The Second Wave Just Hit Europe - And The Oil Isn’t Done

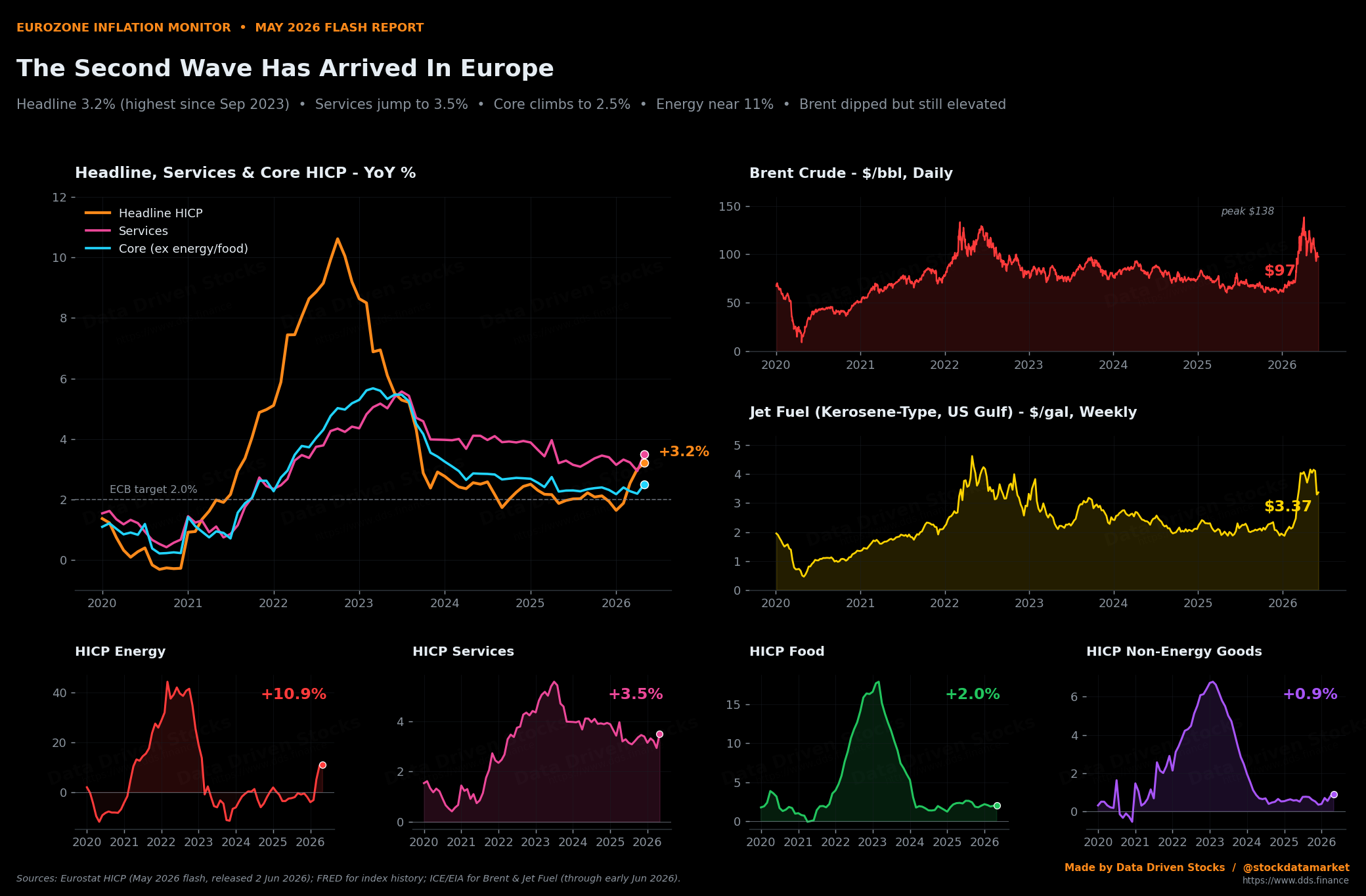

The May inflation report is the one that should worry the ECB. Not because of energy - that was the first wave. Because of what energy did to everything else.

Eurozone inflation monitor, May 2026 flash report. Headline 3.2% (highest since September 2023), services jumping to 3.5%, core climbing to 2.5%, energy near 11% - while Brent crude dipped from its A…

Continue reading this post for free, courtesy of Data Driven Stocks.