Options Trading Basics (Without the Mysticism)

If you want to lose a lot of money - it's a good place to start with

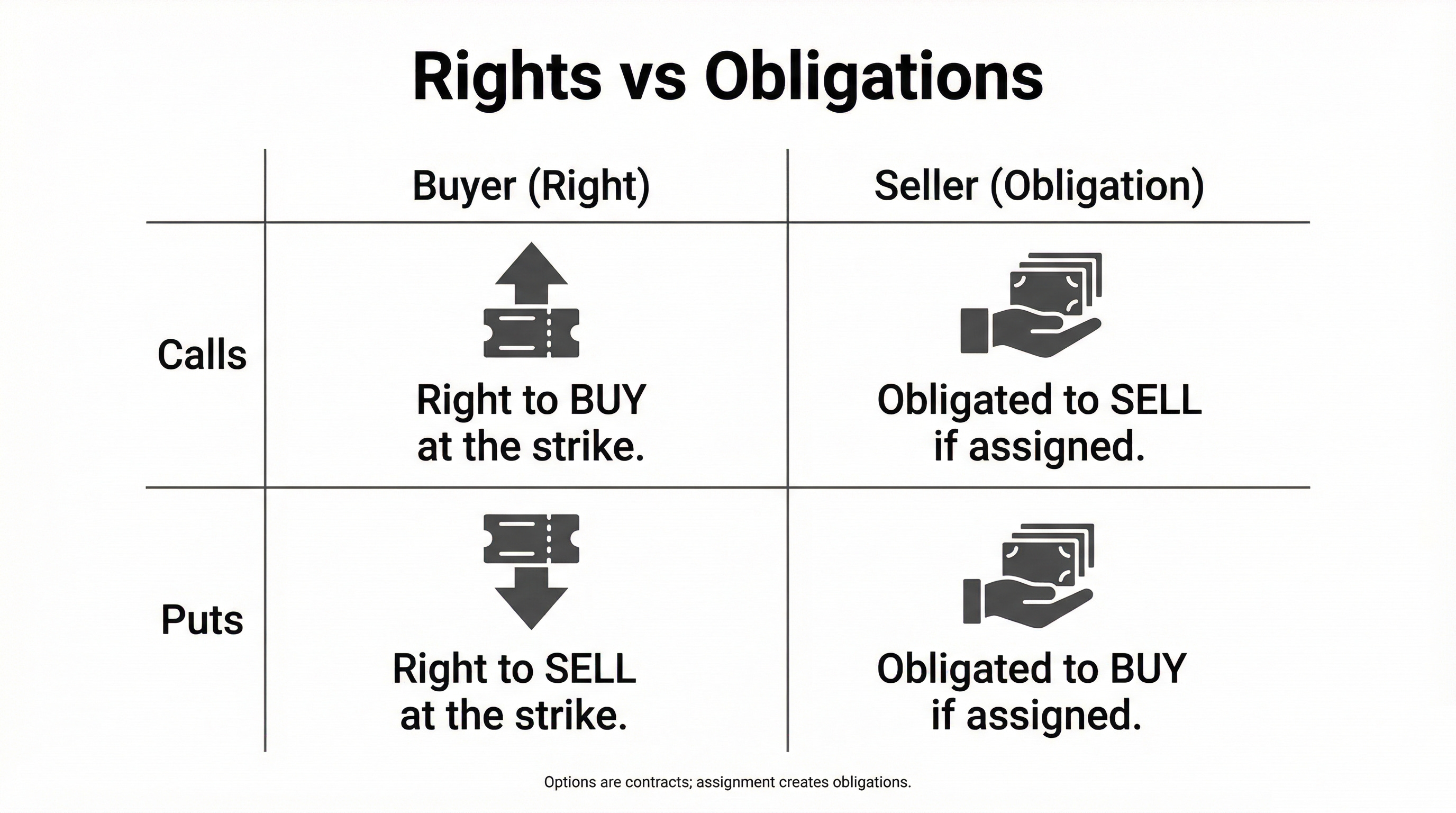

Options are just contracts with a clock on them. A call gives the buyer the right (not the obligation) to buy an underlying asset at a fixed strike price by expiration; a put gives the buyer the right to sell. The seller (writer) is on the other side: they take cash up front (the premium) and accept the obligation that comes with it if they get assigned. Most equity options are for 100 shares per contract, so everything is “per share” in quotes, but “x100” in real dollars.

Below is a practical, beginner-friendly mental model for the four core positions, the Greeks that matter most early on, and the most common “first strategies” people try (with the usual ways they get cooked).

1) The four basic option trades (and their payoff shapes)

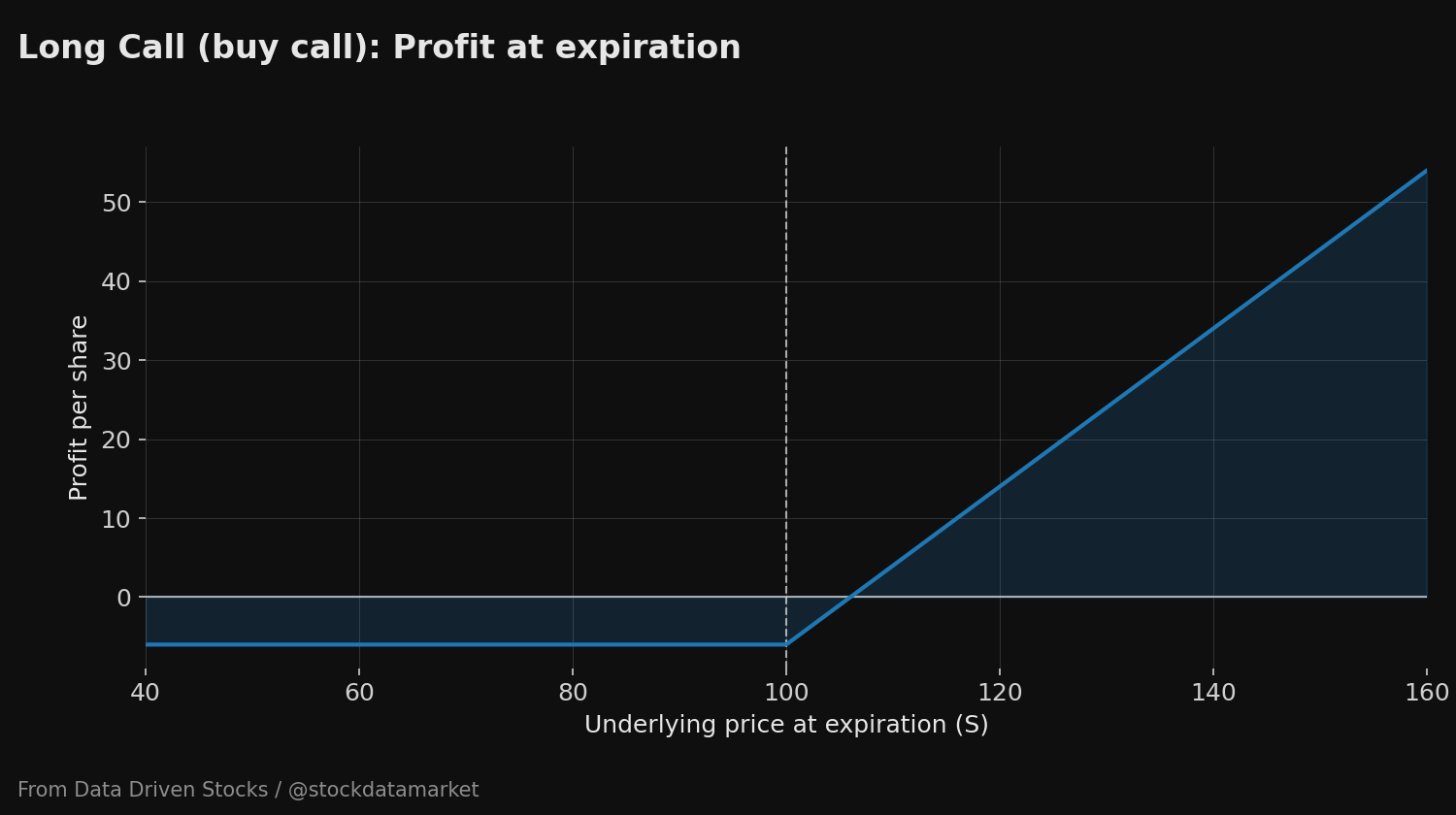

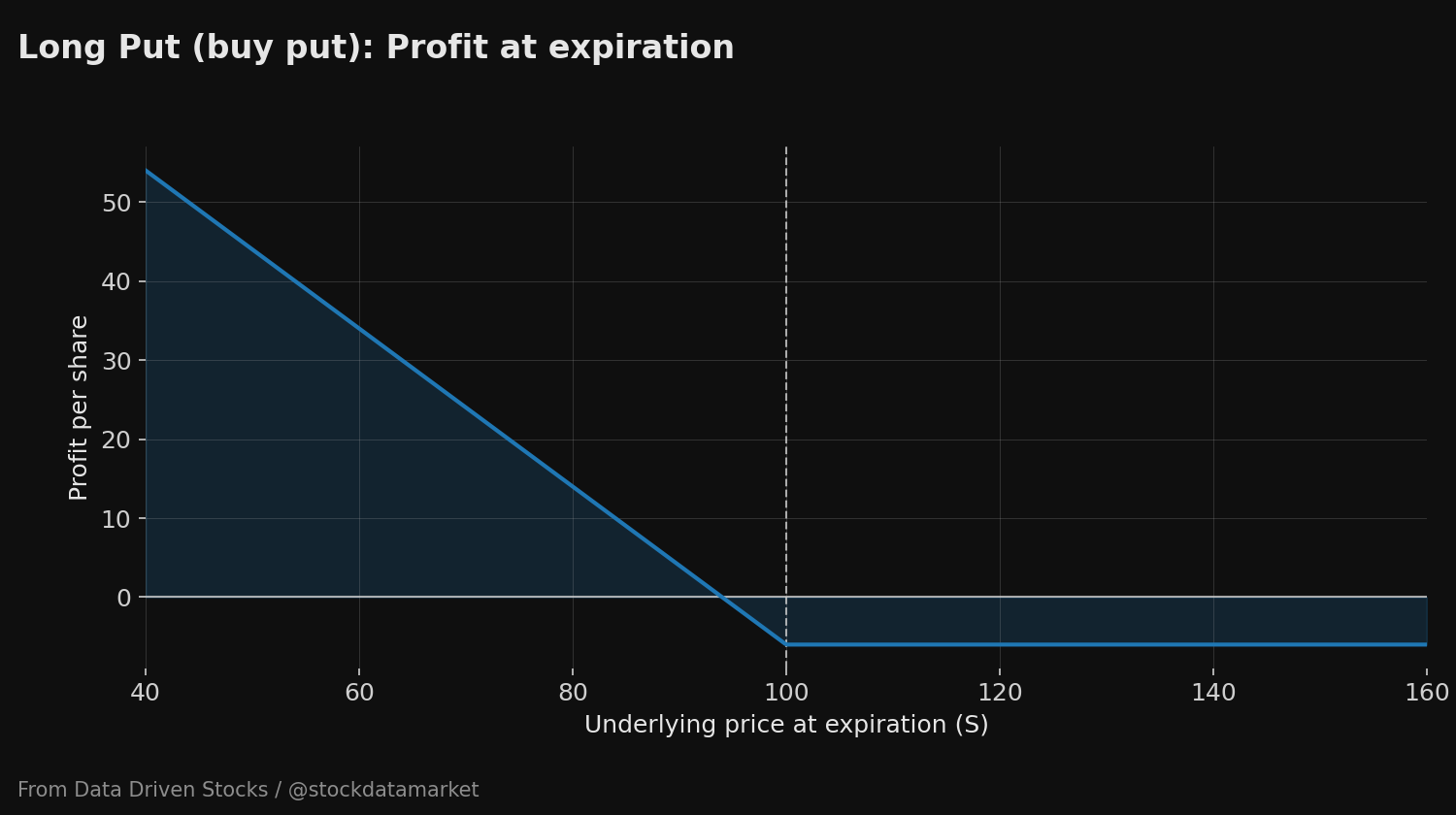

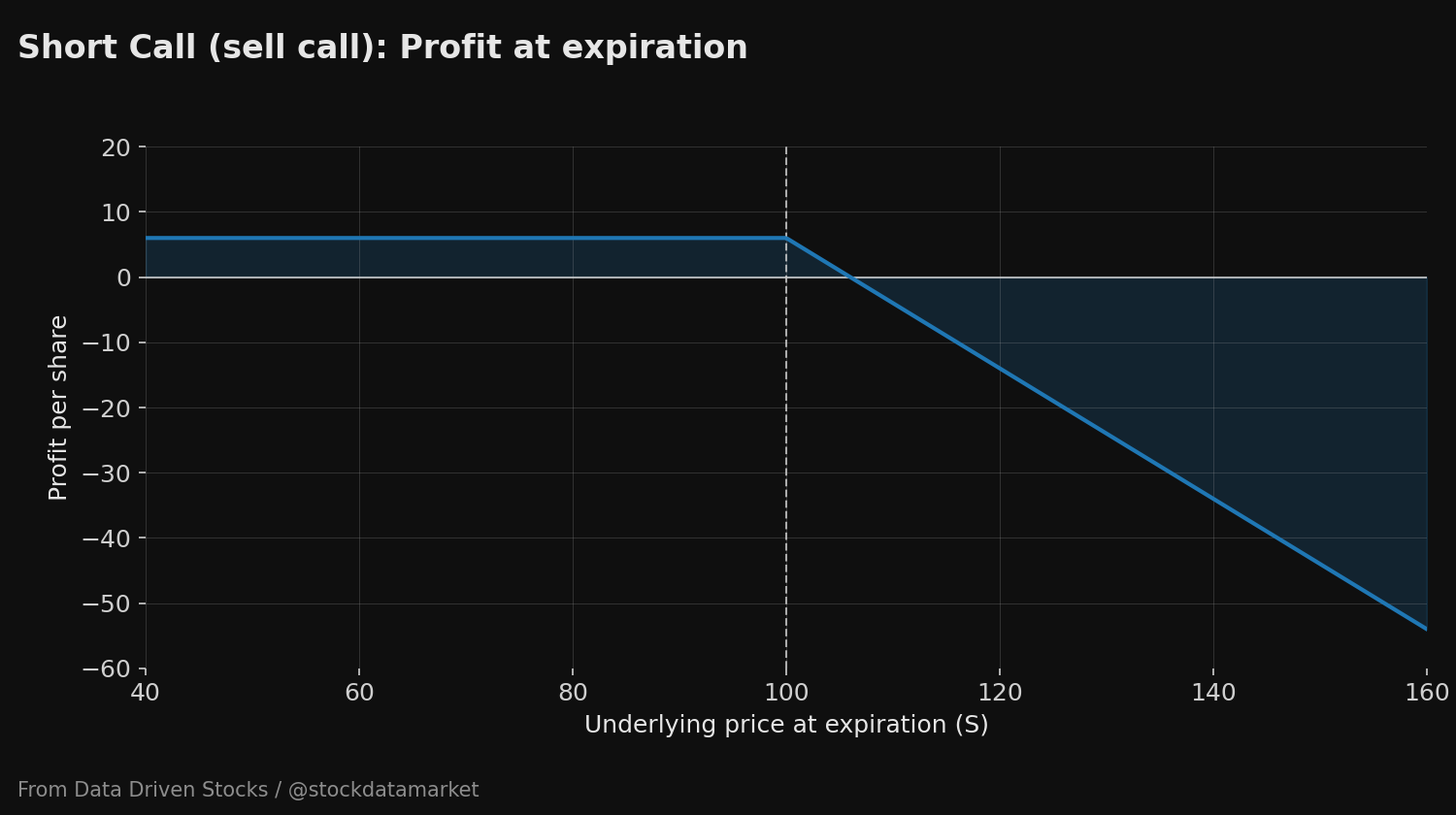

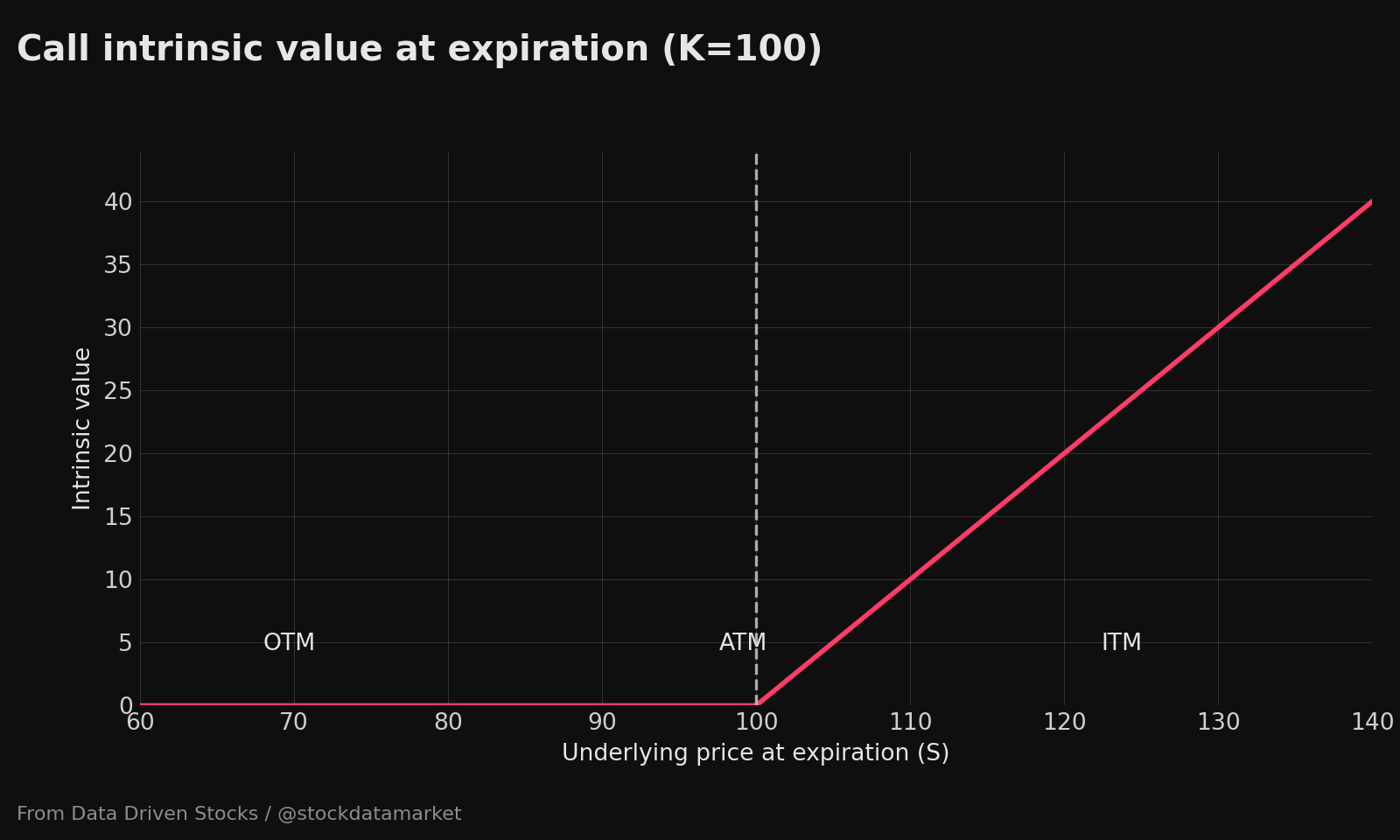

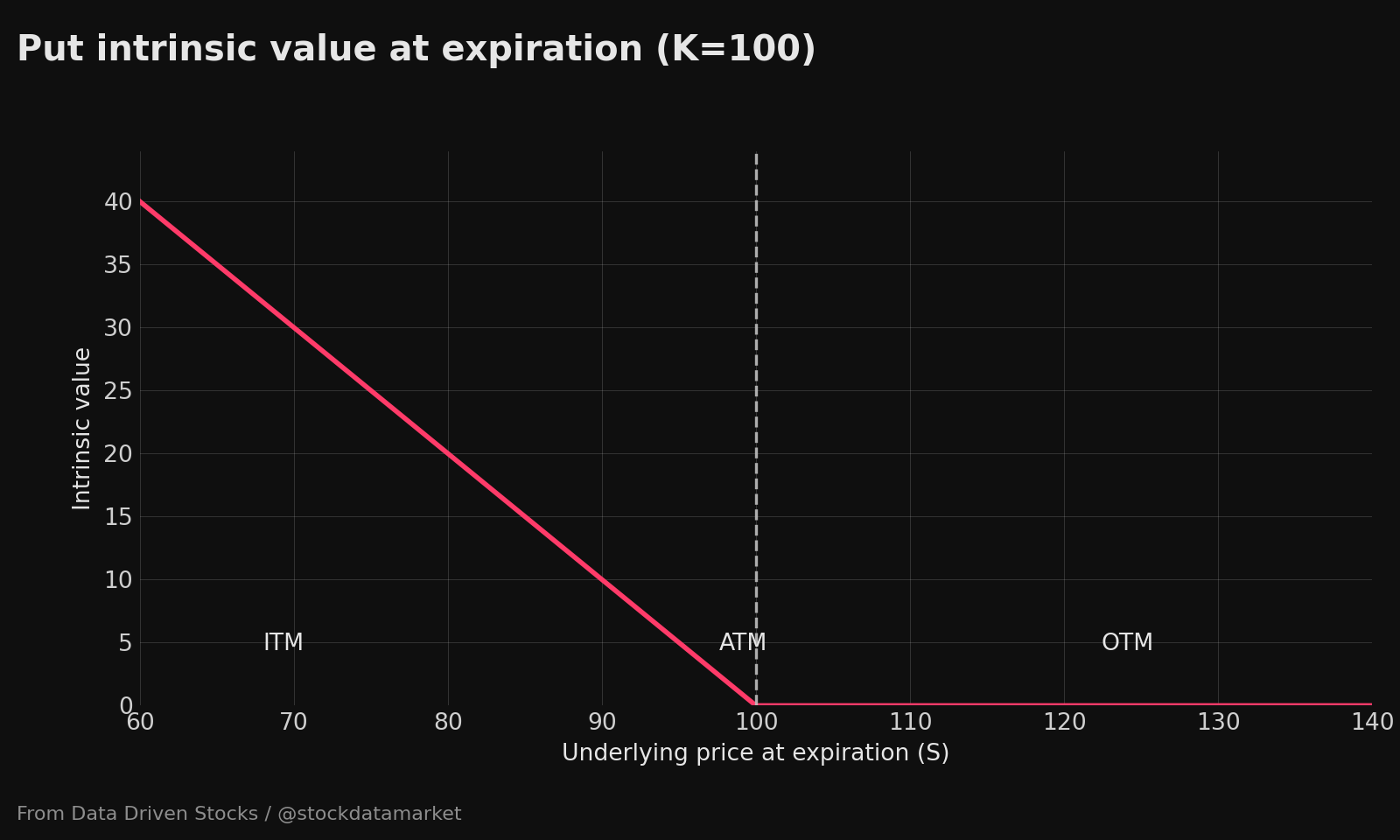

The cleanest way to learn options is to look at the profit at expiration as a function of the underlying price. These payoff graphs ignore early closing, changing implied volatility, and time value before expiration. That’s a feature, not a bug: it lets you see the bones.

A long call is the “I want upside” trade. Your max loss is the premium you paid. Your upside grows as the underlying rises above the strike, and your breakeven at expiration is strike + premium.

A long put is the “I want downside” trade. Your max loss is the premium. Your profit grows as the underlying falls below the strike, and your breakeven is strike − premium.

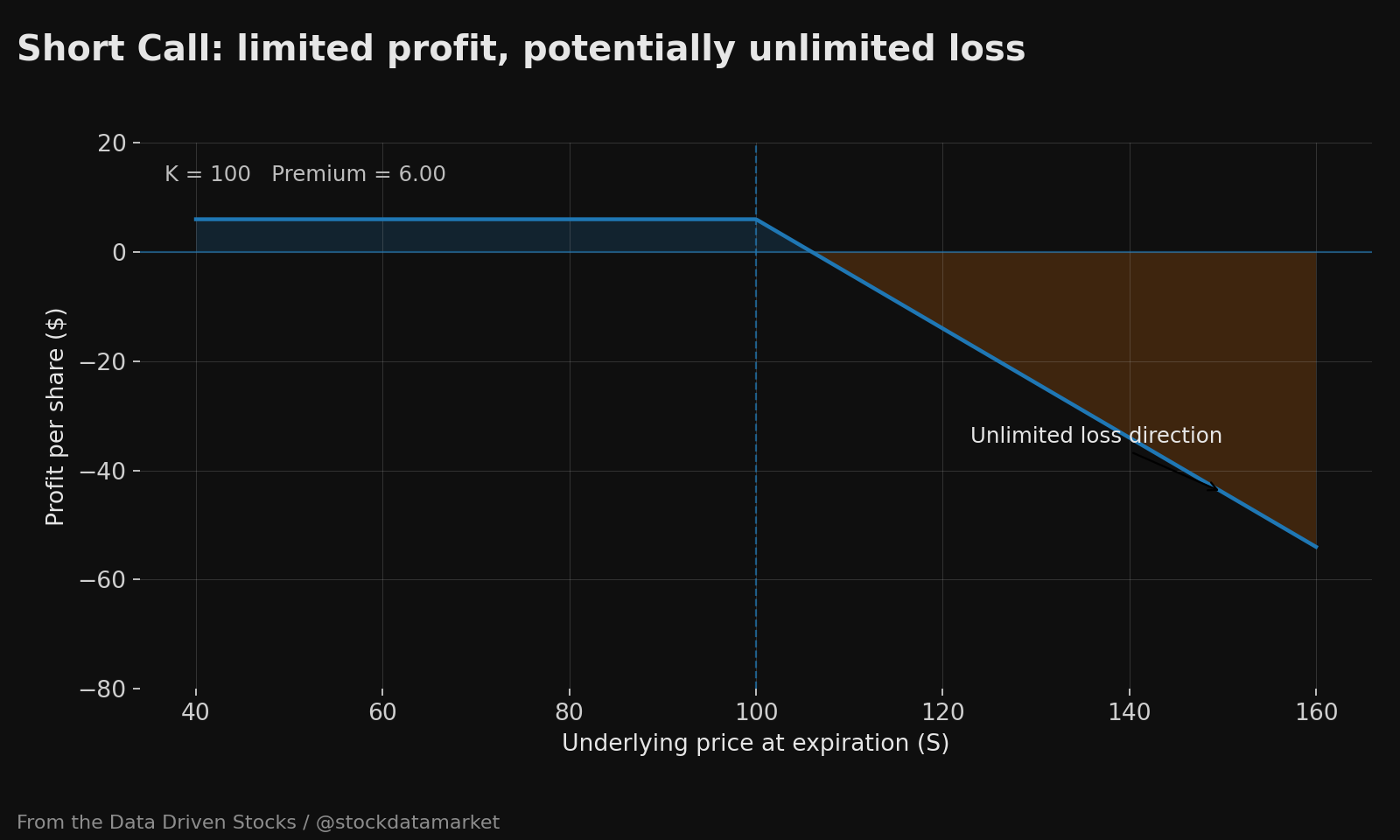

A short call is the “I’ll sell you upside” trade. You keep the premium if the option expires worthless, but if the underlying rips higher you can face very large losses; for an uncovered (naked) short call, the potential loss is unlimited.

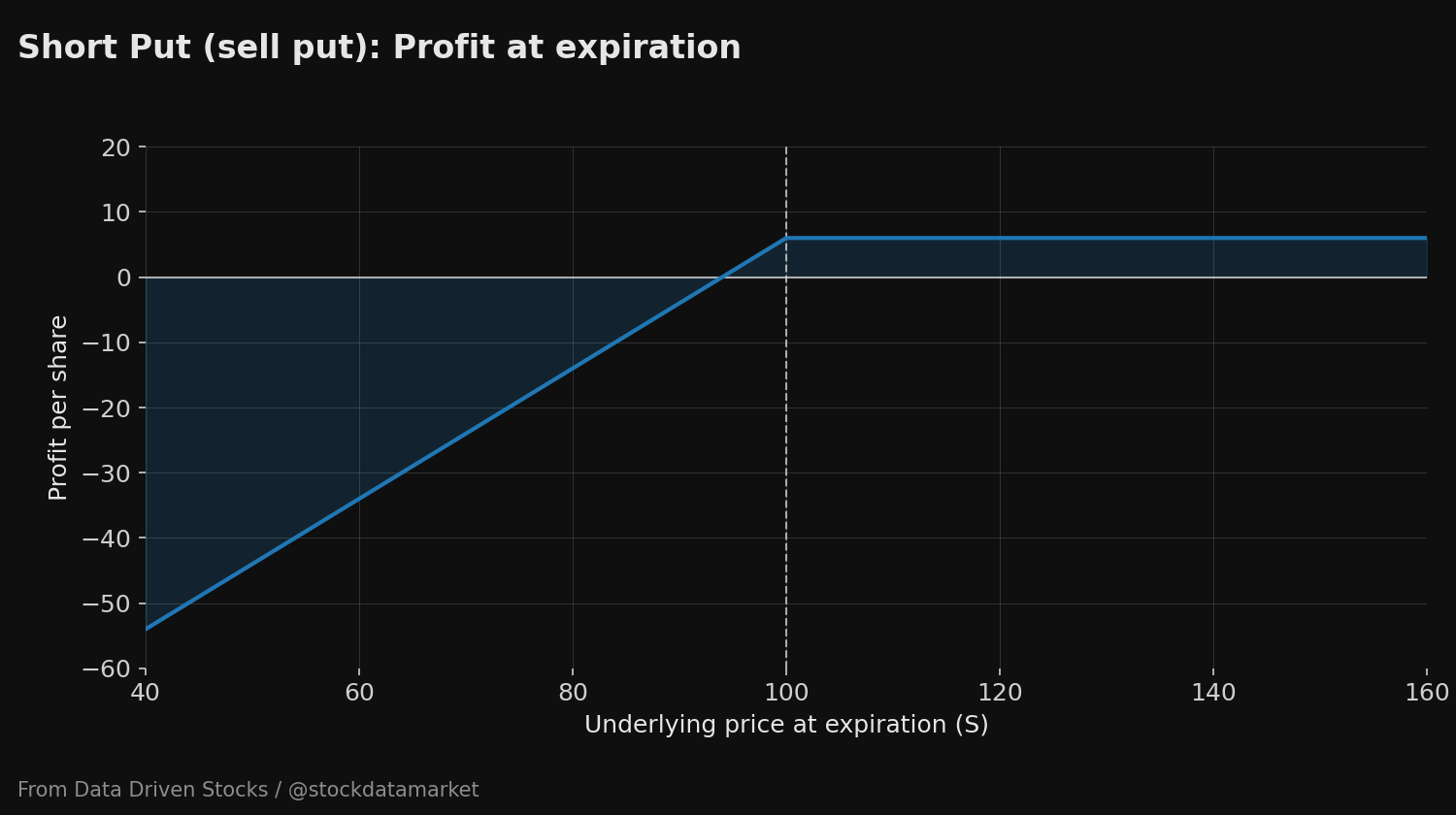

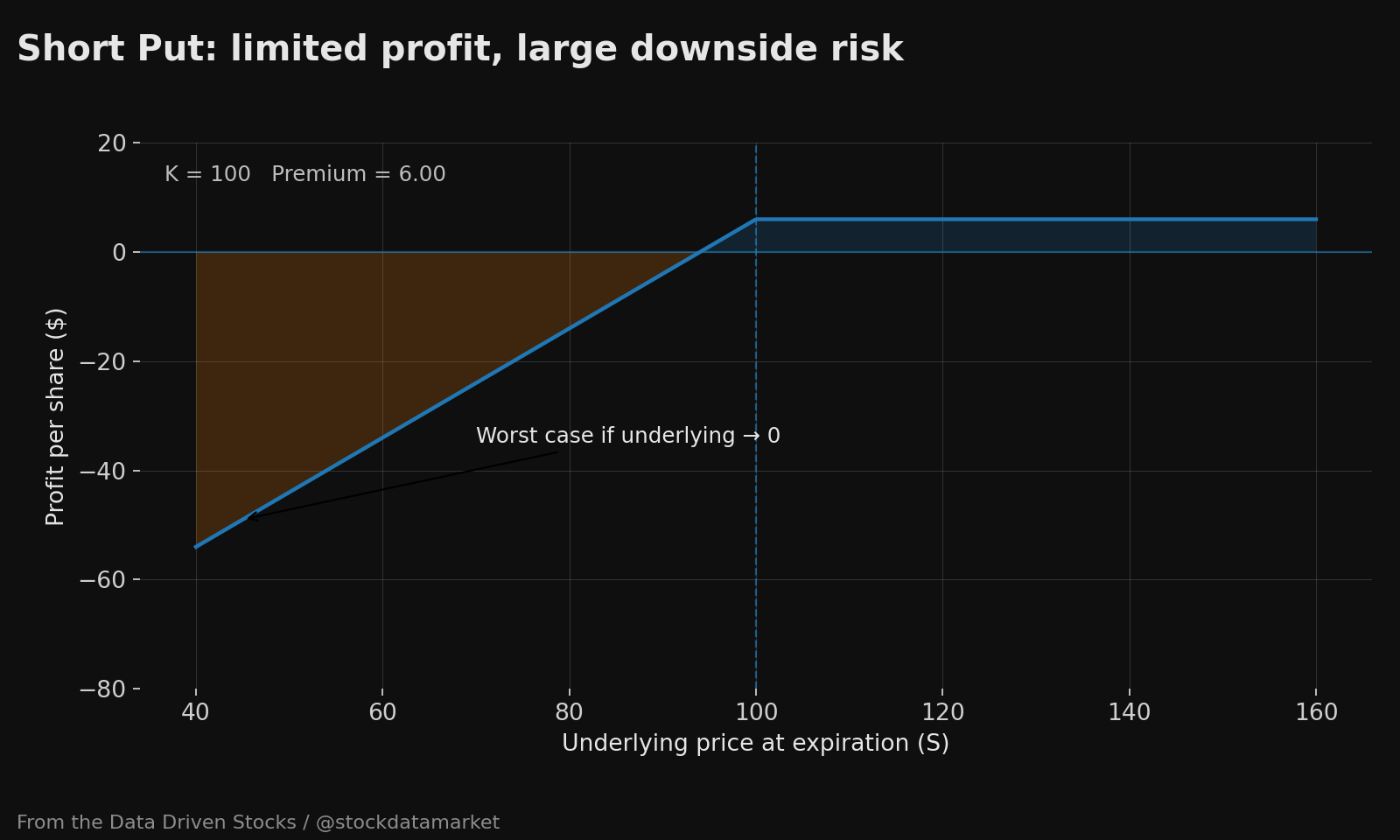

A short put is the “I’ll sell you downside insurance” trade. You keep the premium if the option expires worthless. If the underlying drops, your losses can be large; for a put writer, the underlying can fall to zero, and you may be assigned and required to buy shares at the strike.

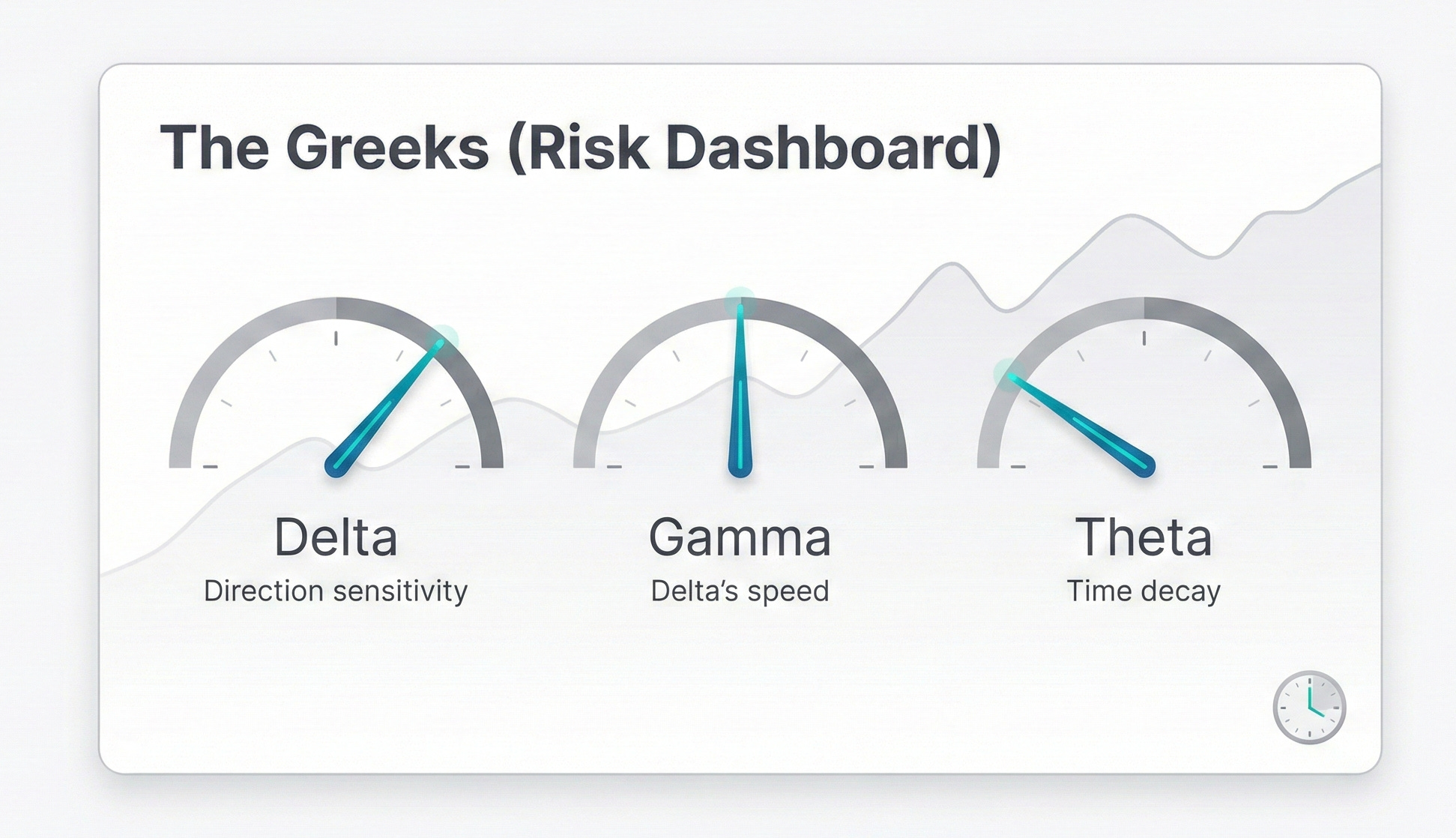

Delta, Gamma, Theta: the three Greeks you actually feel in your P&L

You can learn a lot of options without being a quant, but you do need the “three body blows”:

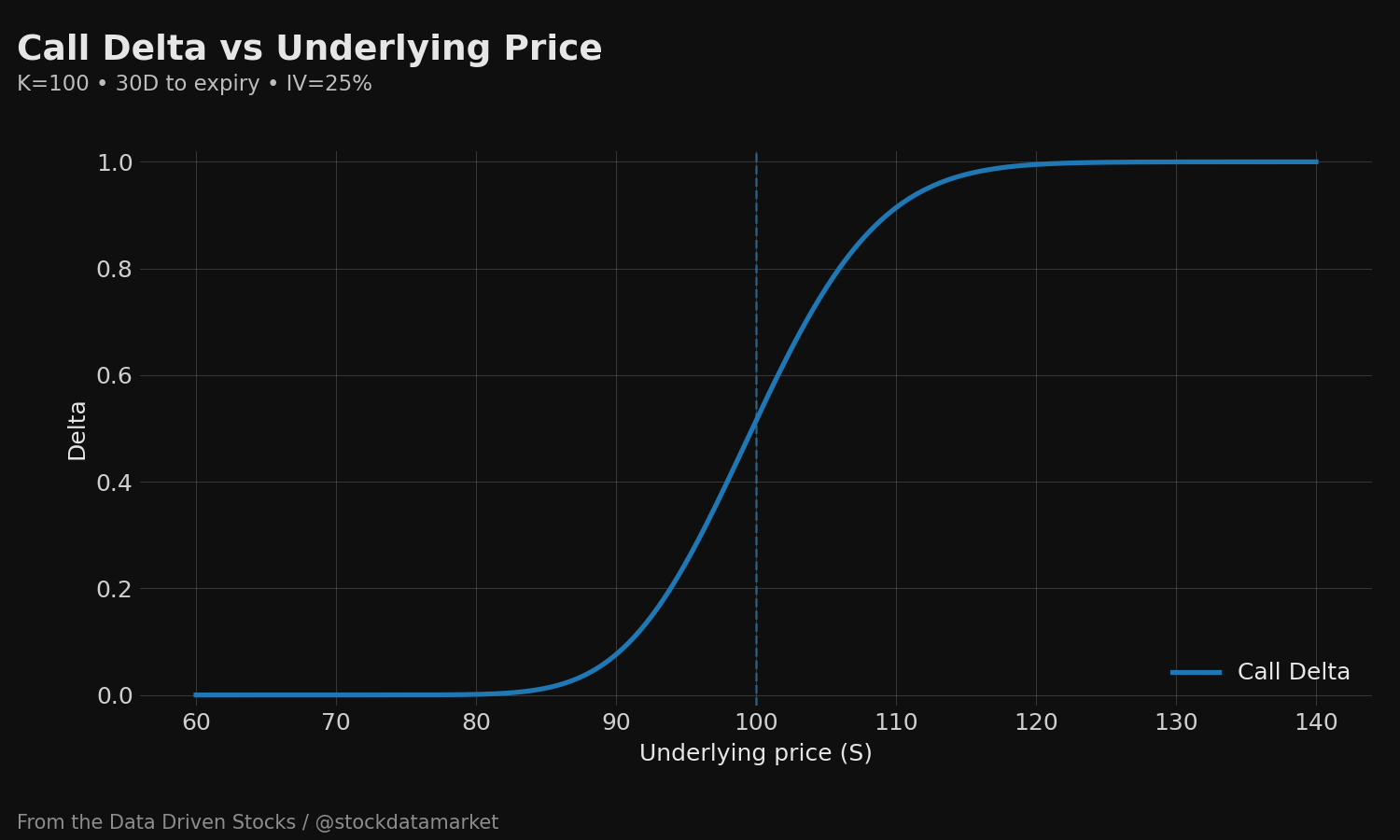

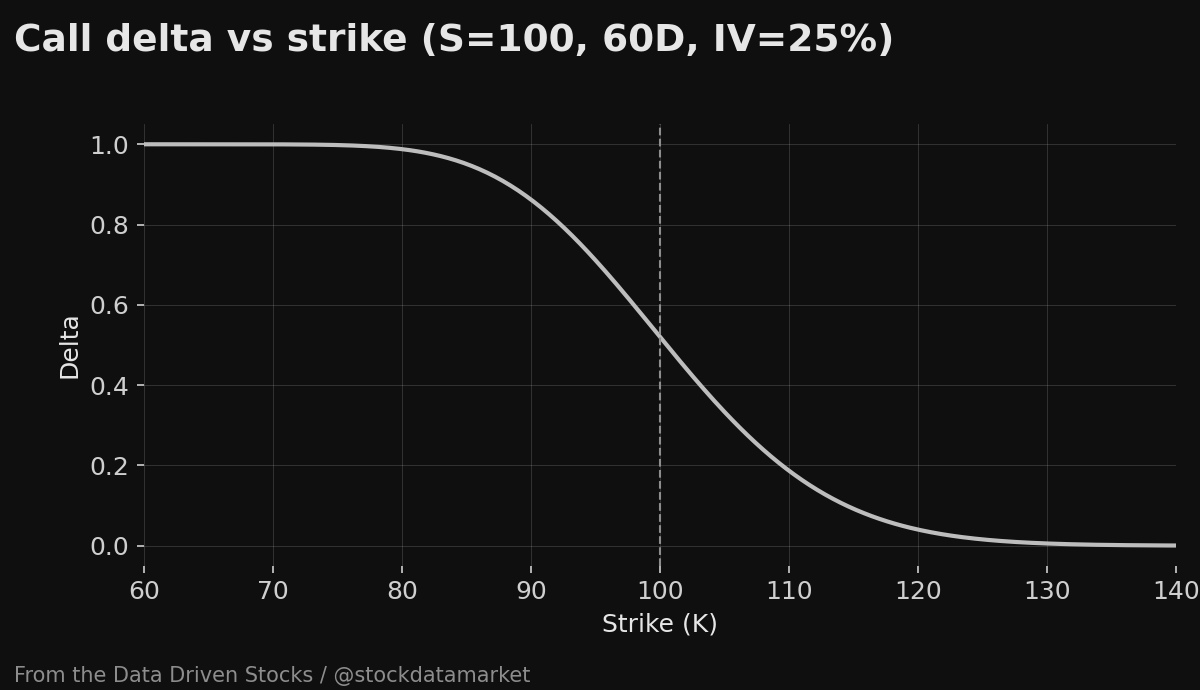

Delta is the “direction exposure.” It estimates how much the option price changes for a $1 move in the underlying. Calls have positive delta; puts have negative delta. Deep in-the-money calls often have deltas that move toward 1, meaning they start behaving more like stock.

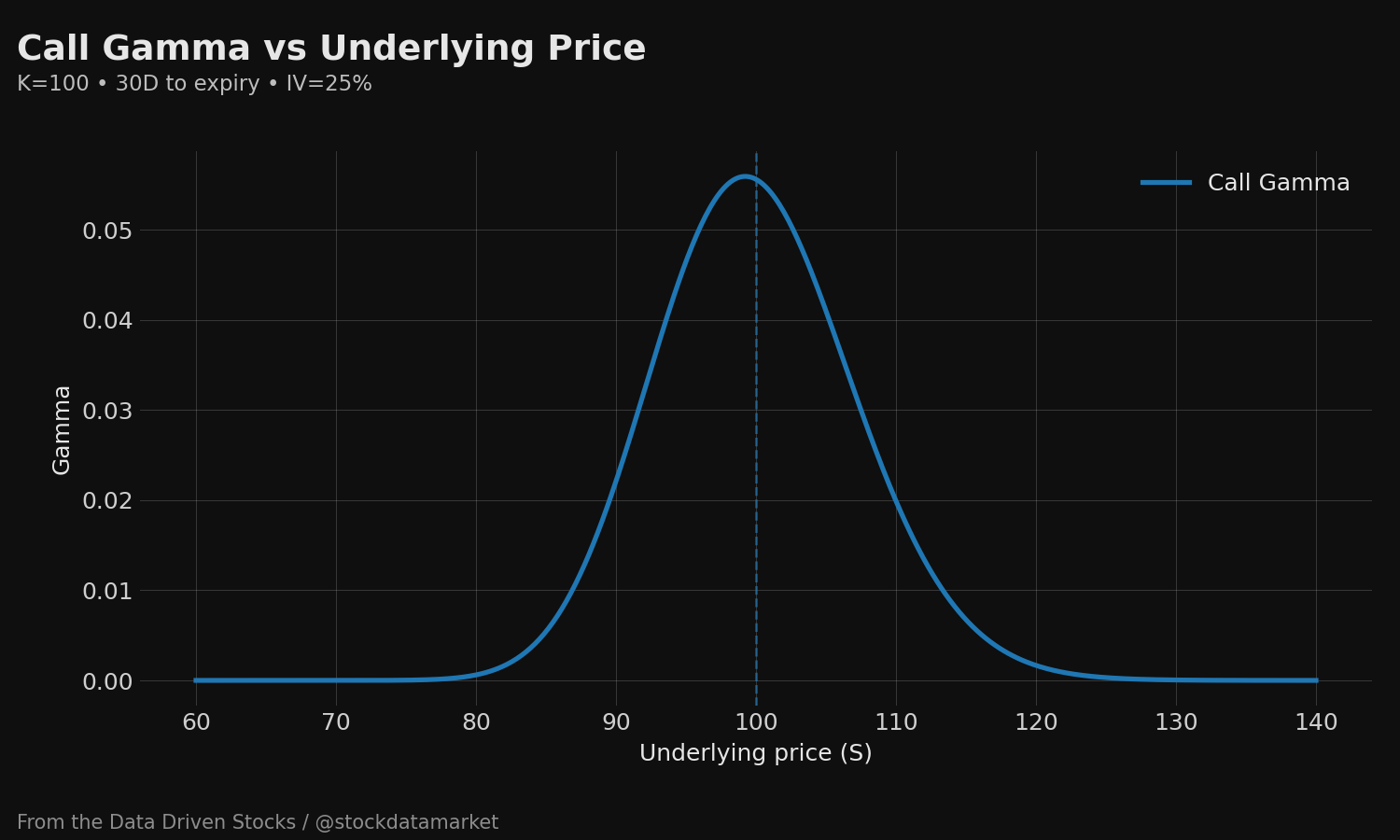

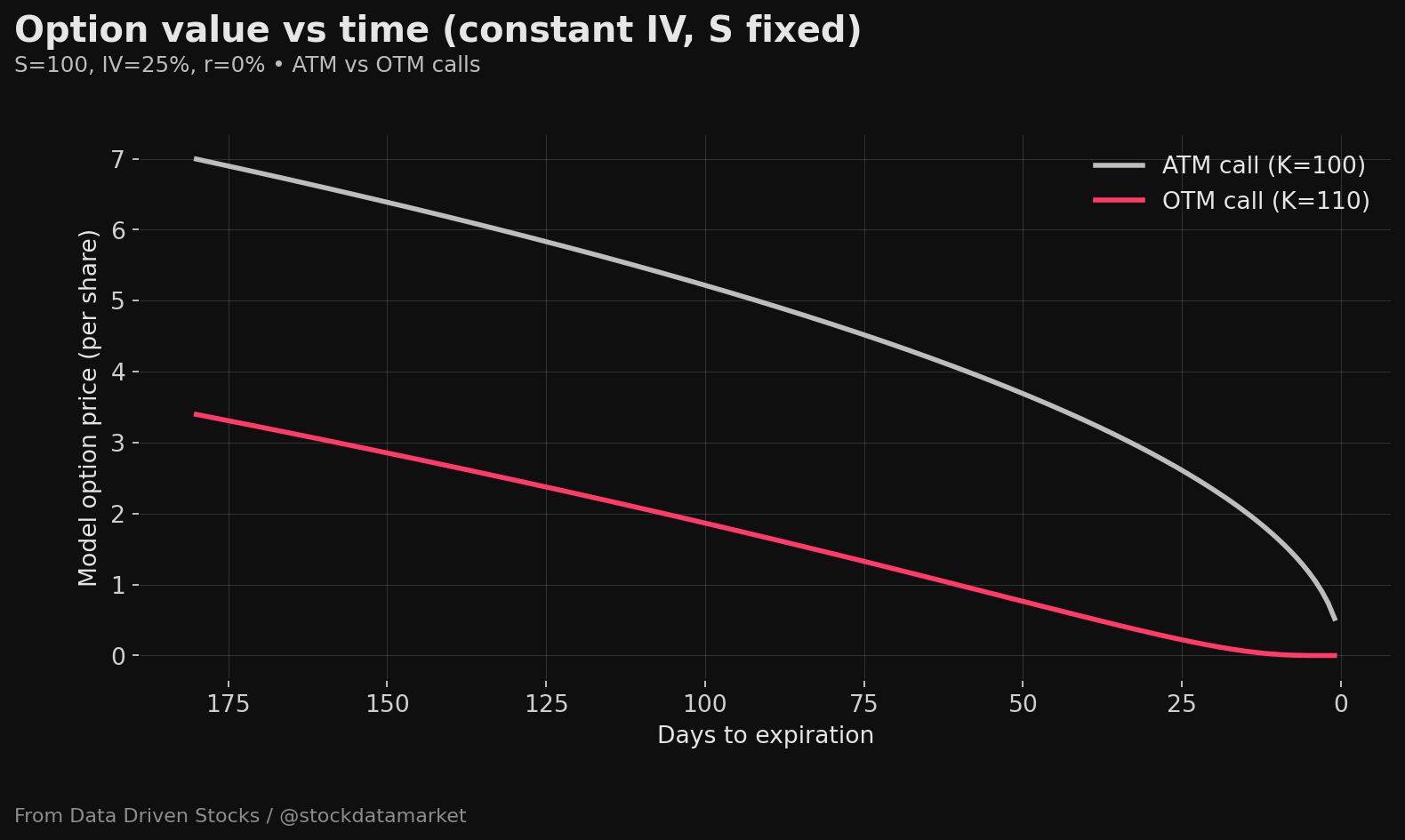

Gamma is “how fast delta changes.” Gamma tends to be highest near at-the-money, especially close to expiration. That’s why near-expiration ATM options can feel like they go from “meh” to “holy ****” in a hurry.

Theta is the “rent you pay to own optionality.” Options are wasting assets; time value tends to decay faster as expiration approaches, and ATM options tend to have the most exposure to that decay. If nothing happens, theta still does.

OTM, ATM, ITM: what “moneyness” actually means

Moneyness is just where the underlying price is relative to the strike.

For a call, if the stock is above the strike, it’s in-the-money; below the strike, it’s out-of-the-money; right at the strike is at-the-money.

For a put, it’s the mirror image: below the strike is in-the-money; above is out-of-the-money; at the strike is at-the-money.

2) Now the “first strategies” people actually trade

You can combine calls and puts into all kinds of spreads, hedges, and structures. But the strategies below are the ones most beginners bump into first, because they’re simple and emotionally loud.

3) Long OTM calls/puts: cheap lotto tickets with a time tax

Buying OTM options feels great because the premium is smaller and the upside looks huge. The catch is that you’re paying for time value, and if the move doesn’t happen fast enough, theta can grind the option down even if you’re “kinda right.” Premiums also depend on implied volatility; in higher implied volatility environments, options tend to have more time premium, which can make buying feel like paying surge pricing.

One practical takeaway: if you insist on buying OTM options, you usually want enough time for your thesis to actually play out. Short-dated OTM buying is where the “I was right and still lost money” stories come from.

4) 0DTE trading: maximum leverage, minimum forgiveness

0DTE options expire the same day. That means very little time value is left, and the remaining premium can evaporate quickly if price doesn’t move hard and fast. When you buy 0DTE, “going to zero” is not a freak accident; it’s a common outcome when an option finishes OTM.

Can 0DTE be profitable? Sure. But it’s a tool for specific situations, like trying to express a view on an intraday move with defined risk. If you’re not deliberately trading volatility and timing, 0DTE is basically you trying to speedrun time decay.

If you want a clean mental rule: the shorter the option’s life, the more your P&L becomes a race between price movement and the clock.

5) Long ATM calls/puts: where things are most sensitive

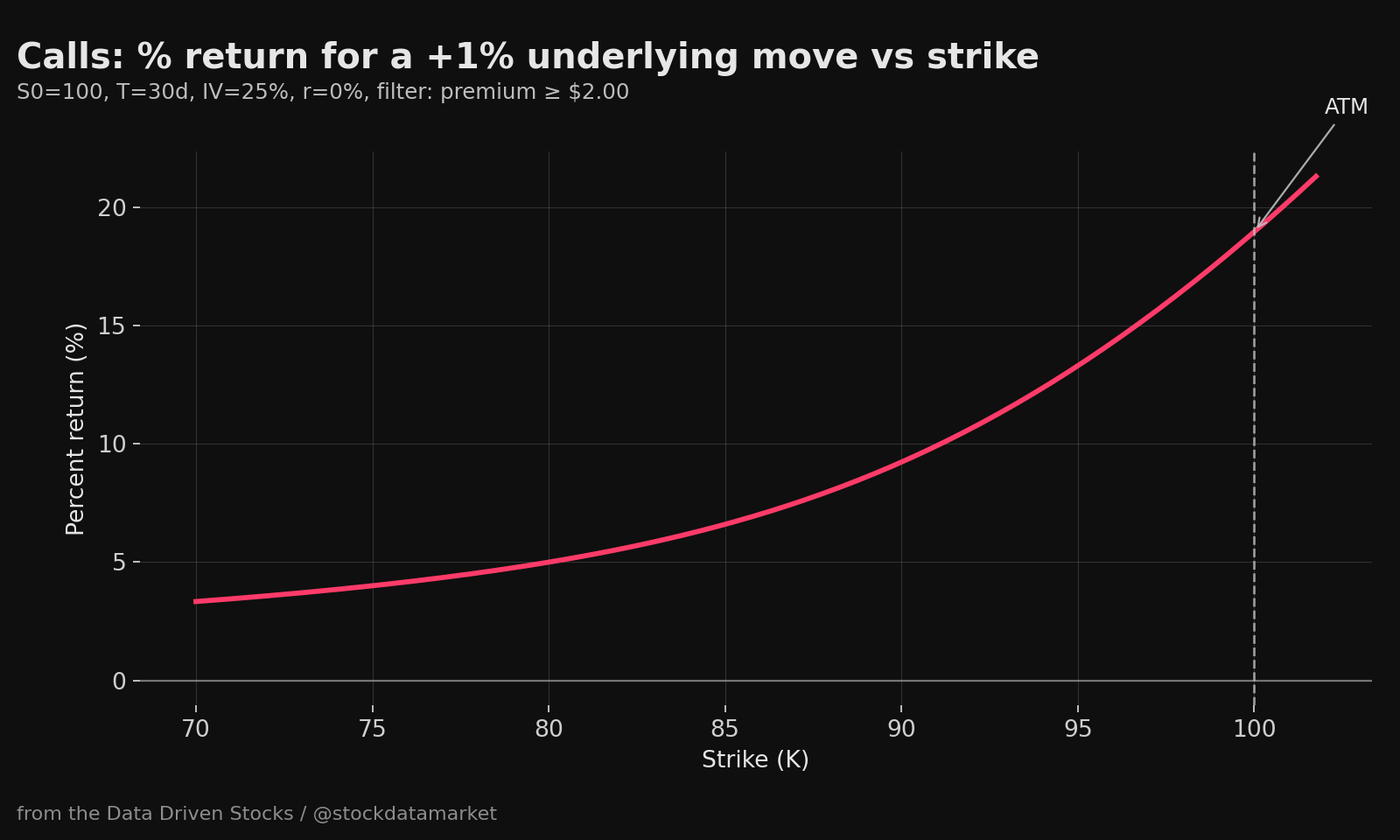

ATM options tend to have the biggest “action” in the Greeks that make options feel like leverage. Gamma is typically highest near ATM, especially near expiration, which means delta can change rapidly as the underlying moves around the strike. That’s the “this thing started moving and then it REALLY started moving” experience.

A practical way to visualize leverage is to ask: “If the stock pops a little, which strike gives the biggest percentage jump in option price?” For options with meaningful premium (not ultra-cheap far OTM), that tends to peak near ATM or slightly OTM.

6) Shorting OTM puts/calls: harvesting theta… while respecting the tail risk

Selling options is the opposite mindset. You collect premium up front and you benefit from time decay, but you accept obligations if assigned. This is where many traders talk about “high probability” and “theta harvesting,” and that can be true in the narrow sense that many options expire worthless.

But the official risk disclosures are blunt: uncovered call writing can involve unlimited losses, and put writing can involve substantial losses (down to the underlying going to zero). On top of that, short option writers may face margin requirements and margin calls that can increase when the market moves against them, and brokers can liquidate positions if margin isn’t met.

There is also a mechanical risk beginners underestimate: assignment turns your option position into stock exposure. A short put can force you to buy shares at the strike. A short call can force you to sell shares at the strike (or be short shares if you don’t own them).

7) Long ITM calls/puts: “stock-like” behavior with built-in risk limits

ITM options are the “less flashy, more practical” end of the spectrum. They cost more than OTM options because they contain intrinsic value, but they often have less exposure to time decay than ATM options, and their delta can be high. Deep ITM calls often have delta moving toward 1, which is why they’re sometimes used as a stock substitute: you can get stock-like exposure with less capital than buying 100 shares outright.

The key nuance is leverage math. Delta near 1 means the option’s dollar change can resemble the stock’s dollar change. Your percentage return depends on how much premium you paid. If you pay $30 for a deep ITM call and the underlying rises $1, the call might rise roughly about $1 (delta ≈ 1), which is around a 3.3% move on the option for a 1% move on a $100 stock. That’s leverage, just not magic.

The big risk is still direction: if the underlying drops enough, an ITM option can lose intrinsic value and slide toward ATM/OTM territory, where losses can accelerate. The good news is the loss on a long option is still limited to the premium paid, even if it expires worthless.

Final reality check (the part everyone skips)

Options pricing is not just direction. Premiums reflect time and implied volatility, and the official disclosures repeatedly emphasize that options can become worthless quickly and that writing options can expose you to very large losses and margin calls. If you want to trade options and survive long enough to get good, treat position sizing like it matters, because it does.