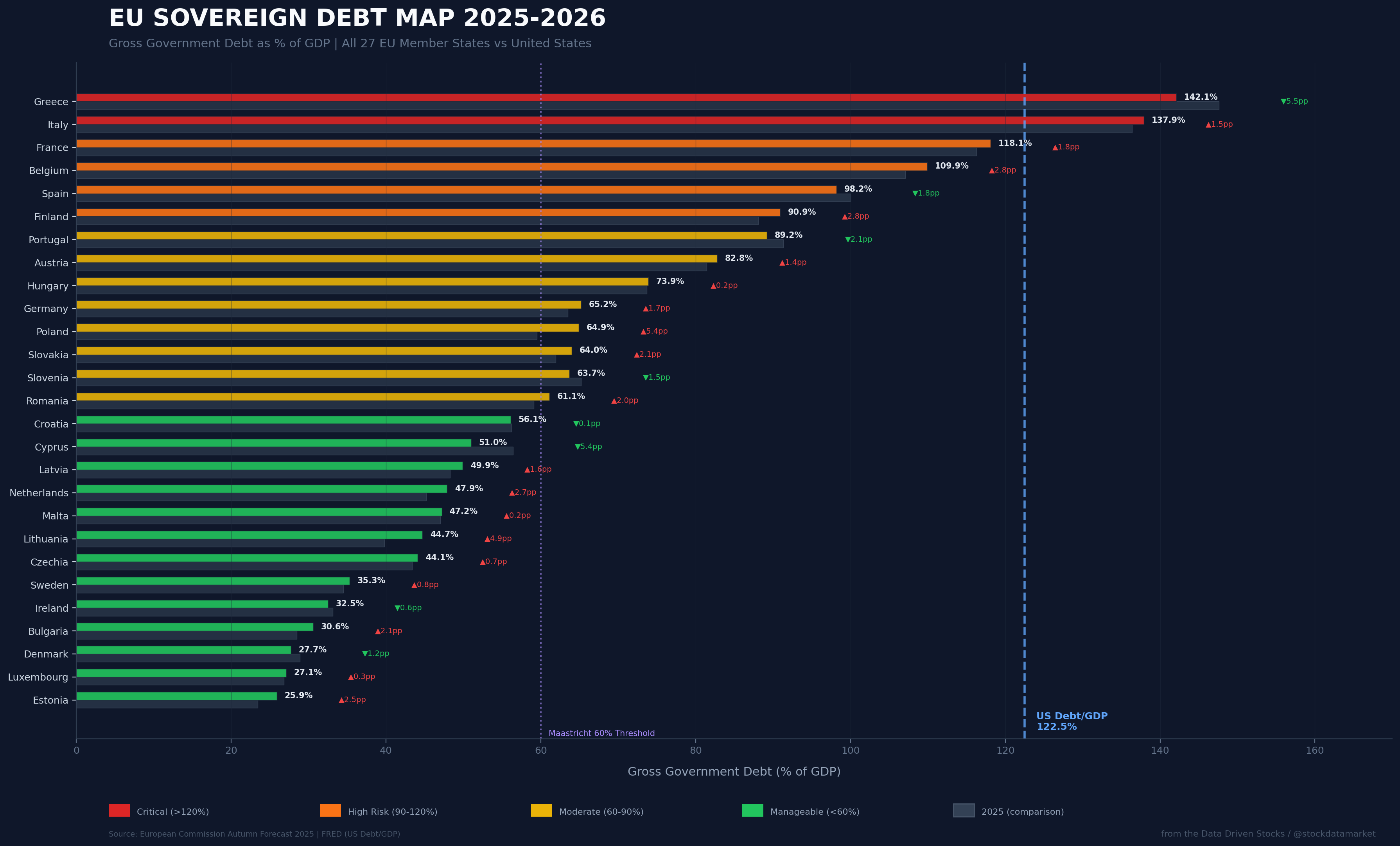

Europe’s $14 Trillion Debt Bomb Is Ticking - And the Iran War Just Lit the FuseThe EU carries more debt than ever before, bond yields are spiking, and a full-blown energy shock just slammed into the continent. Data Driven StocksMar 30, 2026∙ Paid2ShareEU Sovereign Debt Map 2025-2026 - All 27 member states ranked by Debt/GDP with year-over-year change and US comparison line. Data: European Commission Autumn Forecast 2025, FRED.Continue reading this post for free, courtesy of Data Driven Stocks.Claim my free postOr purchase a paid subscription.PreviousNext