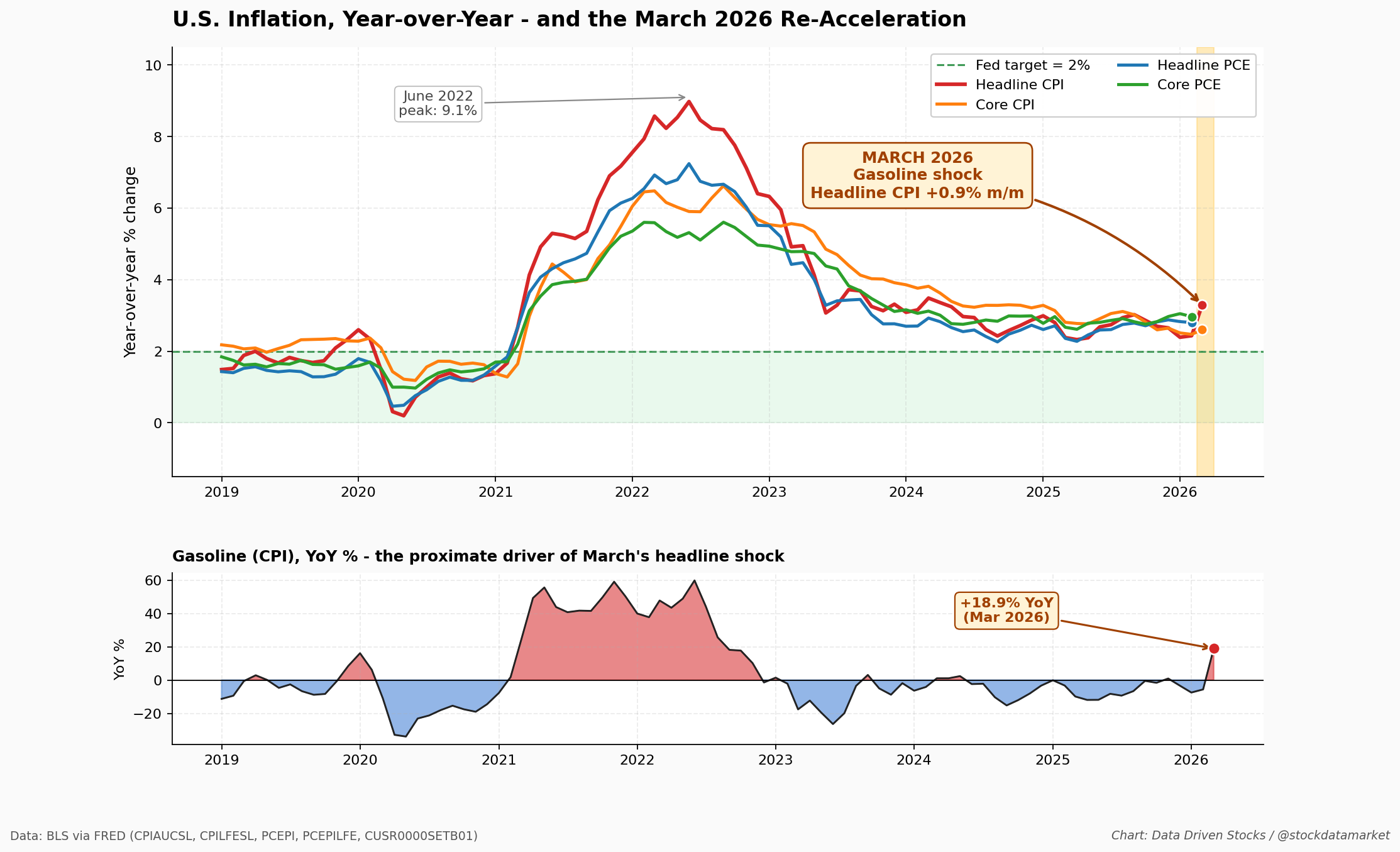

March CPI Just Detonated At 0.9%: Gasoline Did 75% Of The Damage, And Now The Fed Has A Problem

April 2026 inflation data is out, and it’s worse than the past year suggested. The real story isn’t the +0.9% - it’s what’s beneath it and what BLS is warning about next month.