The $4 Trillion Triple-IPO Is Coming - and Only One of These Three Is Actually Ready

SpaceX, Anthropic and OpenAI are all stampeding toward the public market at once. We pulled the numbers. The gap between the hype and the homework is enormous.

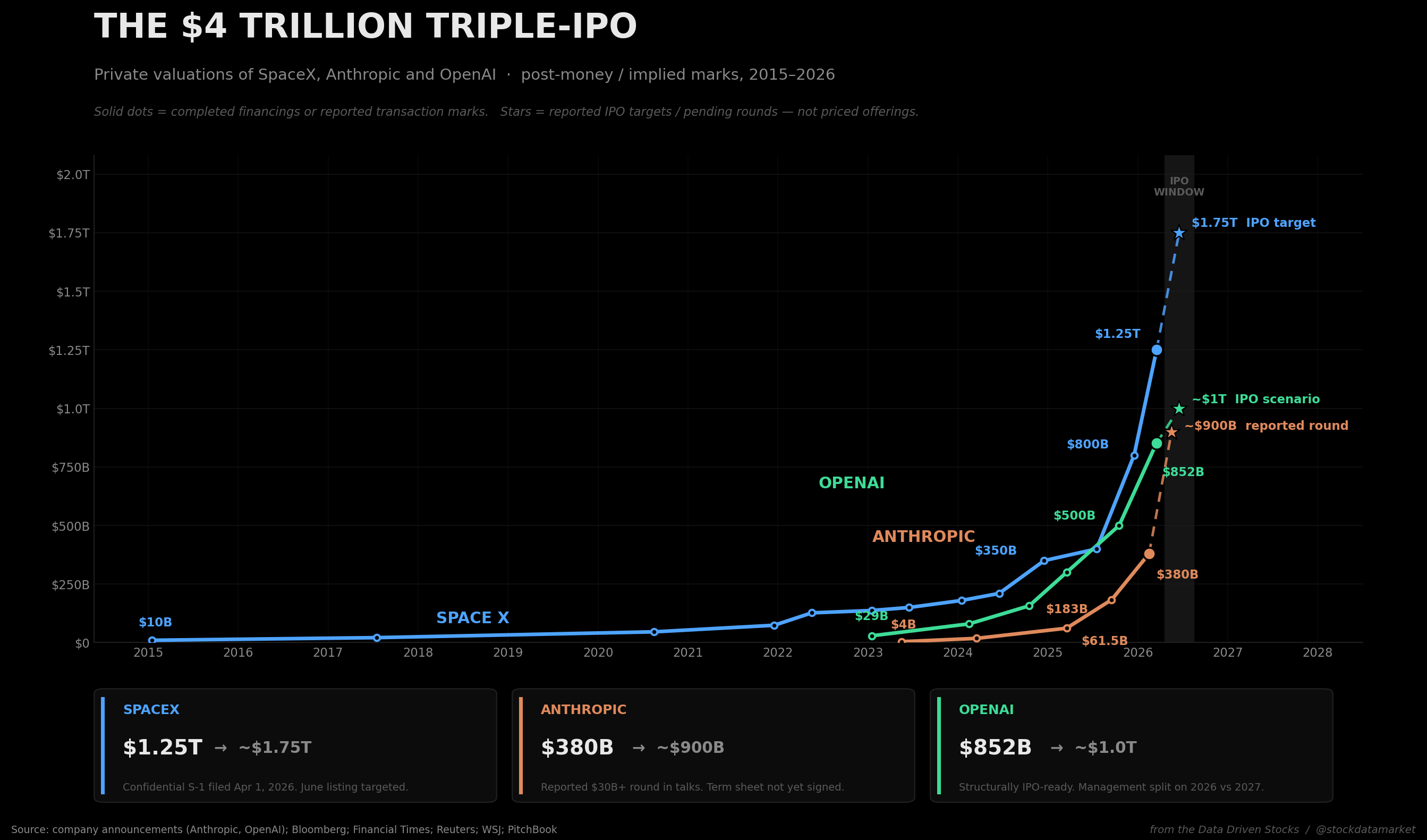

Private valuations of SpaceX, Anthropic and OpenAI, 2015-2026. Solid dots are completed financings or reported transaction marks; stars are reported IPO targets and pending rounds - not priced offeri…

Continue reading this post for free, courtesy of Data Driven Stocks.