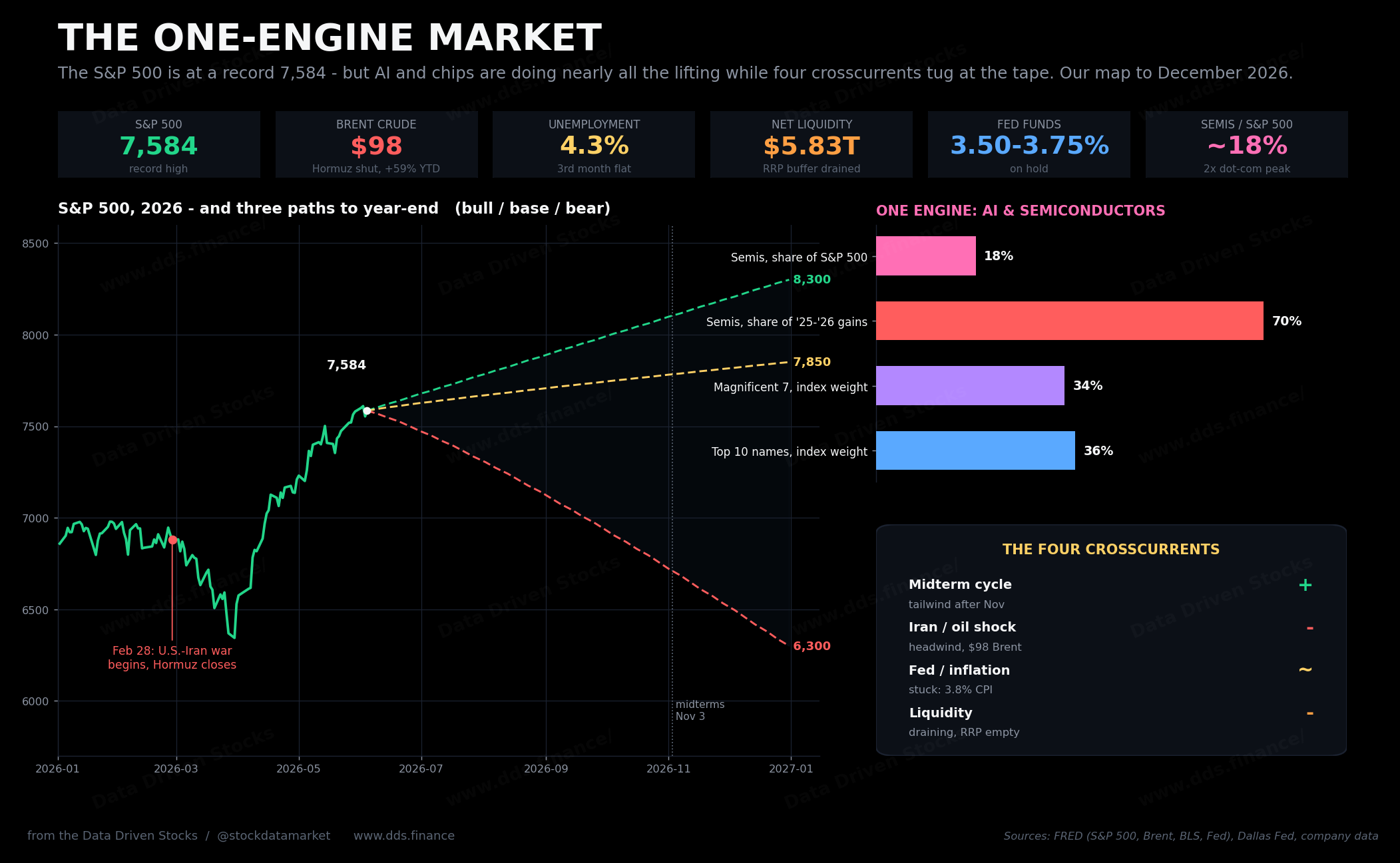

The S&P 500 Is at 7,400 and Running on One Engine. Here’s the Market Map to December 2026.

Midterms say buy the dip. Tehran says hedge it. The Fed says wait. And a single trade - AI and chips - is holding up the whole tape. Here’s how the next seven months actually break (or break apart).