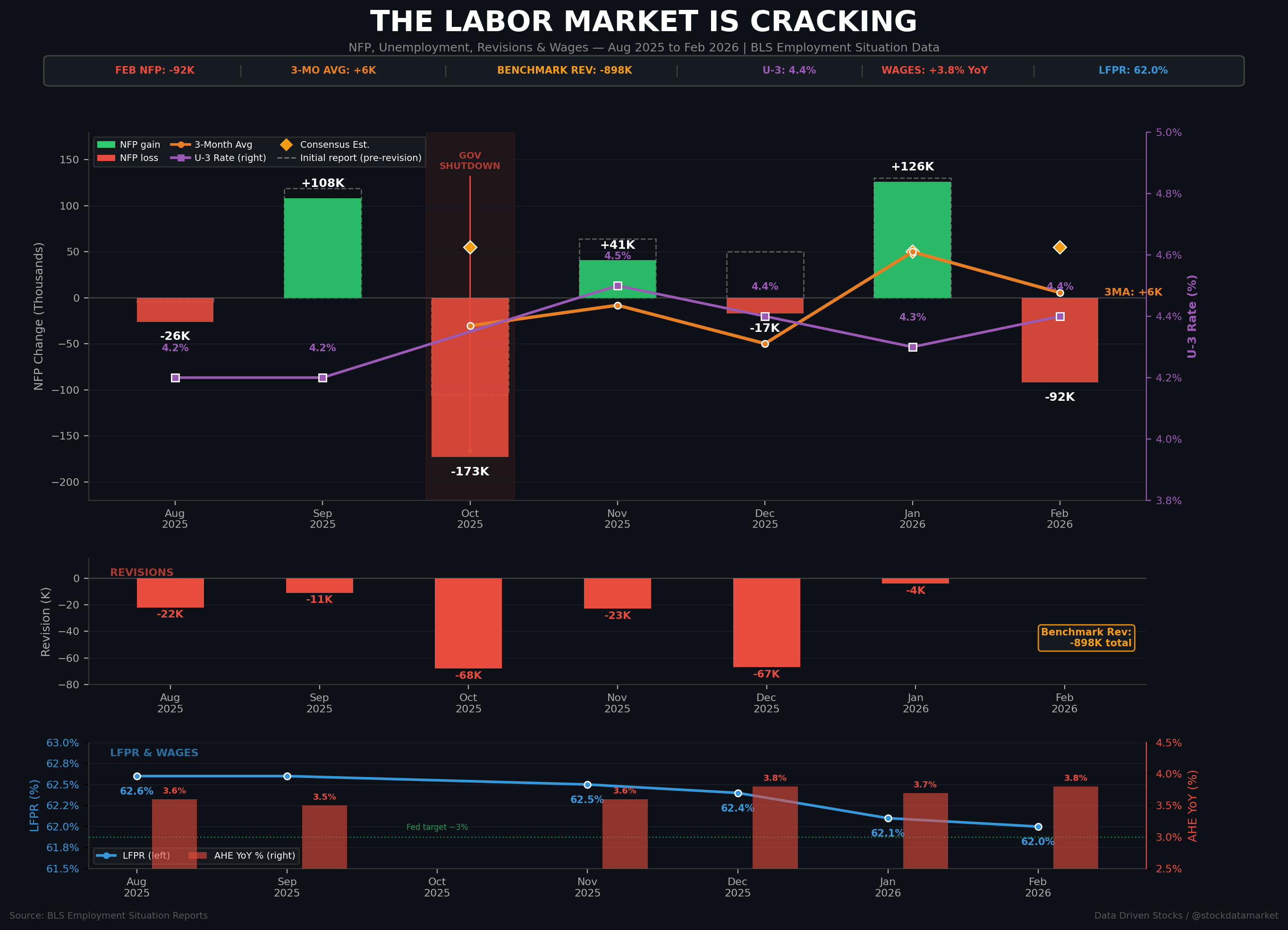

The Labor Market Is Getting Weaker and Weaker Under the Hood

The headline was bad. The details were worse. And the revisions? Don’t even get us started.

On March 6, the Bureau of Labor Statistics dropped the February 2026 Employment Situation report, and it confirmed what anyone paying close attention already suspect…