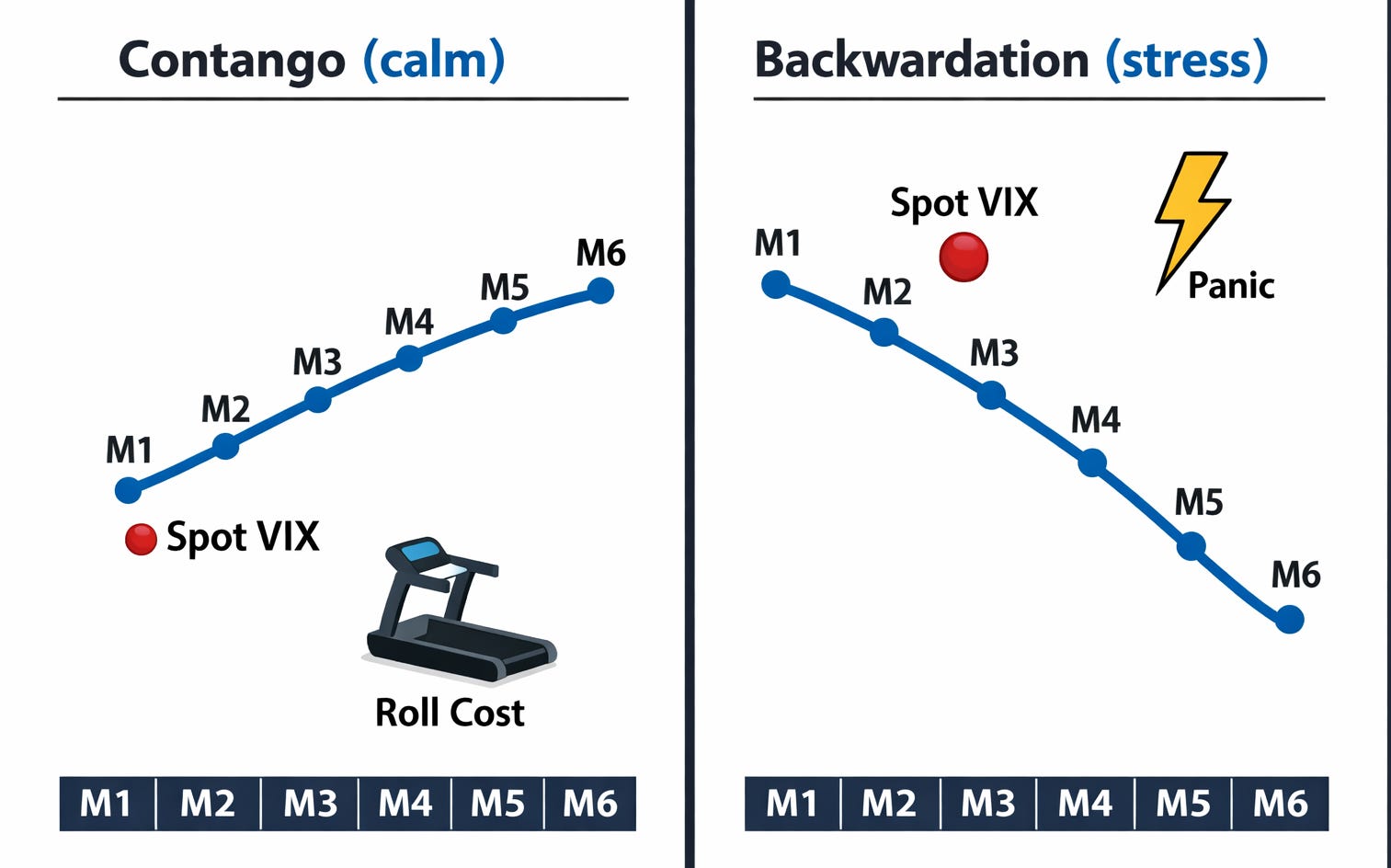

The key relationship: futures converge, they don’t copy

As expiration approaches, the future has less “time” to disagree with reality. So it tends to converge toward the value used at settlement (more on that settlement value in a second).

In calm regimes you often see something like:

Spot VIX is 14

Front‑month VIX future is 16

Second‑month is 17

Nothing “wrong” here. This is just the market pricing that volatility can normalize upward and also embedding a volatility risk premium (insurance isn’t free). Cboe explicitly talks about both the mean‑reversion tendency of volatility and the long‑run premium embedded in option‑implied volatility versus realized volatility.

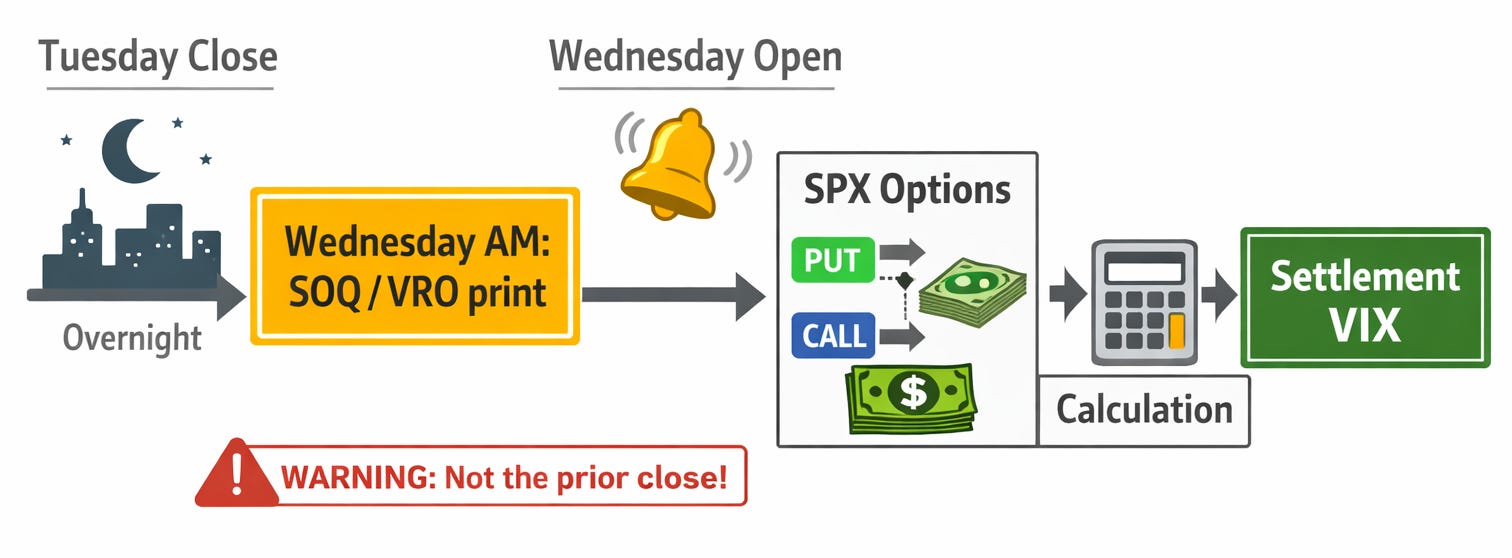

The expiration mechanism: the Wednesday that decides everything

VIX futures and VIX options don’t settle like stocks. The final settlement value is calculated on the morning of expiration (usually a Wednesday) via a Special Opening Quotation (SOQ) of the VIX Index.

Here’s the important nuance: that SOQ is built from the opening prices of the SPX options used in the VIX calculation, which is why the Cboe calls the settlement process “tradable” (because you can trade the SPX options used in that settlement print).

The expiration date itself is also special. For the standard monthly VX contract, the final settlement date is tied to the SPX option calendar: it’s typically a Wednesday 30 days before the third Friday of the following month (the SPX option cycle logic).

If you’ve ever seen weird price action around “VIX settlement,” that’s why. It’s not conspiracy. It’s a specific, mechanical print based on a slice of SPX options at the open.

Practical implication: you can be right on spot VIX and still be wrong on the future

Because the future is pricing expected VIX at its expiration, you can get situations where spot VIX spikes 10% today… but the front‑month future barely shrugs because the market thinks the spike is temporary and will fade before settlement.

That one idea basically explains 90% of why VIX ETPs confuse people.

3) VIX ETFs: “VIX cosplay” (what they actually hold, and why the moves aren’t 1:1)

Let’s say this cleanly: most “VIX ETFs” do not track spot VIX.

They track an index of VIX futures.

And that one difference is why your brain says “VIX up 10% = my ETF up 10%,” but your brokerage says “lol no.”

The baseline product: VIXY is not “VIX”, it’s “short‑term VIX futures”

ProShares VIX Short‑Term Futures ETF (VIXY) is explicit about its benchmark: it seeks results (before fees/expenses) that match the S&P 500 VIX Short‑Term Futures Index.

It also says the quiet part out loud: the ETF is not benchmarked to spot VIX, and VIX futures can be expected to perform very differently from VIX—so the ETF can be expected to perform very differently from VIX, on a daily basis and over time.

Now what is that index, mechanically?

S&P describes it as using the next two near‑term VIX futures contracts and rolling from the front month into the second month daily in equal fractional amounts, maintaining a constant one‑month rolling long position in first and second month VIX futures.

So when you buy VIXY, you’re basically buying a rolling blend of front‑month and second‑month VIX futures.

Leveraged version: UVXY turns the volume knob to 1.5x… daily

UVXY seeks 1.5x the daily performance of the same short‑term VIX futures index.

The word “daily” is not decoration. ProShares explicitly warns that returns over periods longer than one day can deviate (sometimes a lot) from the daily target because of compounding and volatility.

That’s why leveraged volatility products are famous for being tactical tools, not “buy and forget” investments. ProShares is blunt: these funds are generally intended for short‑term investment horizons.

Inverse version: SVXY is basically “short short‑term VIX futures”… but at -0.5x

SVXY seeks -0.5x of the daily performance of the S&P 500 VIX Short‑Term Futures Index.

Again, it’s daily, and it’s futures, not spot VIX. So it’s not “short VIX,” it’s “short a rolling futures index,” which is a different animal.

Mid‑term version: VIXM is slower, smoother, and less “panic‑beta”

VIXM tracks the S&P 500 VIX Mid‑Term Futures Index, which maintains a weighted average of about five months to expiration.

And ProShares even describes the mechanics: the index rolls daily, keeping exposure across the 4th through 7th month VIX futures while maintaining that ~5‑month average maturity.

Translation: VIXM is typically less sensitive to today’s volatility pop than a short‑term product, because it’s sitting further out on the curve.

Why the moves aren’t 1:1 (and why “VIX up 10%” can mean “ETF up 0.7%”)

There are three big reasons, and they stack.

First, the ETFs track futures, and futures are the market’s view of VIX at the futures’ expiration dates. So a spot move today might not change the market’s view of what VIX will be at settlement very much.

Second, the index is a rolling blend of two futures. Even if the front contract moves, the second contract might move less, and the portfolio return becomes a weighted average.

Third, rolling itself has a cost when the curve is in contango (later futures priced higher than nearer futures). Both S&P’s description of daily rolling and ProShares’ own warnings spell out that VIX futures indexes have historically reflected significant costs associated with rolling futures on a daily basis, and those costs can consistently reduce returns over time.

This is the “VIX ETF decay” everyone memes about. It’s not magic. It’s the roll.

If you want a clean mental model, think of it like this:

Spot VIX is a weather report.

VIX futures are the forecast for next month’s weather report.

VIX ETFs are a subscription service that keeps buying next month’s forecast every day… and pays a spread for doing so.

4) SPX/XSP straddles: trading volatility without saying “VIX” out loud

If VIX comes from SPX options, then buying/selling SPX options is basically trading volatility at the source.

That’s why “I want to trade VIX” often becomes “I’m trading implied volatility via SPX/XSP structures.”

Long straddle = I expect that VIX will go up. Short straddle = I expect that VIX will go down.

Why SPX and XSP are popular volatility instruments

Cboe highlights that SPX options have cash settlement and European exercise, among other features.

XSP (Mini‑SPX) also emphasizes cash settlement and European exercise, which removes early assignment risk, and it’s smaller in notional than SPX.

If you’ve ever had a short SPY option exercised early for no reason other than “dividend vibes,” you understand why traders like European‑style index options.

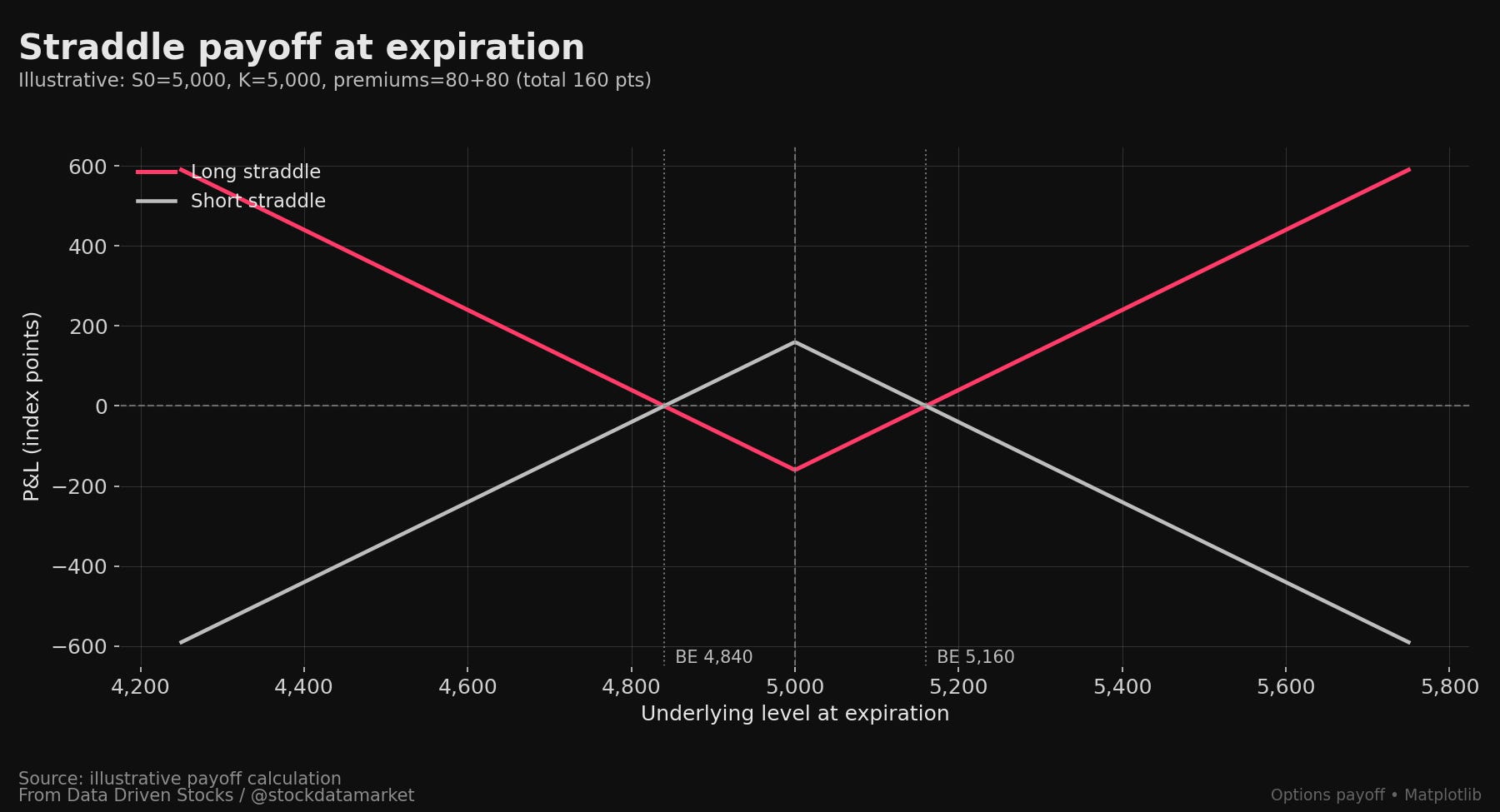

The “long straddle”: the classic “long vol” trade

A long straddle is buying a call and buying a put with the same strike and expiration. OptionsEducation defines it exactly that way, and the payoff idea is simple: you want a big move in either direction.

This is the purest “I think volatility is underpriced” retail‑friendly trade.

It’s also the purest “theta is eating my lunch” trade.

Because if the market doesn’t move enough, both options bleed time value.

Strategy vibe: long straddles tend to make sense into known catalysts (CPI, Fed, earnings season for single names, etc.) when you believe realized movement will beat implied pricing. The win condition is not “up” or “down.” It’s “bigger than the market priced in.”

The “short straddle”: being the insurance company

A short straddle is selling both a call and a put at the same strike and expiration. That’s the definition Investopedia gives, and the key point is the intent: profit when the underlying doesn’t move much, because you keep the premium.

But this is not a cute trade. Short straddles can have substantial risk if the underlying moves sharply.

Strategy vibe: this is a “sell vol when it’s overpriced” trade, often used when implied volatility is high and you expect it to mean‑revert lower. That idea lines up with Cboe’s discussion of volatility mean‑reversion and the volatility risk premium (implied often above realized).

If you take one thing here: long straddle = long volatility, short straddle = short volatility. You’re not predicting direction. You’re predicting how much and how pricey the insurance should be.

5) VIX options: cash‑settled fear (wide spreads, weird pricing, and “ITM but still down”)

Yes, you can trade VIX options.

And yes, people get absolutely cooked because they assume they behave like SPY options.

They don’t.

VIX options settle to the SOQ (not the close), and it happens on expiration morning

Cboe explains that volatility derivatives (including VIX options) settle via a Special Opening Quotation of the VIX on the morning of expiration (usually Wednesday).

So the thing that matters at expiration is not “what VIX closed at Tuesday,” it’s the settlement print built from the opening SPX options used in that calculation.

VIX options are European‑style and priced off VIX futures

Cboe’s margin manual explicitly notes that VIX options have European‑style exercise and that pricing is based on the corresponding VIX futures contract.

That’s the second big reason people get confused: VIX options are not “options on spot VIX.” They’re effectively options on the forward (the future), which itself is an expectation of where VIX will be at settlement.

Why VIX options feel expensive (and why spreads can look ugly)

When volatility is high, people desperately want convexity. Everyone wants insurance at the same time. That tends to lift option premiums.

Cboe also warns these products are complex and the risk of loss can be substantial.

And in real markets, bid/ask spreads often widen when things get hectic. Even if a product is “liquid,” panic pricing is still panic pricing.

The “ITM but still lost money” example (this is real math)

Say you buy a VIX put.

You’re right directionally: volatility falls.

You’re even “right” at settlement: your put finishes in the money.

You can still lose if you overpaid.

Example with round numbers:

You buy a VIX 25 put for 7.00 points (so you pay 7.00 premium).

At expiration, the settlement value prints 22.

Your intrinsic value is 25 − 22 = 3.

Your P&L is 3 − 7 = -4.

You were “ITM.” You still lost.

That’s not a VIX thing. That’s just options. Premiums embed implied volatility, time, and demand. When the demand and implied volatility collapse, the option can deflate faster than spot moves help you. And because VIX options are priced off the future, you can even be right about spot VIX and still not get paid the way you expected.

6) Why Wall Street shorts VIX: selling insurance (until the hurricane)

This is where the “why is everyone short vol?” question gets spicy.

Cboe describes the “risk premium yield” idea plainly: over long periods, expected volatility implied by SPX option prices has tended to trade at a premium versus subsequent realized volatility. That gap is basically what option sellers are harvesting.

Add in another structural tailwind: VIX futures indexes can have persistent roll costs (especially in contango), which ProShares says can consistently reduce returns over time for long exposure.

That combo is the “short vol carry trade” in one sentence:

Sell volatility, collect premium, let time and term structure work for you.

It’s often a very good strategy… until it isn’t.

Because volatility is mean‑reverting, but it’s also jumpy. It doesn’t slowly climb the stairs. It takes the elevator. Cboe explicitly calls out mean‑reversion as a key driver of the VIX futures term structure, and that’s exactly why short‑vol can feel like free money most days… and then violently reverse when perceived risk explodes.

So yes, institutions short vol regularly.

And yes, the graveyard is full of “it works until it doesn’t” short‑vol stories.

7) A practical VIX playbook: long calm, short panic, respect the calendar

This is not financial advice. This is the mental model traders actually use.

7.1) Long the calm: when VIX is low, it can pop fast

When implied volatility is cheap, you’re basically buying insurance when nobody wants it.

The reason this can work is that volatility is not symmetric. Panic reprices faster than calm. And volatility tends to mean‑revert, which Cboe explicitly highlights.

The cleanest “long vol” expressions are usually convex structures: calls on VIX futures, long VIX call spreads, long SPX straddles/strangles, or even just “long gamma” via options.

But the cost is real: time decay is always on, and if nothing happens you bleed.

7.2) Fade the panic: when VIX is high and catalysts fade, it often mean‑reverts down

When volatility spikes, insurance gets expensive.

Often the move that caused the spike passes, realized volatility cools, and implied volatility comes back down toward its long‑run average. Again, Cboe directly discusses mean‑reversion in volatility.

That’s the logic behind short‑vol trades: sell rich insurance after the fire, not before.

But the caveat is brutal: sometimes the catalyst isn’t “a one‑day scare.” Sometimes it’s “a regime change.” In those scenarios, shorting volatility too early is how traders learn humility.

7.3) The fine print: expiration and decay are not “details,” they’re the entire business model

This is the part that wrecks new traders.

Short‑dated VIX futures and VIX‑futures‑based ETFs can lose value rapidly when the curve is in contango, because the product is constantly rolling into more expensive contracts and then watching them converge. S&P describes the daily roll mechanism in the index, and ProShares explicitly says rolling costs can consistently reduce returns over time.

Leveraged versions add daily compounding risk on top, which ProShares warns can cause returns over longer periods to deviate significantly from the daily target.

Options add their own calendar tax: theta goes exponential near expiration, and vega can collapse right when you think you’re “right.” With VIX options specifically, remember they’re European‑style and priced off the future, and settlement is a SOQ print on Wednesday morning.

If you treat VIX products like long‑term holdings, you’re not investing.

You’re paying rent.