Prices Are Rising Fast In Europe Again - And This Time The Math Doesn’t Work

The March EU's Inflation HICP print wasn’t a blip. It was the first month of a regime change that the consensus is still pricing as transitory. Here is the data.

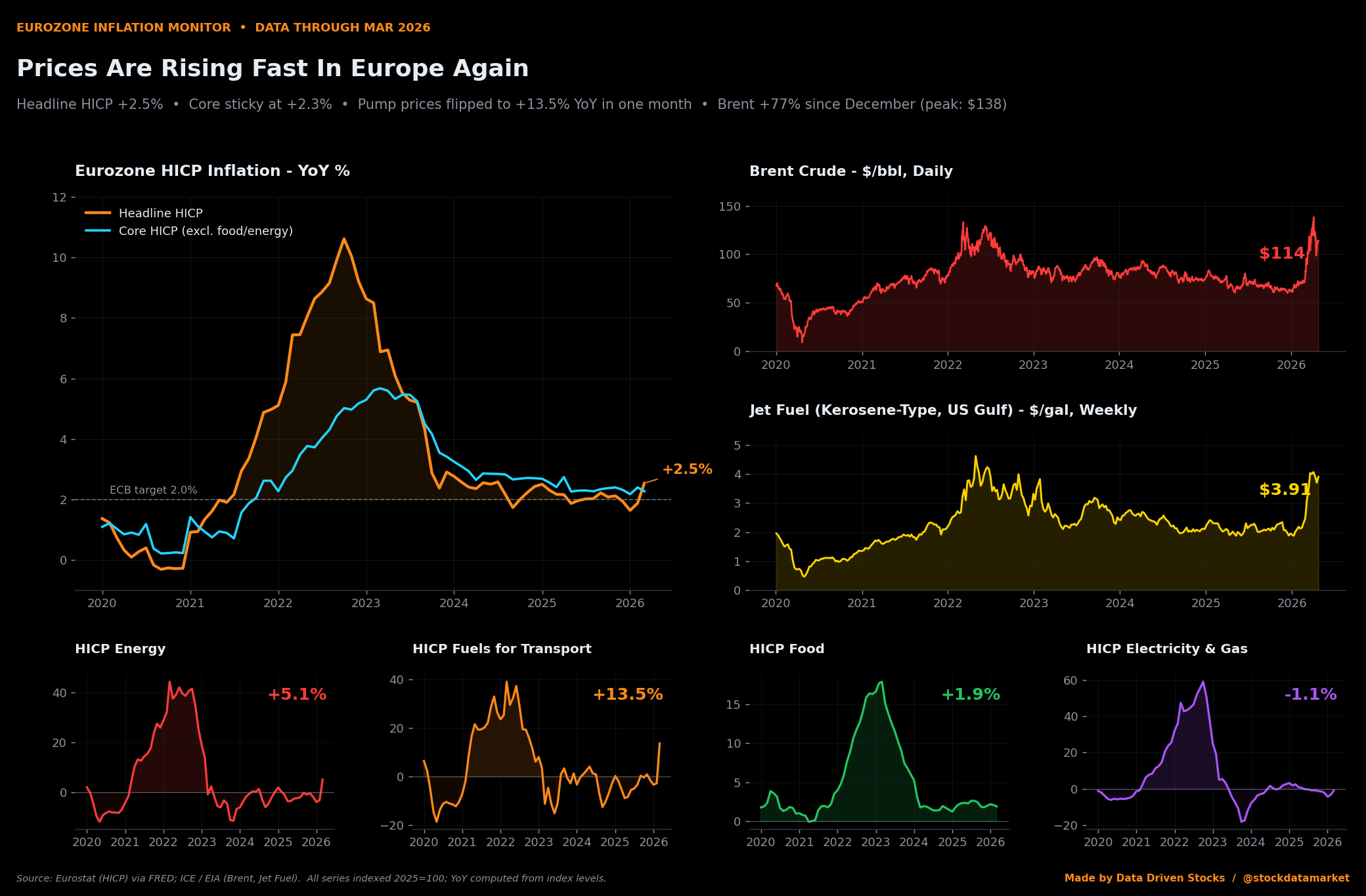

Eurozone inflation monitor through March 2026. Headline HICP back to +2.5% YoY, core sticky at +2.3%, pump prices flipped to +13.5% in a single month, and Brent has surged 77% from $64 to $114 since …

Continue reading this post for free, courtesy of Data Driven Stocks.