The RAM Crisis Is Real - But Not Where Everyone Thinks

Everyone is screaming about a “RAM shortage.” The data says something more interesting: there isn’t one crisis. There are four. And only some of them are physics.

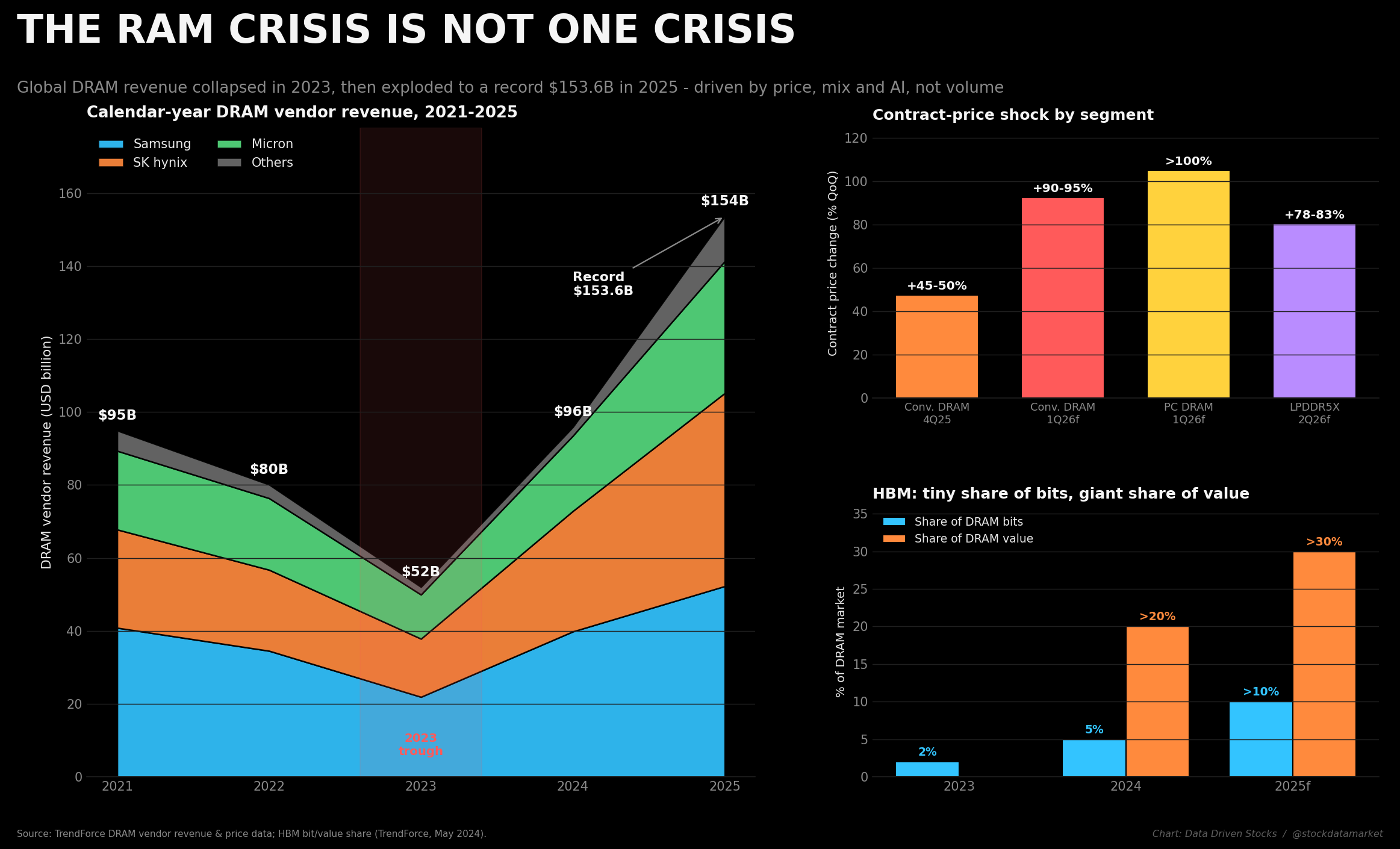

Global DRAM revenue cratered to $52B in 2023, then climbed to roughly $153.6B in 2025 (summing TrendForce’s quarterly vendor-revenue tables; other trackers range from about $129B to $166B). The rebou…

Continue reading this post for free, courtesy of Data Driven Stocks.