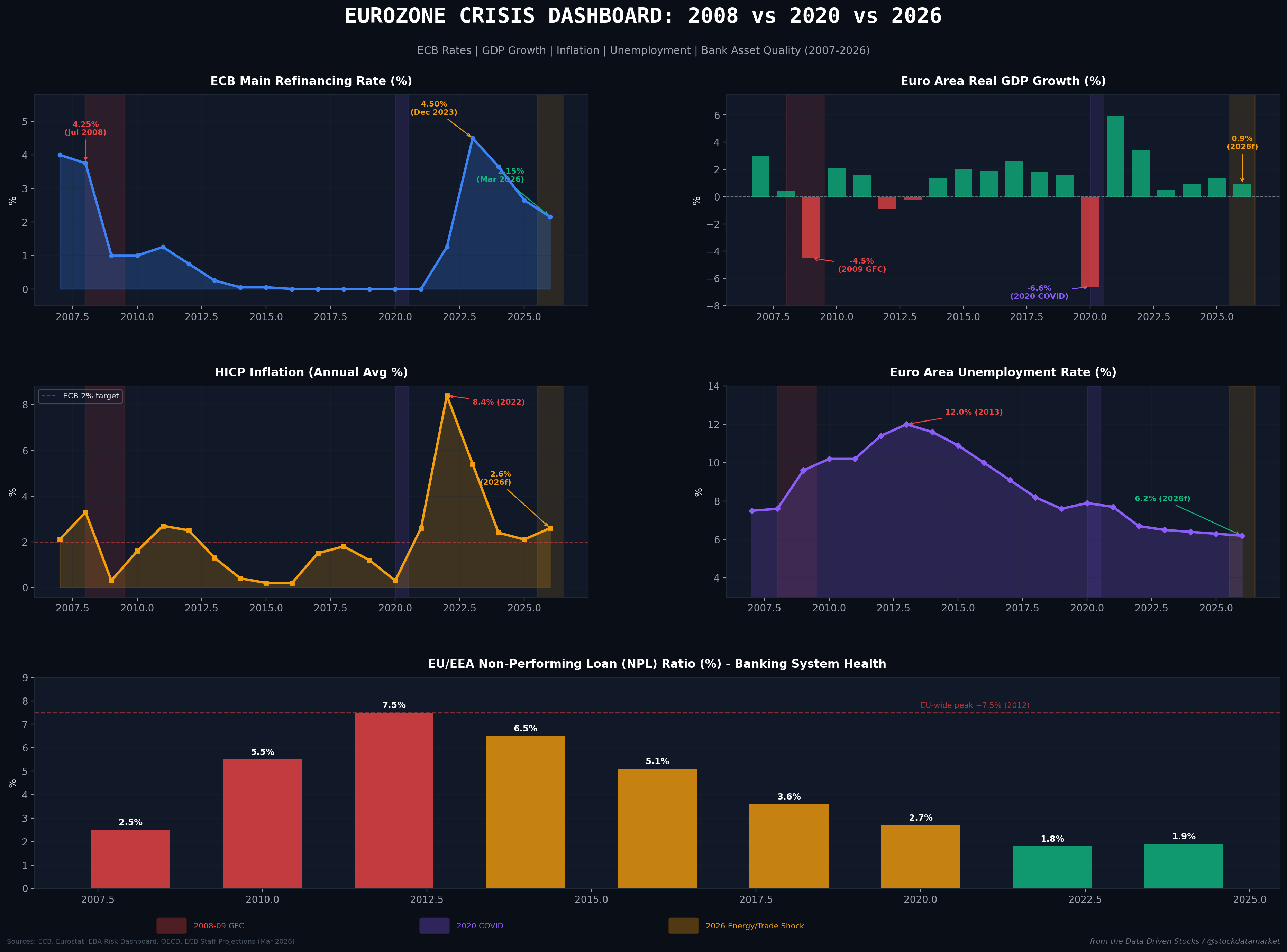

Is the ECB Facing Another 2008? Lagarde’s Crisis Playbook Meets the Worst Energy Shock Since the 1970s

The European Central Bank just froze rates, slashed growth forecasts, and warned of “significantly more uncertain” times. The 2008 comparisons are flying.