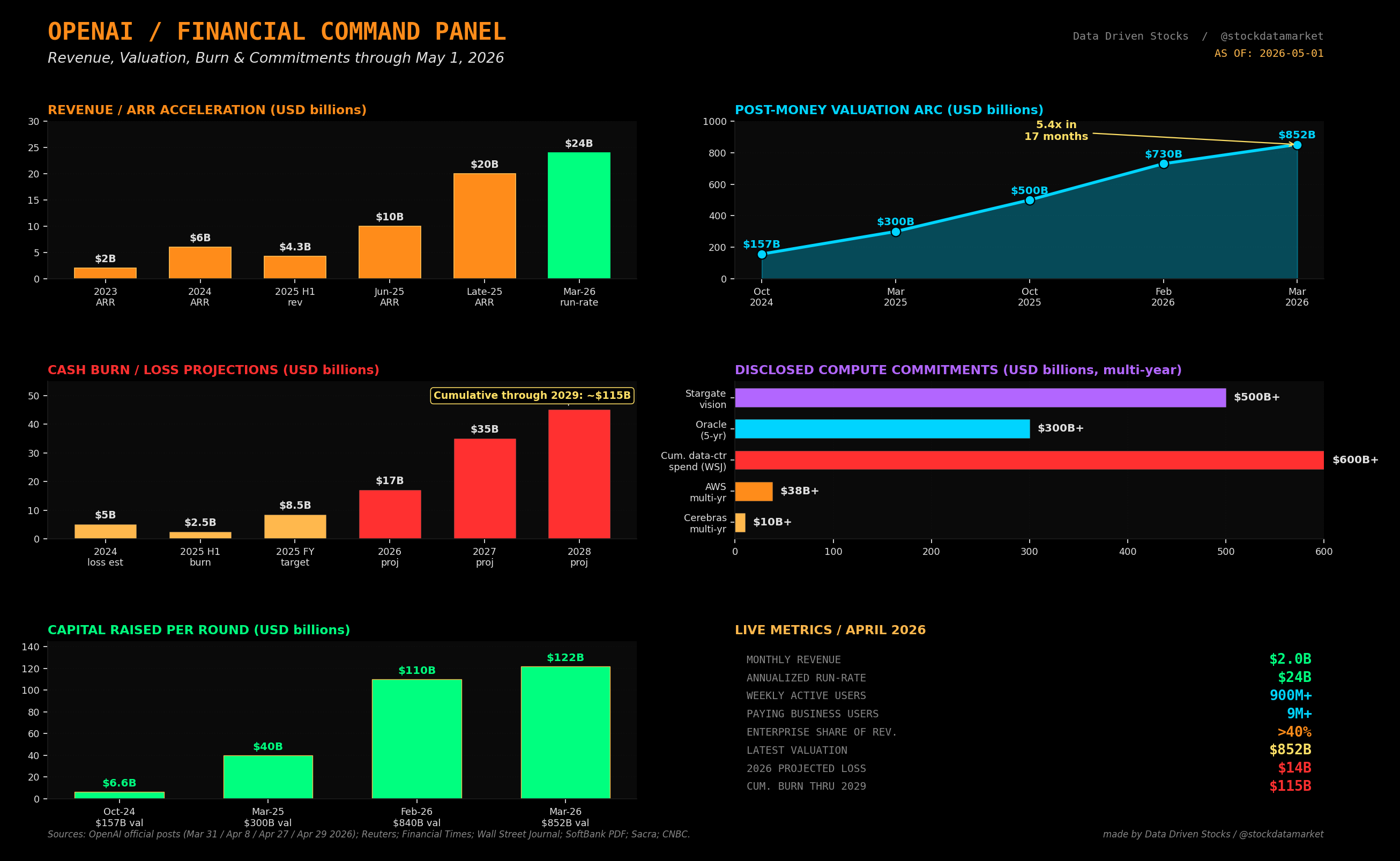

OpenAI’s $852 Billion Paradox: The Most Valuable Startup In History Burns $17 Billion A Year - And Just Raised $122 Billion More

OpenAI’s financial health as of May 1, 2026 - the revenue, the burn, the CAPEX, the changing projections, and whether the flywheel can actually pay for itself before the decade ends.