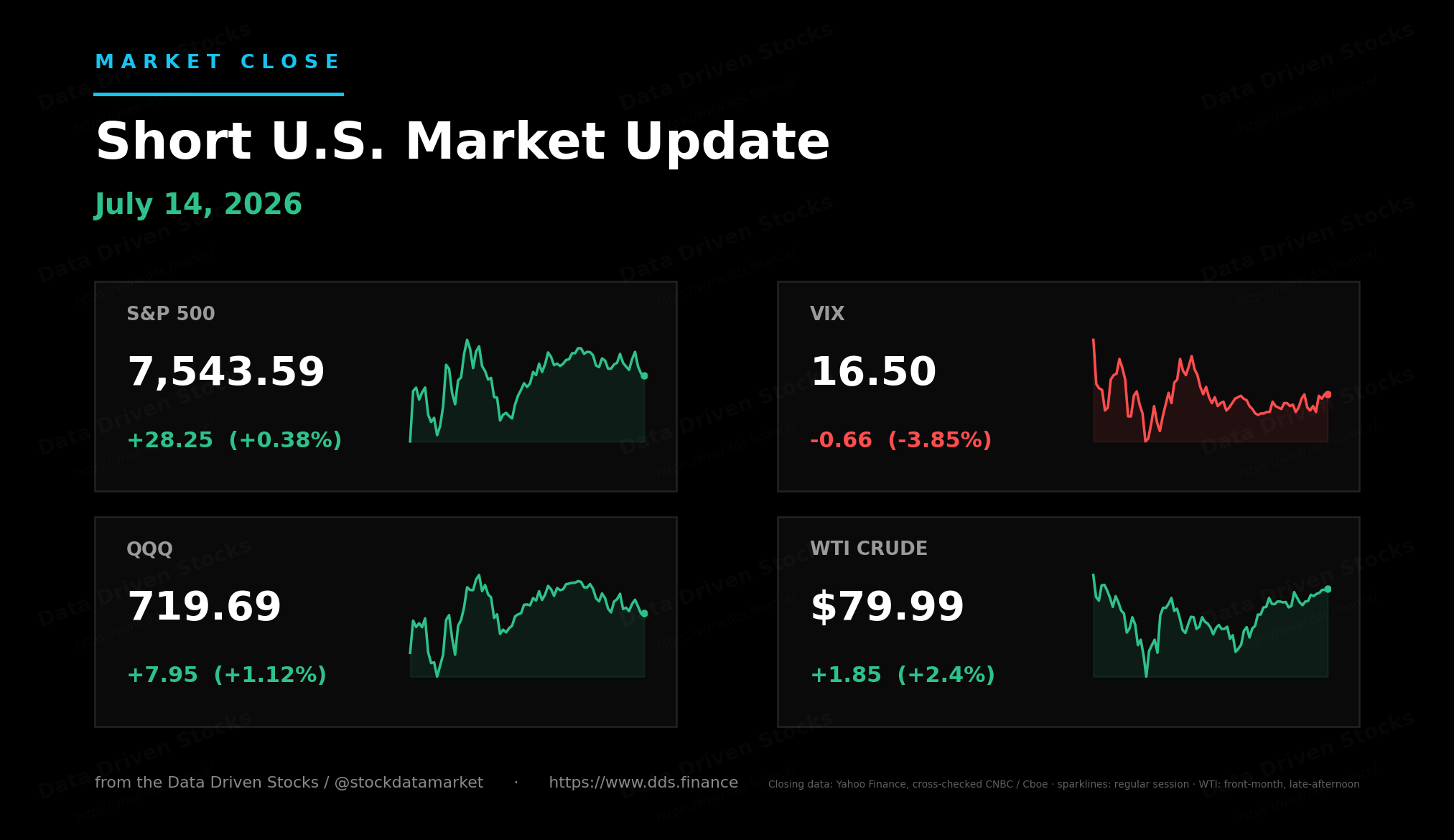

Short U.S. Market Update - July 14, 2026 - Market Close

Weird market, and nothing did change since pre-market aside from Iran-U.S. war escalation

By the time you read this, New York has gone home and Wednesday is already warming up somewhere between Seoul and Sydney. The cold June CPI got the day it deserved on the tape, sort of. The S&P 500 closed at 7,543.59, up 0.38%, and that number is doing a lot of work: it sits above the 7,525 support that mattered this morning, below the 7,550 pivot, and just under the rising BULL trendline that carried the index through early July. That line was support on the way up. Today the market walked up to it from below and could not close through it. Call it what it is: an ambiguous close, with positioning to match.

An ambiguous close

The shape of the session tells the story better than the closing print. The index dipped right at the open, ticking a low of 7,513.23 in the first minutes, then rallied straight through Fed Chair Warsh’s 10:00 testimony to the day’s high of 7,557.44 just after 11. Then it spent the entire afternoon leaking, from the mid 7,550s back to 7,543.59, giving up 7,550 and the trendline in the final stretch. Highs before lunch, fade into the bell. The morning map called for ping-pong between 7,550 and 7,600 and we got the ping-pong, just one floor lower, 7,513 to 7,557. Rate-hike expectations eased on the cold print, though the market still carries one 25 bp hike for 2026.

Under the surface it was a livelier day than the index suggests. Goldman Sachs closed up 9% on its earnings and JPMorgan added 2.5%, so the bank quarter aged much better than the sleepy pre-market reaction implied. IBM never found a bid and finished down 25.2% after its warning. And oil kept going: WTI added another 2.4% to just under $80, Brent to around 85.5, on top of Monday’s 9% jump, with the Strait of Hormuz still driving the whole complex.

QQQ and the Korea problem

QQQ rose 1.1% to 719.69, and on the chart that gain bought exactly nothing. The rising support line that held this whole leg broke on Monday. Today’s bounce carried price back up to the underside of that line and stalled there into the close. A retest from below that fails to reclaim is not a bullish look, whatever the daily percentage says.

The reason sits in Seoul. The KOSPI, which at its late-June peak near 9,400 had more than doubled on the year, is now about 27% below that peak. On Monday it fell 8.95% to 6,806.93, tripping the seventh circuit breaker of the year, which means more than half of all circuit breakers in the Korea Exchange’s history have now fired in 2026. SK Hynix dropped 15.4%, its worst session on record, two days after raising over $26 billion in its Nasdaq ADR debut, and Samsung lost 10.7%. Tuesday’s bounce in Seoul was less than one percent, to about 6,850. The Korean AI-hardware trade led this entire leg higher. It looks exhausted, and QQQ trades like it knows.

VIX in no man’s land

The VIX closed at 16.50, down 0.66, and slipped back below the summer support line it had reclaimed only yesterday. Between 16 and 18, the two accelerators from this morning’s map, there is simply nothing: no level that forces the next move. Below 16 the vol-selling flywheel starts turning and equities get their grind fuel. Above 18 vol buying picks up speed toward 20, then 22. Tonight it sits in the middle of that range with no opinion at all, which is another way of saying tomorrow’s data gets to decide.

The strangest overnight map in a while

Now the part that made us look twice. The 1DTE market-maker data into tonight is unlike anything we remember seeing. Dealers’ single biggest positive-gamma block sits exactly where we closed, around 7,545 to 7,550. That is a pin. Just above it there is a band of negative gamma at 7,565 to 7,575, and higher up, at 7,650 to 7,670, a wall of negative charm next to the board’s biggest call blocks. Below the pin, though, there is almost nothing. A thin shelf near 7,430, then air, all the way down to 7,300, where the largest put block on the entire board and the strongest positive charm sit together.

Normally this map is a ladder, shelf after shelf. Tonight it is one pin and two trapdoors. The read is blunt: the market wants to sleep at 7,550, and if something happens overnight that breaks the pin, there is not much in the way before 7,430, and after that the magnet is 7,300. And the standing rule applies even to a map this strange: the tape spends most of its time between levels, not through them, so if price hands you one of these, a day trader, or anyone holding options near expiration, should think hard about taking the profit.

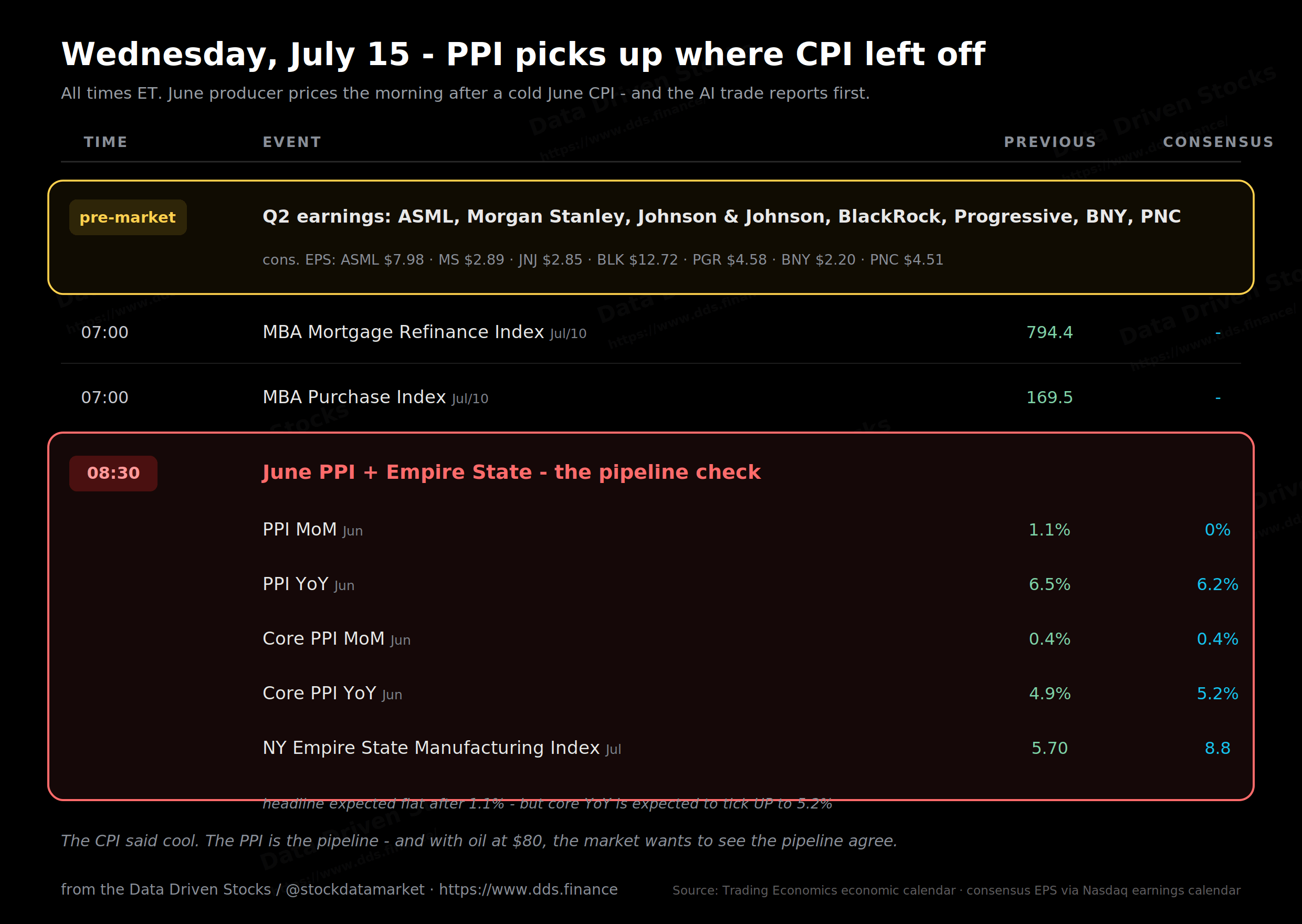

Tomorrow runs through the PPI and ASML

Wednesday funnels into 8:30 ET again. The June PPI is the other half of the inflation story: consensus wants the headline flat on the month after May’s 1.1%, and the yearly rate easing from 6.5% to 6.2%, but core PPI is actually expected to tick up, from 4.9% to 5.2% year over year. The CPI said cool. The PPI is the pipeline, and with oil sitting at $80 the market wants to see the pipeline agree. Empire State lands at the same minute, expected at 8.8 after 5.70, and the MBA mortgage numbers open the morning at 7:00.

Then there are the earnings, all before the bell: ASML, Morgan Stanley, Johnson & Johnson, BlackRock, Progressive, BNY and PNC. ASML is the one that matters for the chart above. It is the first major AI-capex print since Korea cracked, and its order book will speak directly to that “AI fades” line QQQ keeps living under.

So we head into the night pinned at 7,550 with two trapdoors below, a VIX with no opinion, and the AI trade’s report card due before breakfast. Sleep also with one eye on Seoul - we don’t know what KOSPI will do.