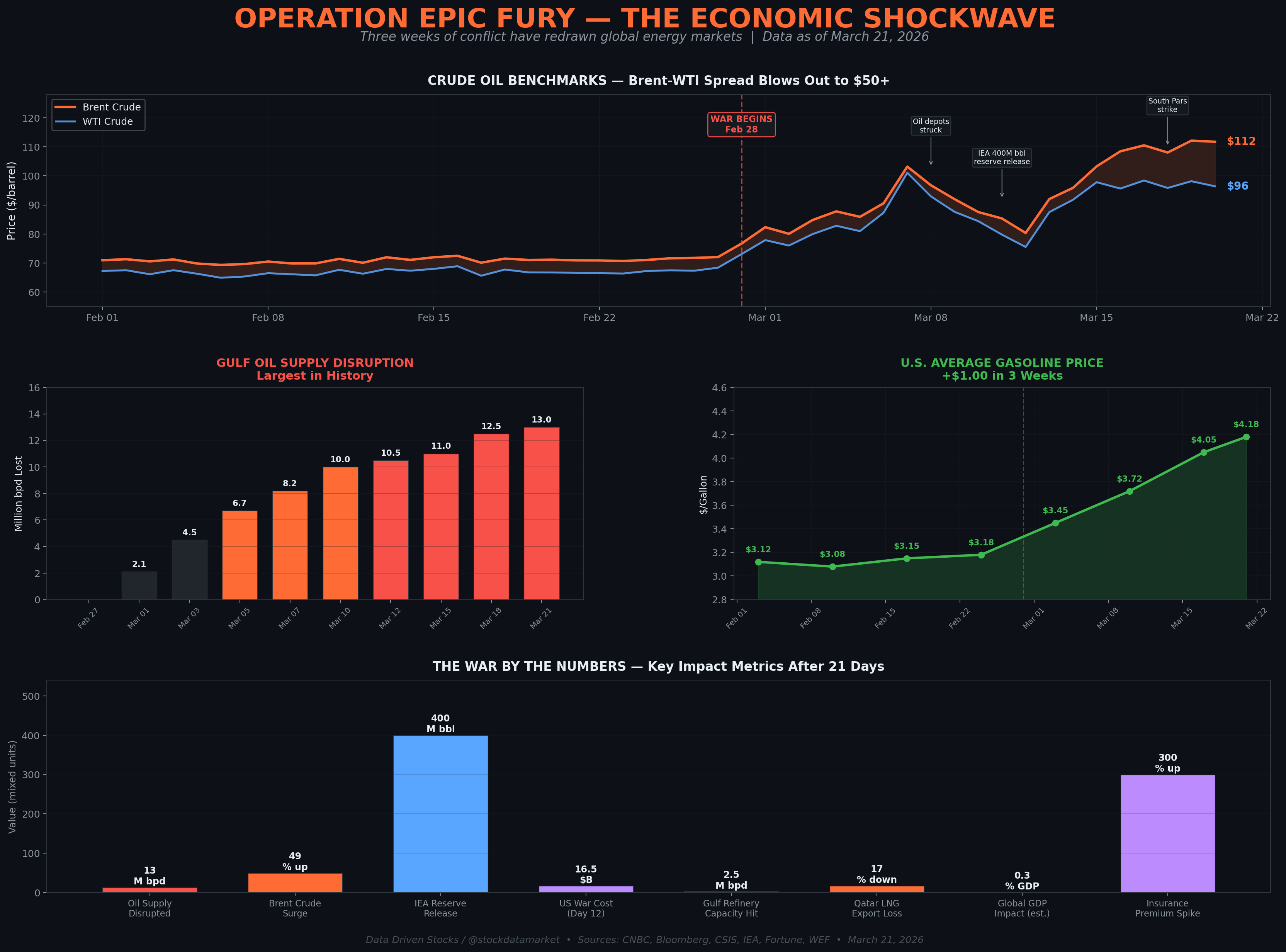

Operation Epic Fury by the numbers — Brent crude has surged over 50%, Gulf oil supply disruptions have exceeded 13 million barrels per day, and U.S. gasoline has climbed a full dollar in three weeks.…

Continue reading this post for free, courtesy of Data Driven Stocks.