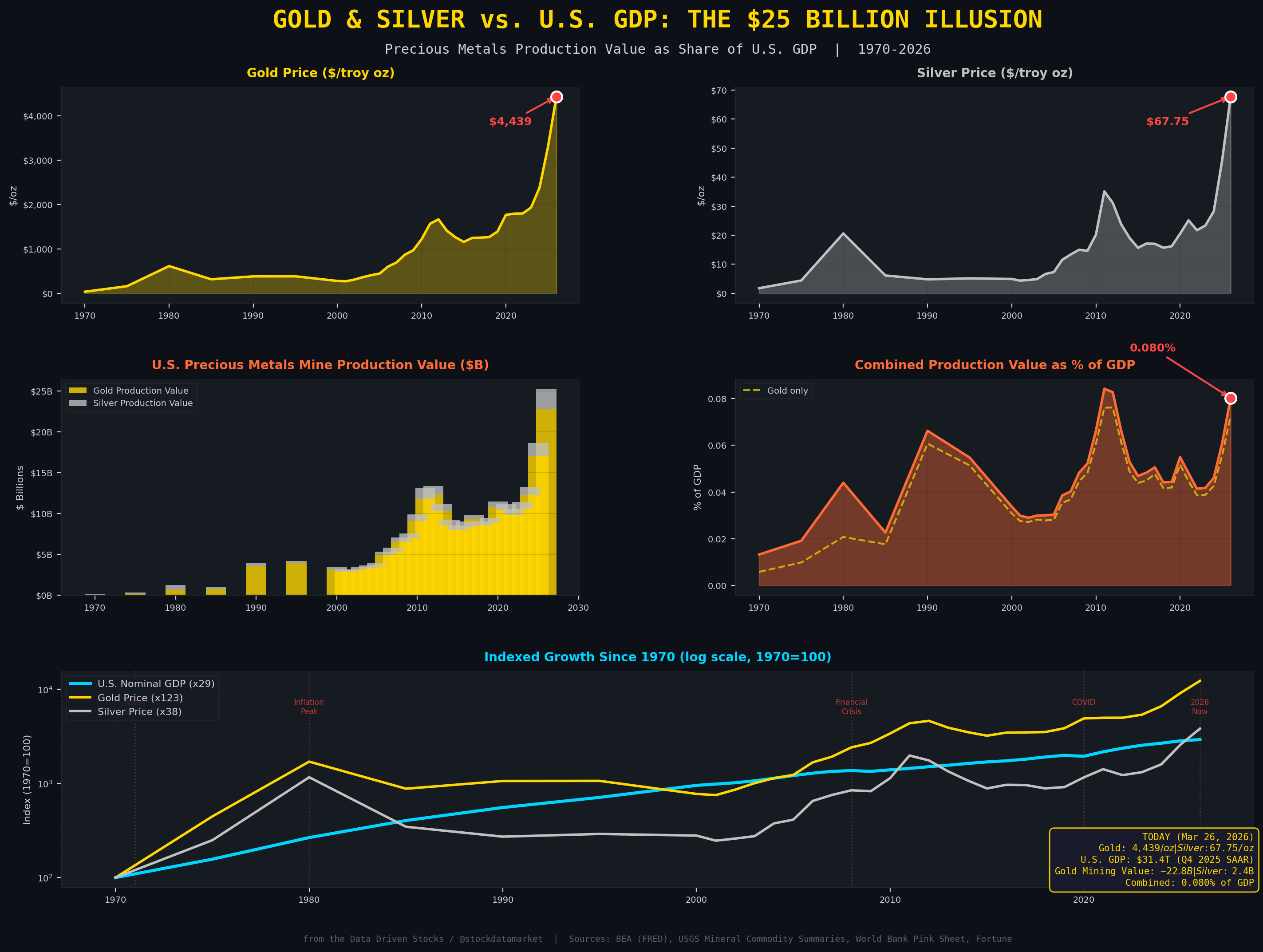

Gold at $4,400 and Silver at $68: Why Precious Metals Still Barely Move the Needle on U.S. GDP in 2026

The $25 billion illusion - how record-high gold and silver prices translate to less than 0.08% of America’s $31.4 trillion economy, and why that number is important than you think