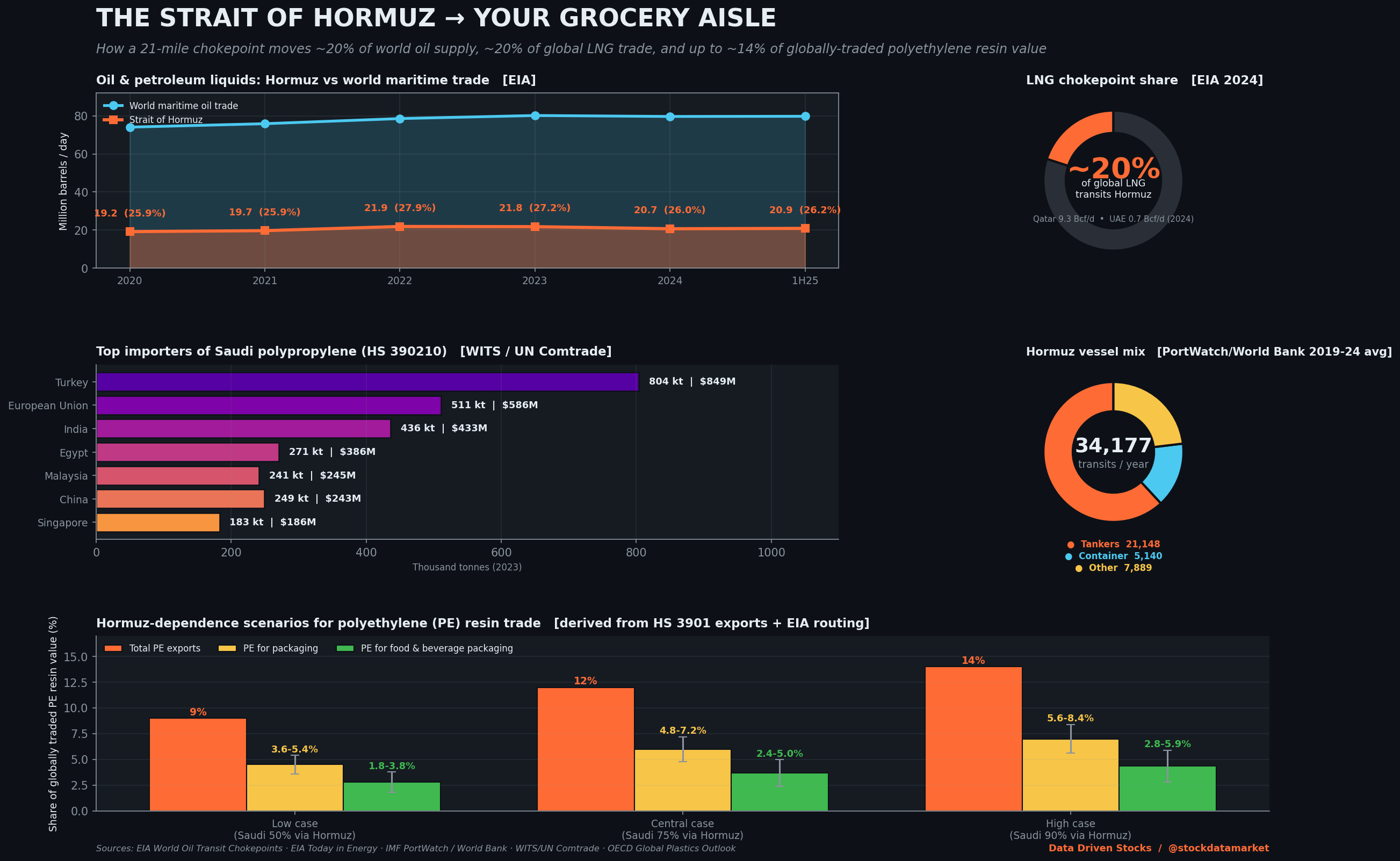

The 21-Mile Chokepoint Hiding in Your Yogurt Cup: Why an Iran War at the Strait of Hormuz Could Rewire Global Food Packaging in 2026

Everyone talks about Hormuz as an oil story. Almost nobody talks about the pellets. That is a mistake - and 2026 may be the year we finally pay for it.