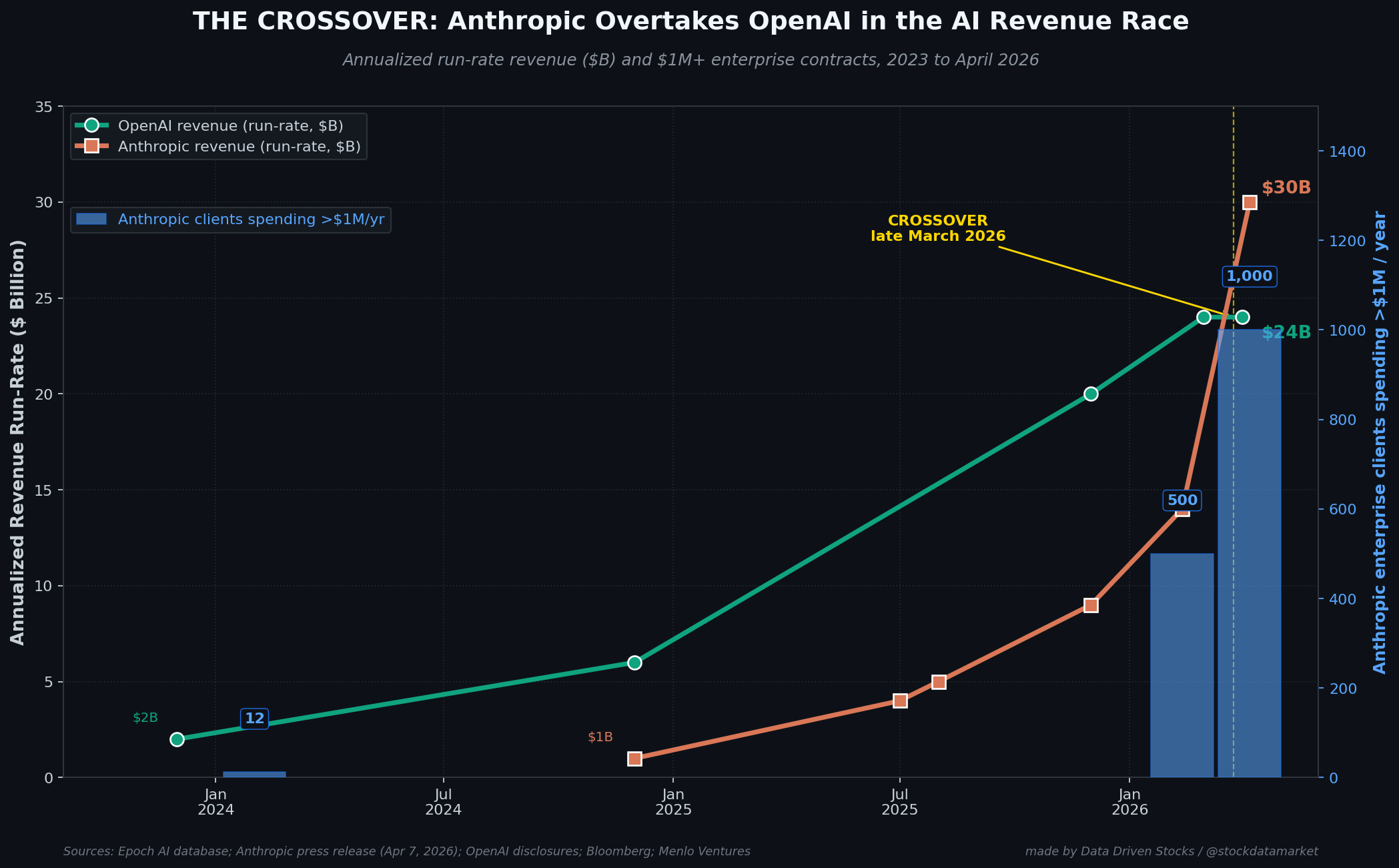

The Crossover: How Anthropic Quietly Lapped OpenAI in 15 Months and Reset the Entire AI Market

A data-driven autopsy of the $30 billion moment that just rewrote the AI playbook - and what it means for global markets, enterprise software, and the coming wave of AI IPOs.