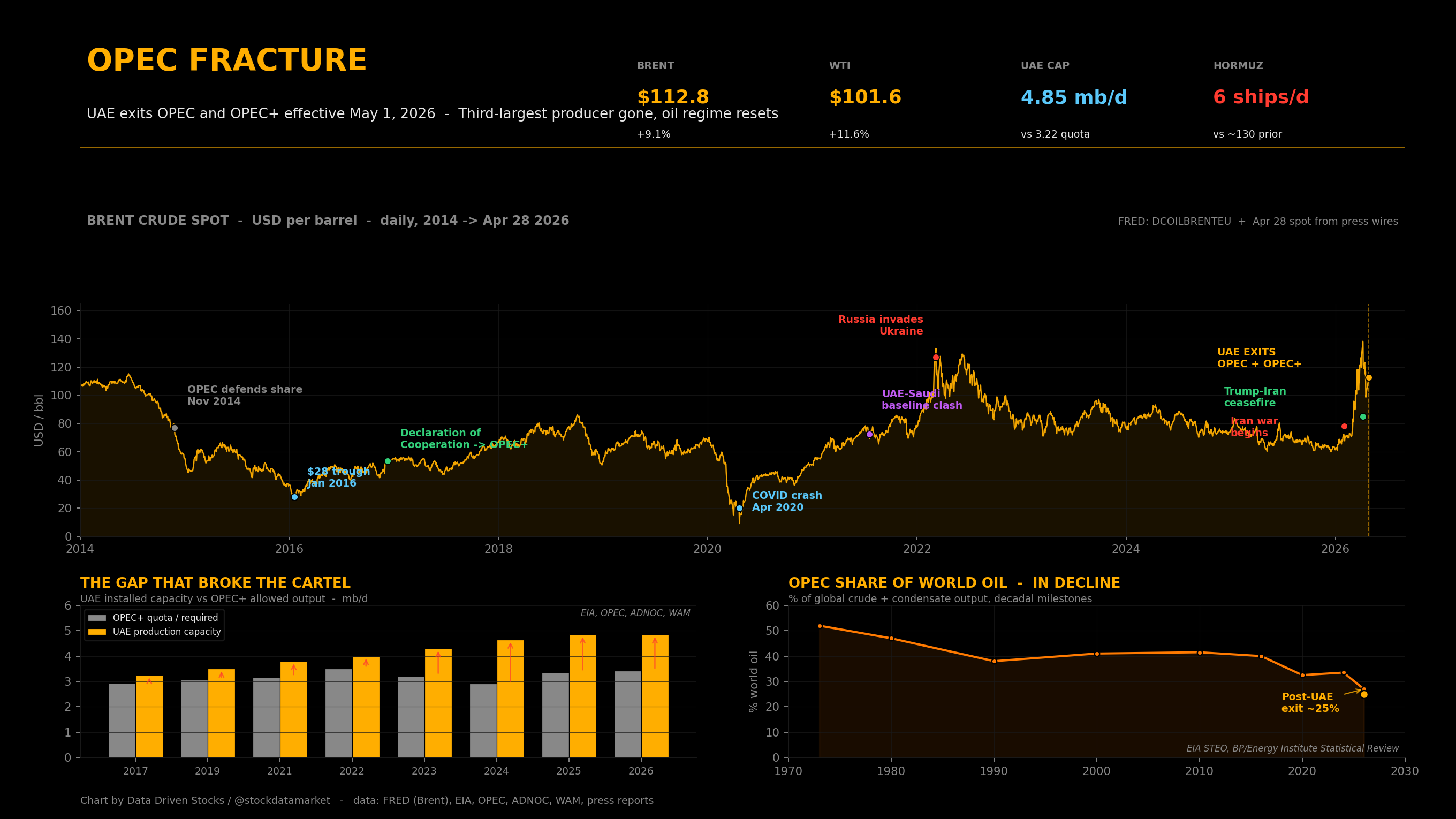

OPEC FRACTURE - Brent crude oil from 2014 through April 28, 2026, with the regime-defining events that bracketed the cartel’s last decade. The bottom-left panel shows the gap between UAE installed ca…

Continue reading this post for free, courtesy of Data Driven Stocks.