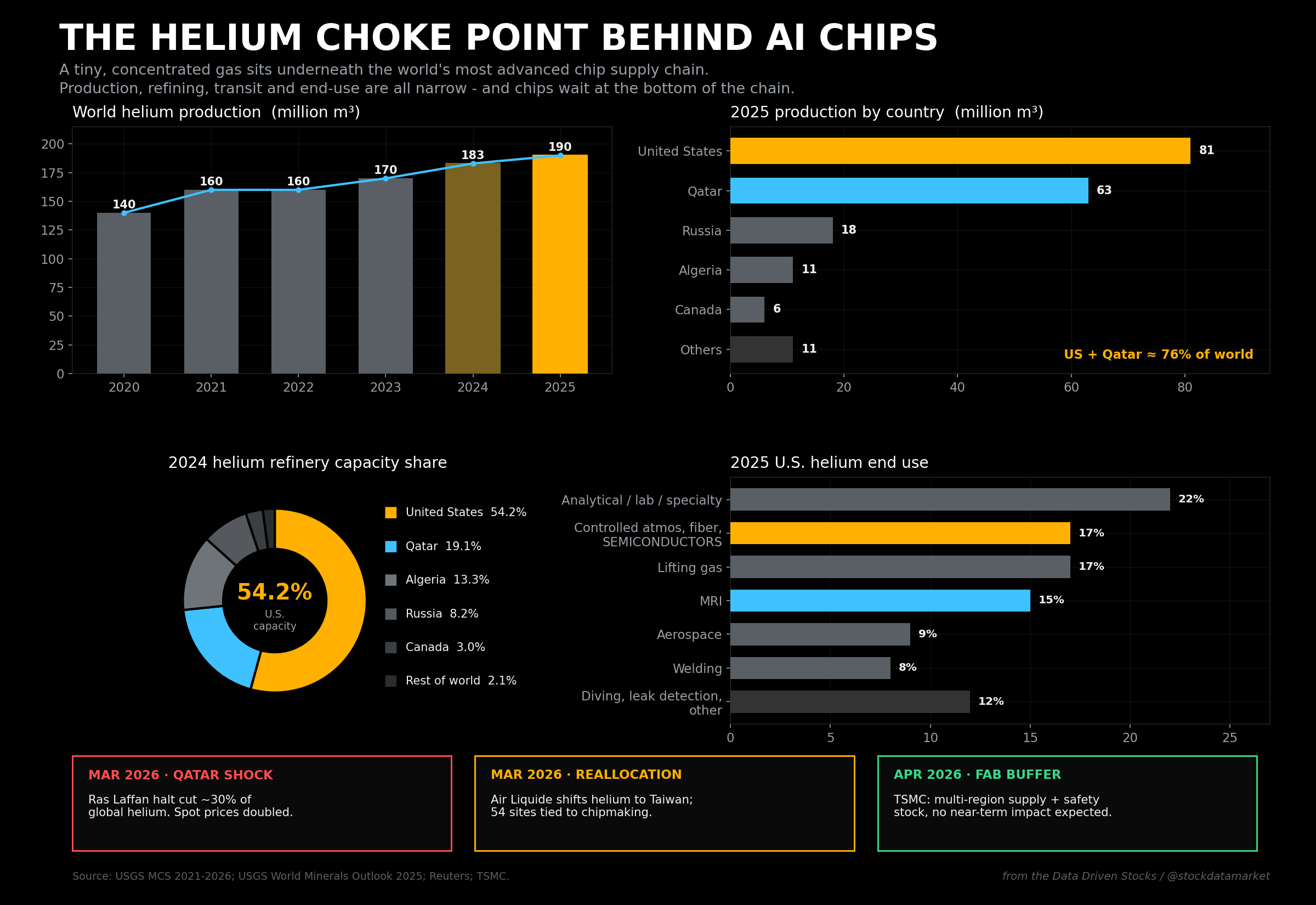

World helium supply recovered after 2020, but it is still tiny, concentrated, and tied to specialized logistics. The chip angle is not about balloons. It is about cooling, process stability, and prio…

Continue reading this post for free, courtesy of Data Driven Stocks.