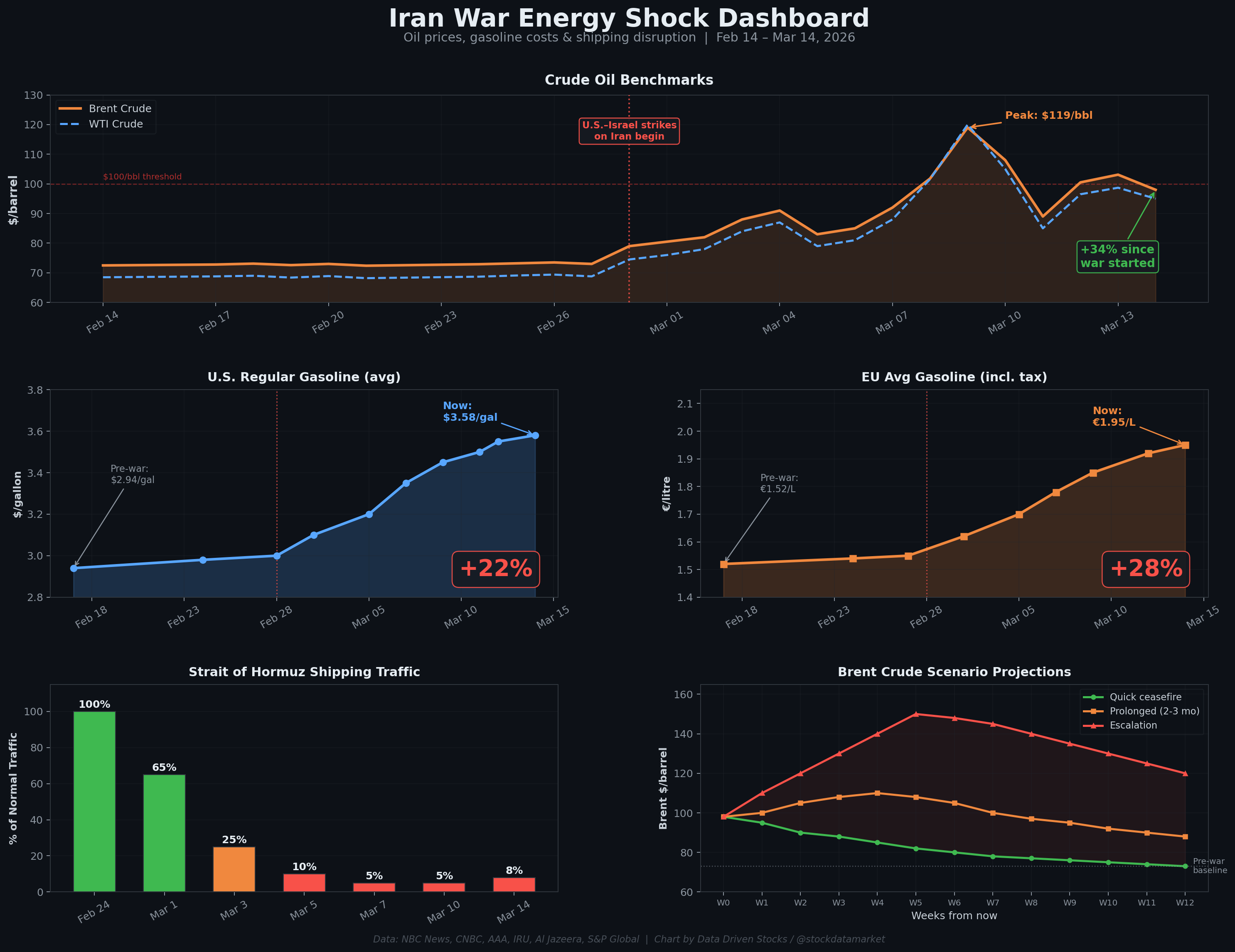

Iran War Energy Shock Dashboard — Brent crude has surged past $100/bbl, U.S. gasoline is up 22% and EU gasoline up 28% since Feb 28. Strait of Hormuz shipping has collapsed to 5% of normal capacity. …

Continue reading this post for free, courtesy of Data Driven Stocks.