The Invisible Gas That Could Kill the AI Chip Boom: Helium, Hormuz, and the 2026 Semiconductor Crisis

How a 21-mile-wide strait in the Persian Gulf controls the fate of a $700 billion industry - and why this crisis is unlike anything we’ve seen before.

Most people think semiconductors are about silicon. They think the chip supply chain starts in a Taiwanese fab and ends in an iPhone. They’re wrong.

The chip supply chain starts in a Qatari gas field, moves through a cryogenic dewar at -269°C, sails through a 21-mile chokepoint between Iran and Oman, and arrives at a fabrication plant where it performs a function that no other element on the periodic table can replicate: it cools wafers during lithography with unmatched thermal conductivity.

That element is helium. And right now, roughly one-third of the world’s supply is trapped behind the Strait of Hormuz.

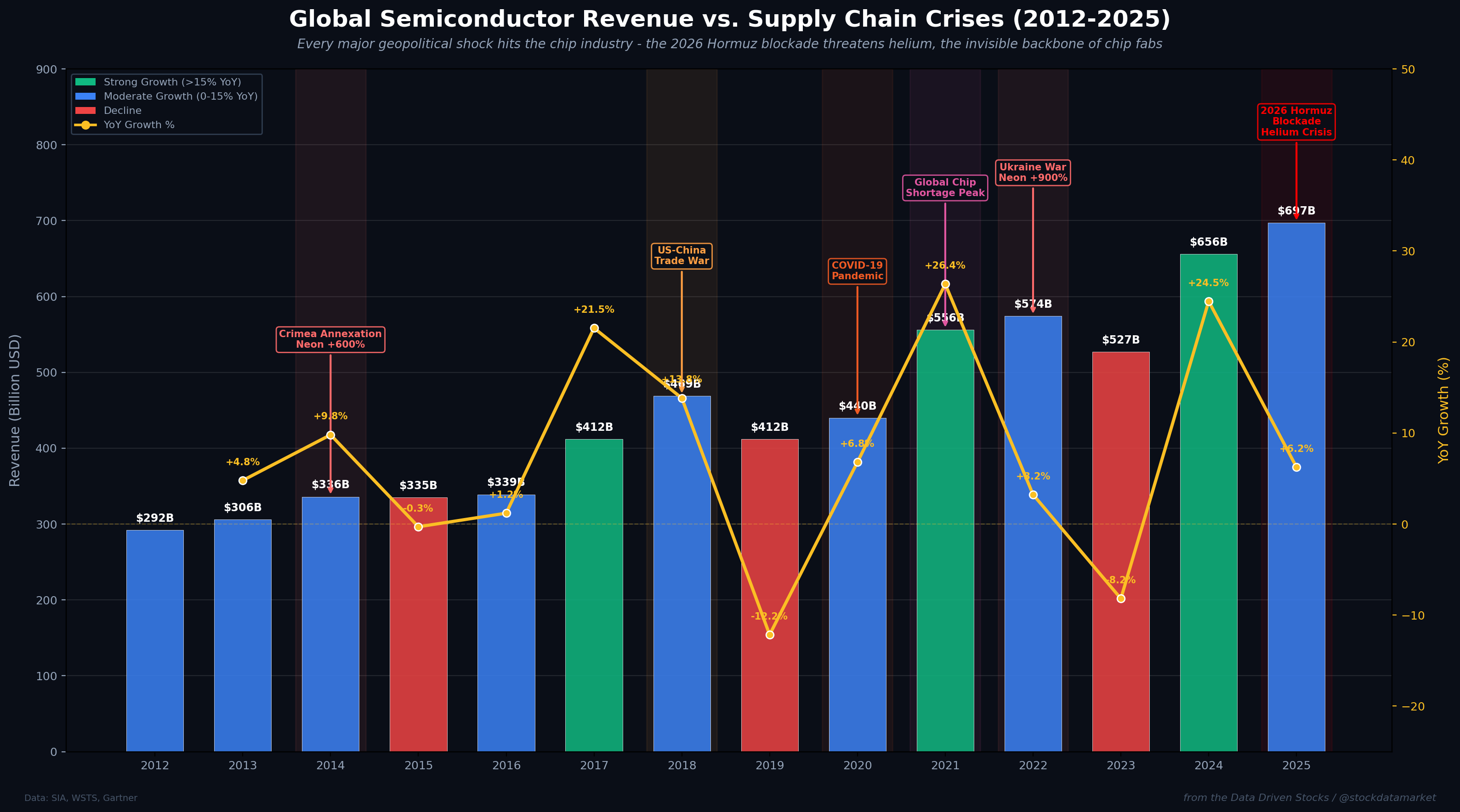

The semiconductor industry has survived a lot. The 1988 US-Japan trade pact that starved chip makers of SRAM. The 2011 earthquake that knocked out Renesas plants supplying 30% of global microcontrollers. The 2014 Crimea annexation that spiked neon gas prices by 600%. The COVID-19 pandemic that scrambled every supply chain on Earth. The 2022 Ukraine war that saw neon prices surge tenfold and xenon rocket from $15 to over $100 per liter.

But the 2026 Hormuz blockade is different. It targets the one material that chip fabs cannot substitute, cannot easily recycle, and cannot stockpile for more than a few weeks. And the clock is already ticking.

Why Helium Matters More Than You Think

To understand why the semiconductor industry is holding its breath (pun intended), you need to understand what helium actually does inside a chip fab.

When advanced chips are manufactured - the kind powering NVIDIA’s GPUs, Apple’s A-series processors, and every AI datacenter on the planet - wafers must be held at precisely controlled temperatures during photolithography and plasma etching. Helium is blown across the backside of wafers to remove heat with surgical precision. Its thermal conductivity is roughly six times higher than nitrogen and ten times higher than argon. There is no adequate substitute. Semiconductor engineers have tried argon and nitrogen alternatives, and the results are clear: throughput drops, yields degrade, and the economics of a $20 billion fab fall apart.

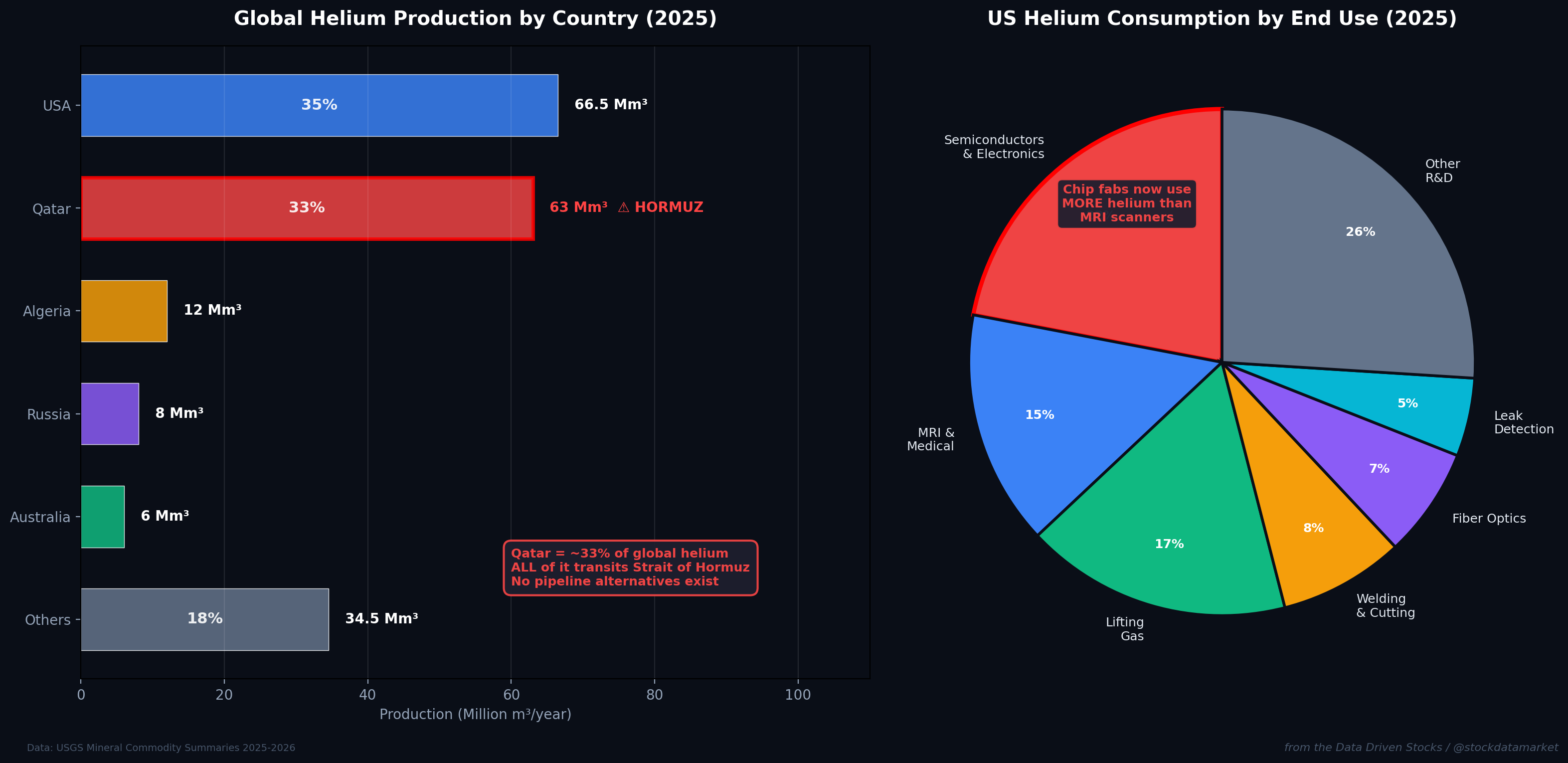

Helium also serves as the inert ambient gas during etching processes and is critical for leak detection in vacuum systems - the kind of systems that every EUV lithography machine depends on. Here’s the kicker: chipmaking now consumes more helium than MRI scanners. As the AI buildout has accelerated, fab demand for helium has grown faster than any other end use.

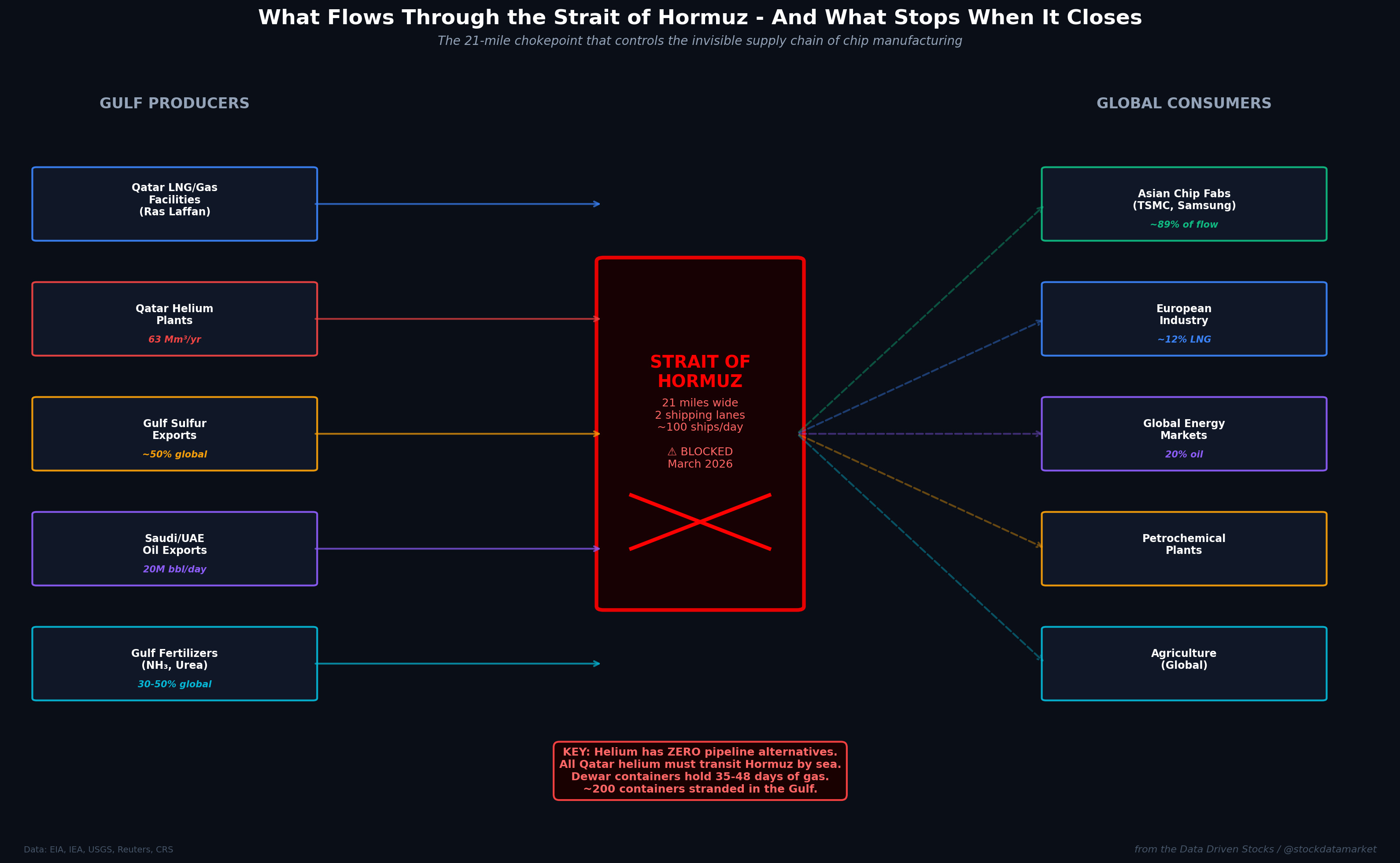

The global helium market produces around 160-190 million cubic meters per year. The United States accounts for about 35% of that, Qatar roughly 33%, Algeria around 5-8%, and Russia 3-5%. But here is the critical detail that most analysts overlook: helium is a byproduct of natural gas and LNG processing. You cannot just “turn on” more helium production. When Qatar’s Ras Laffan LNG complex shuts down - as it did after Iranian drone strikes in early March 2026 - the helium plants shut down with it. They are physically integrated into the same facility.

And unlike oil, which Saudi Arabia and the UAE can partially reroute through pipelines to Red Sea ports, helium has zero pipeline alternatives. Every cubic meter of Qatar’s helium must be liquefied to -269°C, loaded into vacuum-insulated dewar containers (each costing about $1 million), placed on cargo ships, and sailed through the Strait of Hormuz. There is no Plan B. There is no land route. There is no airlift at this scale.

The Chokepoint That Controls Everything

The Strait of Hormuz is 21 miles wide at its narrowest point. It has two shipping lanes, each about two nautical miles across, separated by a two-mile buffer zone. On a normal day in 2025, roughly 100 cargo-carrying vessels transited this passage, with 60-70% being oil tankers or LNG carriers.

On March 2, 2026, the Islamic Revolutionary Guard Corps officially declared the strait closed and announced that any ship entering would be attacked. This came after weeks of escalating strikes, VHF radio warnings, and confirmed attacks on at least 21 merchant vessels. Tanker traffic dropped first by approximately 70%, then effectively to zero.

The numbers are staggering. Before the blockade, 20 million barrels of oil per day transited Hormuz, representing about 20% of global petroleum consumption. About 20% of the world’s LNG trade passed through - primarily from Qatar, the world’s second-largest LNG exporter, which shipped over 112 billion cubic meters in 2025 with roughly 93% of those volumes going through the strait. Asia received about 89% of crude oil and 83% of LNG passing through the chokepoint. China alone got a third of its oil via this route.

But the energy angle, dramatic as it is, actually understates the problem for semiconductors. Oil has pipeline bypass options. Saudi Arabia’s East-West pipeline can redirect up to 5-7 million barrels per day to Red Sea ports. The UAE’s ADCOP pipeline reaches Fujairah on the Arabian Sea. LNG is harder - there are no alternative routes for Qatari or Emirati LNG, and the IEA estimated that a full strait closure would drop global LNG supply by over 300 million cubic meters per day, double the throughput of the Nord Stream pipeline.

But helium? Helium has nothing. No pipelines, no alternative ports, no emergency reserve system like the Strategic Petroleum Reserve. Just roughly 2,000 dewar containers circulating globally, of which some 200 were stranded in the Gulf when the blockade began.

The Countdown: How Fast Does Helium Run Out?

Here is where things get truly uncomfortable for the semiconductor industry.

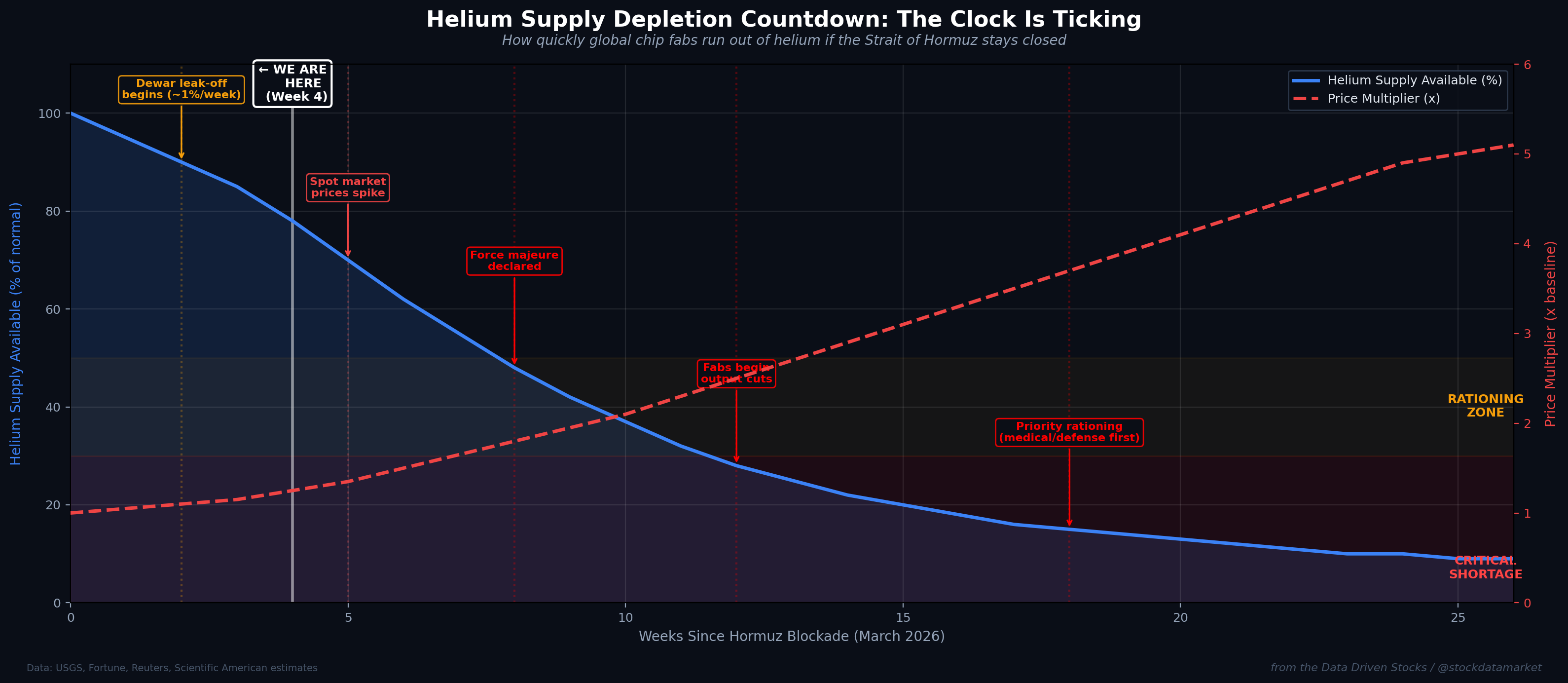

Modern chip fabs operate on lean inventories. Industry sources indicate that wafer fabrication plants typically hold only 1-3 months of high-purity gas supplies. After the 2022 neon shock from the Ukraine war, major chipmakers like TSMC, Samsung, and Intel built up safety stocks to buffer roughly 60-90 days of specialty gas supply. But smaller fabs have far less cushion.

Helium stored in dewar containers has a shelf life of 35-48 days before it begins leaking and is irretrievably lost to the atmosphere. Even in sealed systems inside fabs, helium leaks at roughly 0.1-1% per month. Unlike oil that you can store in a tank for years, helium is constantly escaping.

USGS consultant Phil Kornbluth has estimated that at least 6 weeks would pass before even partial resumption of Qatar’s helium output, even if the strait reopened immediately. Repositioning the 200 stranded dewar containers would take another 2-3 months. Fortune and Reuters analyses converge on the same point: nobody has run out yet, but the shortage arrives within weeks, not months.

The economic modeling is grim. A 30-day blockade was expected to raise helium prices 10-20%. Beyond 60 days, analysts project 50% or greater price spikes and selective rationing. As of late March 2026, we are roughly four weeks into the crisis, and the strait remains firmly closed.

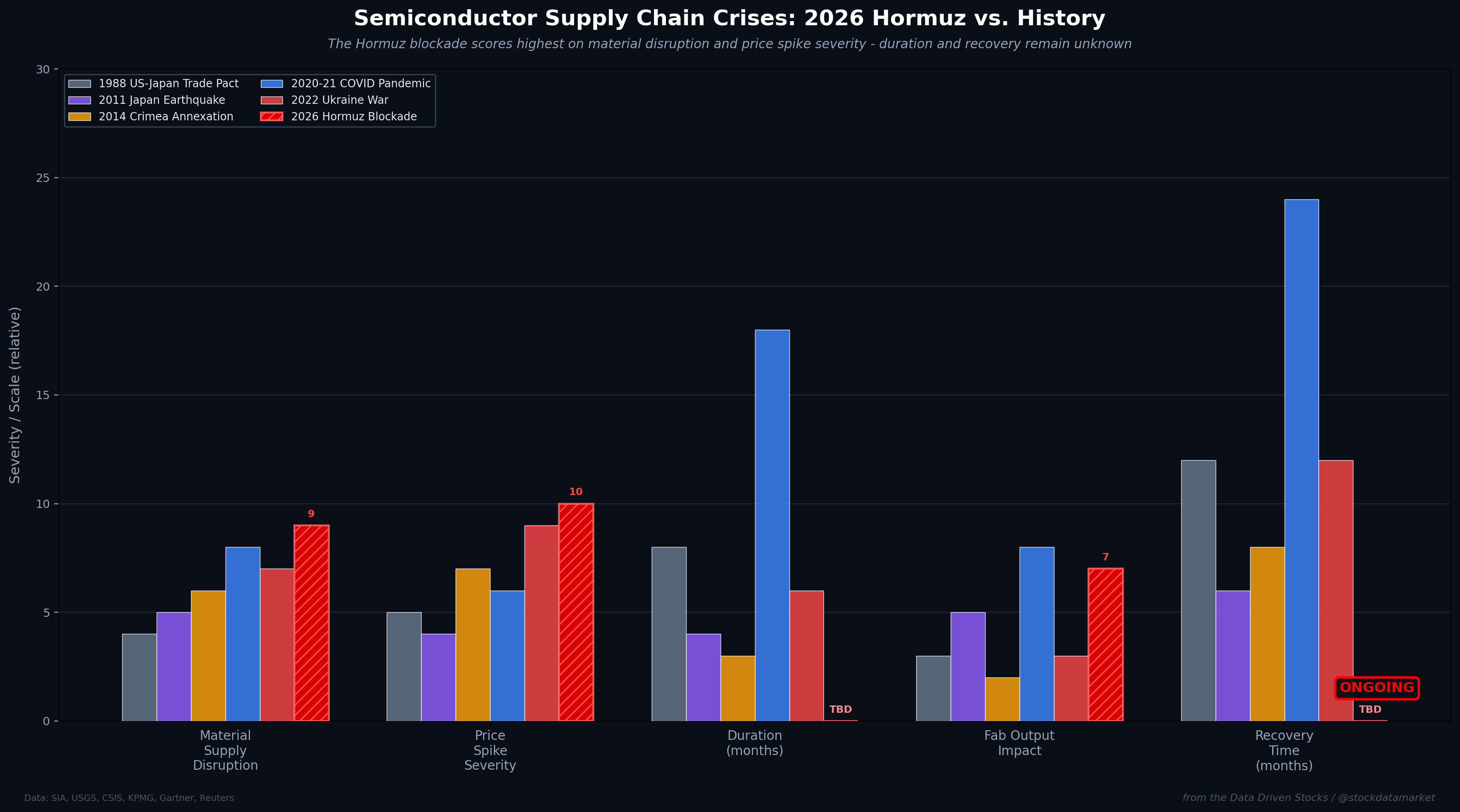

2026 vs. Every Past Semiconductor Crisis

To appreciate how different this moment is, it helps to line up the 2026 Hormuz crisis against every major semiconductor supply disruption of the past four decades.

The 1988 US-Japan semiconductor trade pact was a demand-side squeeze. Japanese manufacturers cut production to stop “dumping” chips below cost, and American firms didn’t re-enter the market fast enough. Hitachi factory workers gave up their summer vacations to meet demand. But raw materials were not the bottleneck - capacity was.

The 2011 Tohoku earthquake knocked out critical Japanese factories, most notably Renesas Electronics, which supplied 30% of the world’s automotive microcontrollers. Recovery took about 100 days. But the disruption was geographically contained and alternative suppliers existed.

The 2014 Crimea annexation was the first time a geopolitical shock hit semiconductor raw materials directly. Neon prices spiked 600% because Ukraine and Russia together supplied 50-70% of the world’s semiconductor-grade neon. But fabs had time to diversify. Linde invested $250 million in a neon plant in Texas. The industry adapted.

The 2020-2021 COVID pandemic was the most far-reaching crisis, costing the US economy an estimated $240 billion in 2021 alone. Median chip inventories plummeted from 40 days to under 5 days. Auto production lost over 11 million vehicles in 2021 alone. Lead times for semiconductors from Broadcom stretched to 22 weeks, nearly double the pre-pandemic norm. But the bottleneck was wafer fabrication capacity and surging demand, not raw material availability.

The 2022 Ukraine war hit specialty gases again. Neon prices in China surged tenfold by March 2022. Xenon went from $15 per liter to over $100. Krypton quadrupled. But this time, the industry was better prepared. TSMC and Samsung had built strategic stockpiles. Excimer laser manufacturers reduced neon consumption by 25-70% through process optimization. The predicted catastrophe was averted.

So what makes 2026 different? Three things.

First, the material at risk - helium - has no substitute. When neon spiked in 2014 and 2022, manufacturers could optimize laser processes, recycle gas, and diversify suppliers. With helium, the options are far more limited. Advanced fabs can recycle up to 90% of helium within tools, but older facilities in Southeast Asia recover only about 50%. And there is no alternative gas that can match helium’s thermal conductivity for backside wafer cooling.

Second, the supply concentration is more acute. Qatar alone represents roughly a third of global helium, and 100% of that output transits Hormuz. When Ukraine’s neon was disrupted in 2022, China and the US could partially compensate. When Qatar’s helium is disrupted, the math simply doesn’t work - remaining Western producers (the US Cliffside facility, Algeria, Australia) cover only about 40% of global demand.

Third, the physical constraints are uniquely brutal. Helium cannot be stored long-term. It leaks through virtually every container. The specialized dewar shipping infrastructure is limited to about 2,000 units globally, and 10% of those are now stranded in the Gulf. Even if alternative supply comes online, the logistics of repositioning cryogenic containers at -269°C across new shipping routes (via the Cape of Good Hope, adding weeks of transit time) create a bottleneck that has no precedent in semiconductor history.

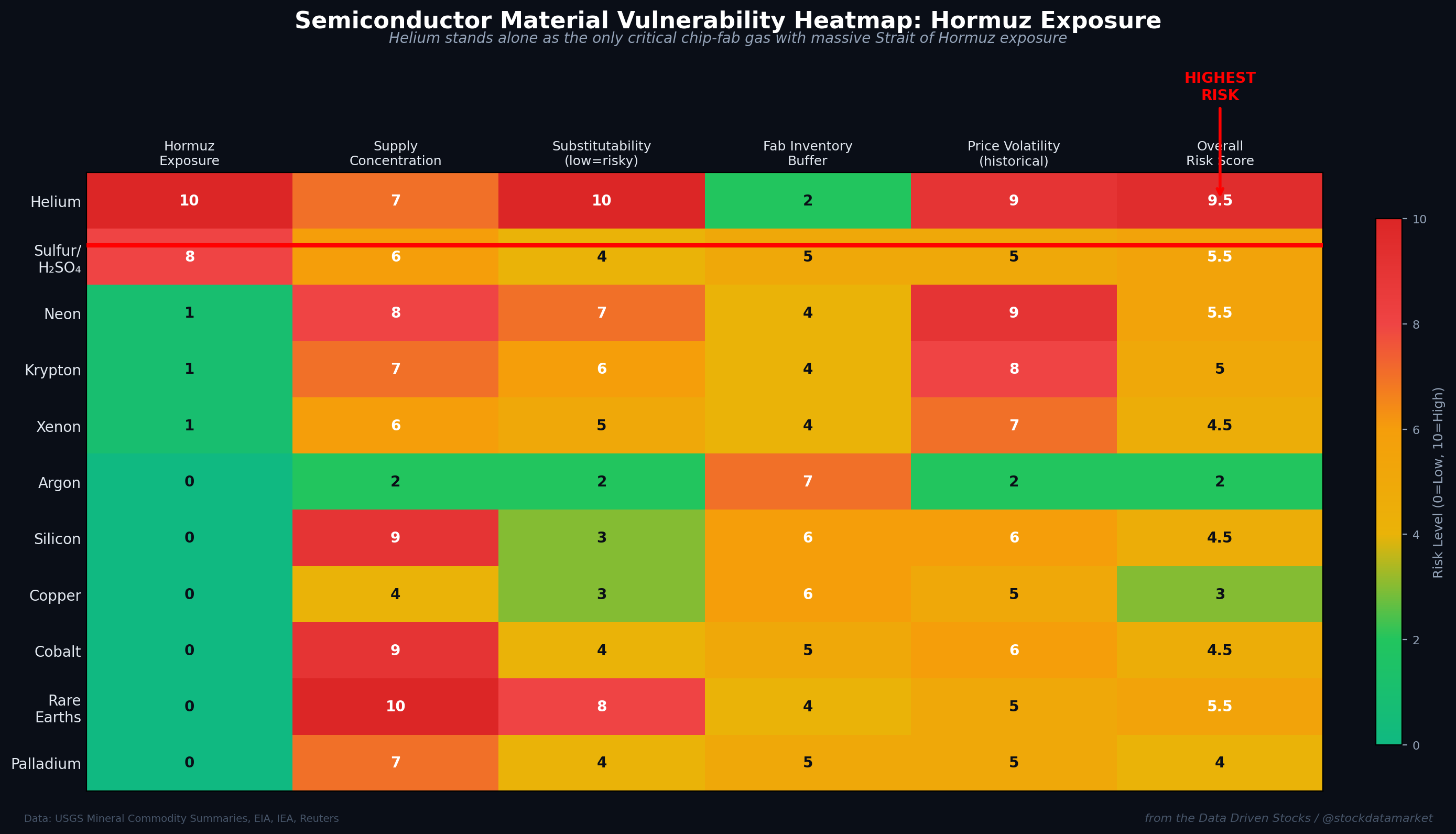

The Wider Material Map: What’s at Risk and What’s Not

Helium is the headline, but it’s not the only semiconductor material flowing through the Strait of Hormuz.

Sulfur and sulfuric acid are the second concern. The Gulf states produce roughly 50% of the world’s sulfur exports, and sulfuric acid is a critical chemical for wafer cleaning and etching. A prolonged Hormuz closure would raise input costs for the high-purity acids that every chip fab consumes in enormous quantities.

But the good news - if you can call it that - is that most other semiconductor raw materials are not Hormuz-dependent. Neon, krypton, and xenon come primarily from air separation plants in the US, Europe, and East Asia. After the painful lessons of 2014 and 2022, major chipmakers built strategic neon stockpiles in Taiwan and Japan covering two or more months of supply. Silicon metal comes overwhelmingly from China (over 70%), Brazil, and Norway. Copper is mined in Chile, Peru, and the DRC. Rare earth elements are dominated by Chinese production. Cobalt comes from the Congo. Palladium from Russia and South Africa. None of these supply chains route through the Strait of Hormuz.

This is both a relief and a trap. Because most semiconductor materials are unaffected, the industry may underestimate the severity of the helium-specific disruption until it is too late. Helium represents a small fraction of total fab costs - less than 1% of wafer cost - but it is a hard constraint. You cannot run a lithography tool without it. A 1% cost item can become a 100% production bottleneck.

What Happens Next: Scenarios and Industry Response

The semiconductor industry is not sitting idle. Several mitigation strategies are already underway.

On the supply side, the US Bureau of Land Management’s Cliffside facility in Texas is ramping output. Japan’s Iwatani has reported stable imports thanks to US supplies and local stockpiles. Algeria’s Hassi R’Mel complex continues shipping via Mediterranean routes untouched by the Hormuz crisis. Canada and Australia are accelerating expansion plans. But none of these can replace 63 million cubic meters of annual Qatari output on a timeline of weeks.

On the demand side, fabs are aggressively implementing helium recycling. Samsung and TSMC’s most advanced facilities already recover about 90% of helium within their tools. But this means the most advanced fabs are relatively protected, while older facilities - which make up a substantial share of global chip output - face steeper cuts.

Governments are stepping in as well. Medical and defense applications are being prioritized over industrial uses. The rationing hierarchy is likely to follow a familiar pattern: MRI scanners and military systems first, then cutting-edge AI chip fabs, then mainstream semiconductor production, then everything else (lifting gas, welding, leak detection). The balloon industry is the first casualty.

Three scenarios are worth considering.

In the optimistic case, the strait reopens within 30-60 days through diplomatic resolution or military action. Helium prices spike 10-30%, fabs absorb higher costs, consumer electronics prices tick up modestly (under 5%), and the industry weathers the shock better than the COVID disruption thanks to post-pandemic stockpiling and diversification efforts.

In the base case, the blockade persists for 3-6 months. Helium prices double or more. Fabs begin selective output cuts, prioritizing advanced nodes (where margins are highest and helium recycling is most efficient) while scaling back production on mature nodes. AI chip delivery timelines slip. Automotive and consumer electronics production takes a meaningful hit. Memory prices rise. The global semiconductor industry loses momentum on what was shaping up to be a record year - Gartner had projected $717 billion in 2025 revenue with continued growth into 2026.

In the worst case, the strait remains closed beyond six months. The helium supply system effectively breaks. Dewar containers are lost or stranded. Supplier contracts go into force majeure. Fabs operate at reduced capacity indefinitely. The cascading effects spread to adjacent industries - MRI availability drops, scientific research stalls, fiber optic cable production slows. The AI infrastructure buildout, which depends on a constant flow of cutting-edge chips from TSMC and Samsung, hits a wall that no amount of capital spending can overcome in the short term.

The Lesson History Keeps Teaching

Every semiconductor crisis of the past 40 years has delivered the same lesson: concentration kills. When SRAM production was concentrated in Japan in 1988, the trade pact exposed the vulnerability. When neon was concentrated in Ukraine, the 2014 and 2022 conflicts exposed the vulnerability. When wafer fabrication was concentrated in Taiwan and Korea, COVID exposed the vulnerability.

Now, helium - concentrated in Qatar and funneled through a single 21-mile maritime chokepoint - is the latest expression of this pattern. And unlike previous crises, where the industry had months or years to diversify, helium’s physical properties (it leaks, it cannot be stored long-term, it must be shipped cryogenically) compress the timeline to weeks.

The semiconductor industry generated $656 billion in revenue in 2024, up 21% year over year. It was projected to surpass $700 billion in 2025. NVIDIA alone became the world’s largest semiconductor company by revenue, riding the AI boom. The top 10 chip companies reached $6.5 trillion in combined market capitalization by December 2024.

All of that growth depends on a supply chain that most investors never think about. Not the silicon wafers, not the EUV lithography machines, not the copper interconnects. The invisible gas that keeps everything cool.

The Strait of Hormuz has been described as the world’s most critical energy bottleneck. As of March 2026, it has become something more: the most critical bottleneck for the AI revolution itself.

The clock is ticking. The dewars are leaking. And the fabs are counting their days.

This analysis is for informational purposes only and does not constitute investment advice. Market conditions are evolving rapidly.

Sources:

U.S. Geological Survey, Mineral Commodity Summaries for Helium (2020-2026), Rare Gases, Silicon, Copper, Cobalt, Rare Earths, and PGMs.

U.S. Energy Information Administration, “Amid Regional Conflict, the Strait of Hormuz Remains Critical Oil Chokepoint” (June 2025); “About One-Fifth of Global LNG Trade Flows Through the Strait of Hormuz” (2024).

International Energy Agency, Strait of Hormuz Factsheet (February 2026); Middle East and Global Energy Markets Report (March 2026).

Congressional Research Service, “Iran Conflict and the Strait of Hormuz: Impacts on Oil, Gas, and Other Commodities” (R45281, March 2026).

Gartner, “Worldwide Semiconductor Revenue Grew 21% in 2024” (April 2025); “Forecasts Worldwide Semiconductor Revenue to Grow 14% in 2025” (October 2024).

Semiconductor Industry Association (SIA) and World Semiconductor Trade Statistics (WSTS), Global Semiconductor Sales Data (2012-2025).

Deloitte, “2025 Global Semiconductor Industry Outlook” (2025).

MIT Technology Review, “The Era of Cheap Helium Is Over” (February 2024).

CSIS, “Russia’s Invasion of Ukraine Impacts Gas Markets Critical to Chip Production” (March 2022).

KPMG, “Russia-Ukraine War: Impact on the Semiconductor Industry” (May 2022).

SPIE, “Noble Gases and the Shock of War” (May/June 2023).

Helium One Global, Helium Market Analysis (December 2024).

Reuters, Fortune, Scientific American, CNBC, and The National - reporting on the 2026 Hormuz crisis and helium market conditions (March 2026).

Wikipedia, “2026 Strait of Hormuz Crisis” and “2020-2023 Global Chip Shortage.”

Bureau of Land Management (BLM), Federal Helium Program posted prices (2019-2022).

Fusion Worldwide, “Global Chip Shortage: Timeline and Key Events.”

World Economic Forum, “Chip Shortage: How the Semiconductor Industry Is Dealing with This Worldwide Problem” (February 2022).

U.S. Department of Commerce, “Results from Semiconductor Supply Chain Request for Information” (January 2022).

Visual Capitalist, “Charted: Global Energy Flows at Risk in the Strait of Hormuz” (March 2026).

SOH still closed but no problems (yet?) with helium?