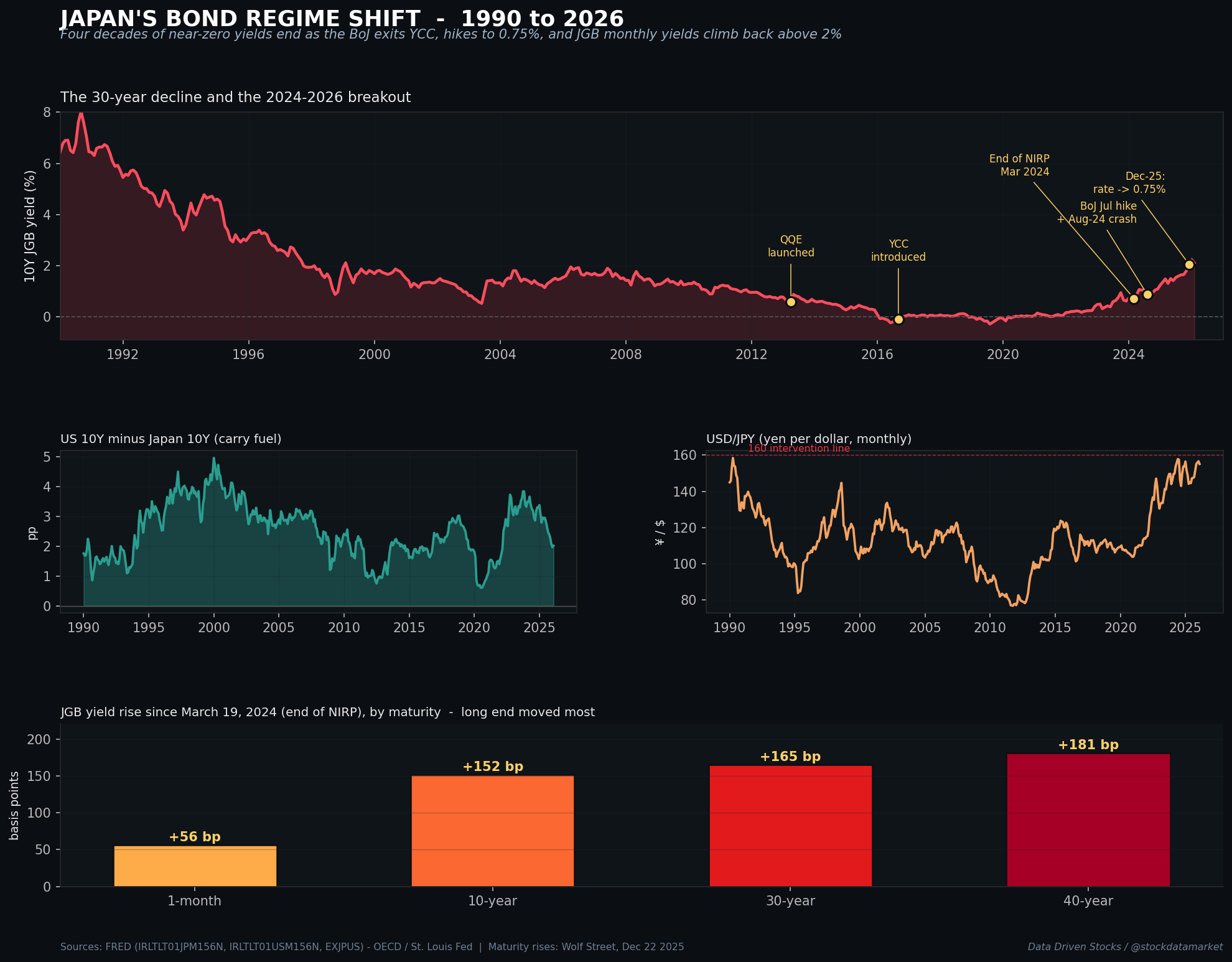

The 30-year decline in Japanese government bond yields ended in March 2024, when the Bank of Japan exited negative rates for the first time in seventeen years. The FRED monthly series shows the 10Y r…

Continue reading this post for free, courtesy of Data Driven Stocks.