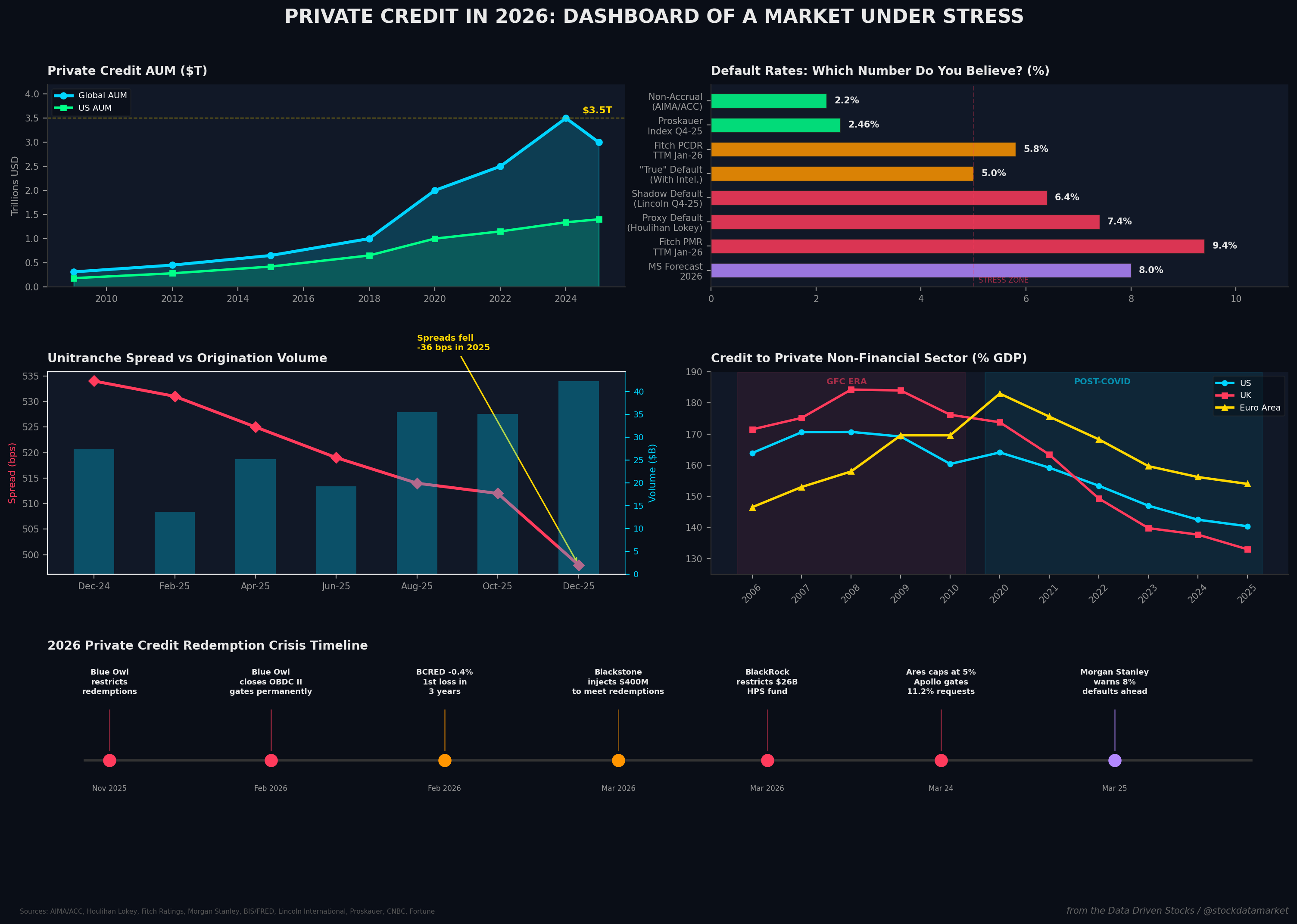

Private Credit 2026 Dashboard - Market Under Stress Private Credit in 2026: The $3.5 Trillion Market That Just Hit a Wall - Is This 2008 All Over Again?

Defaults climbing. Redemption gates slamming shut. Fund managers scrambling. The private credit market is facing its first real stress test - and the comparisons to 2008 are getting louder.