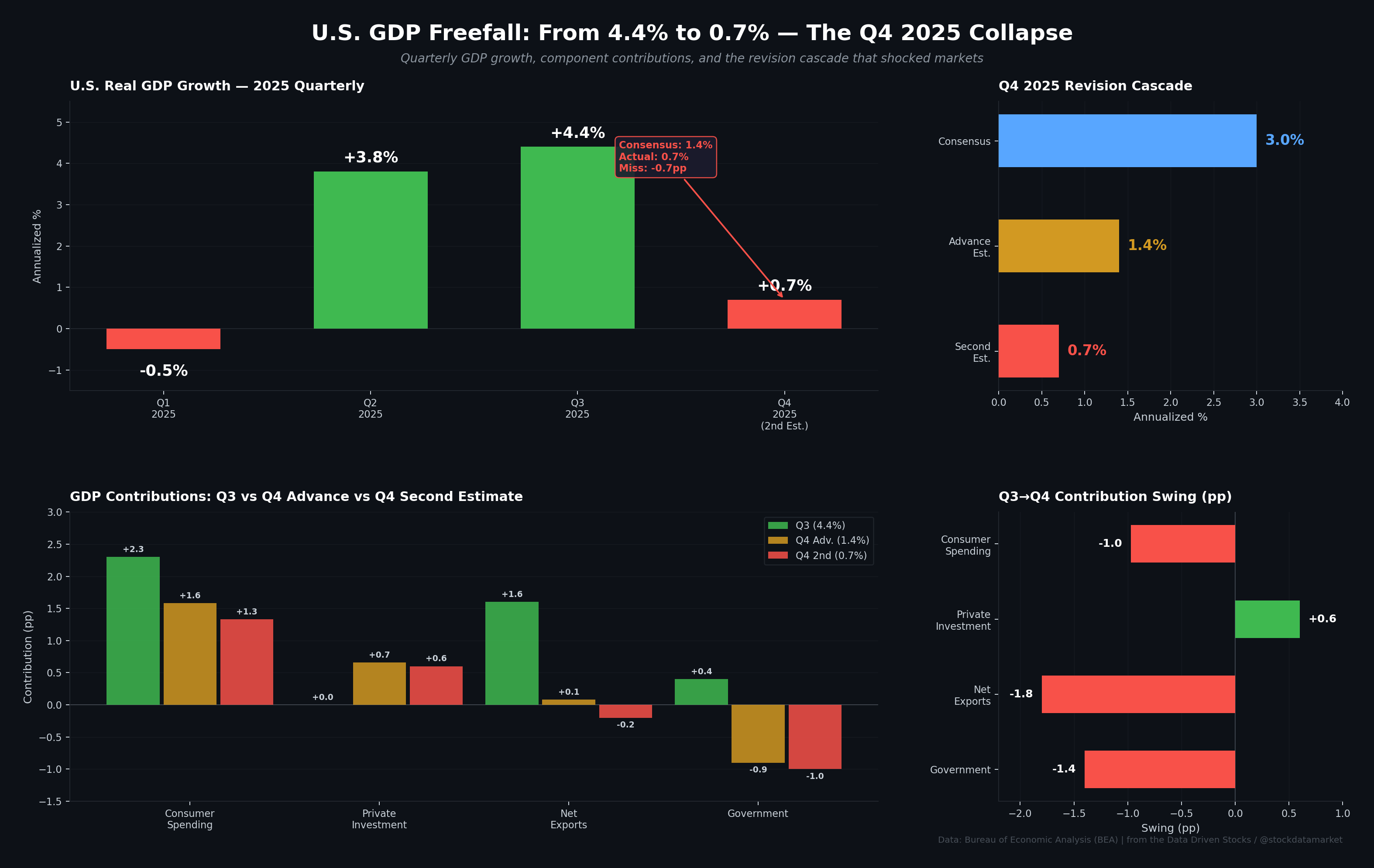

U.S. GDP growth collapsed from 4.4% in Q3 to just 0.7% in Q4 2025 — a 3.7 percentage point swing driven by a government shutdown, evaporating exports, and a cooling consumer. Data: Bureau of Economic…

Continue reading this post for free, courtesy of Data Driven Stocks.