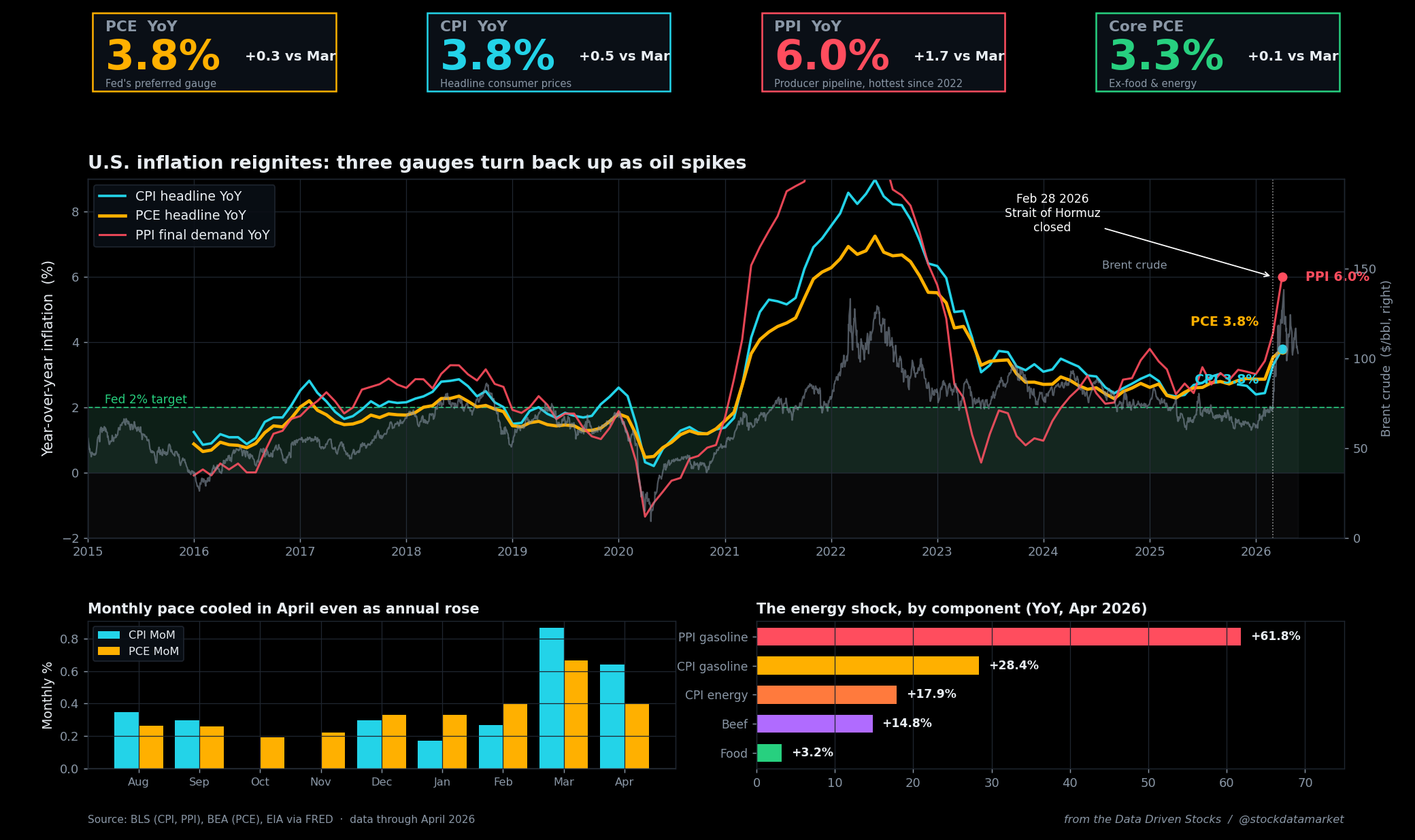

The Strait That Broke the Disinflation: How a 21-Mile Chokepoint Dragged U.S. Inflation Back to 3.8%

The Fed thought it had this beaten. Then a war closed the Strait of Hormuz, oil doubled, and every inflation gauge in America turned back up at once. Here’s the data - and where it goes next.