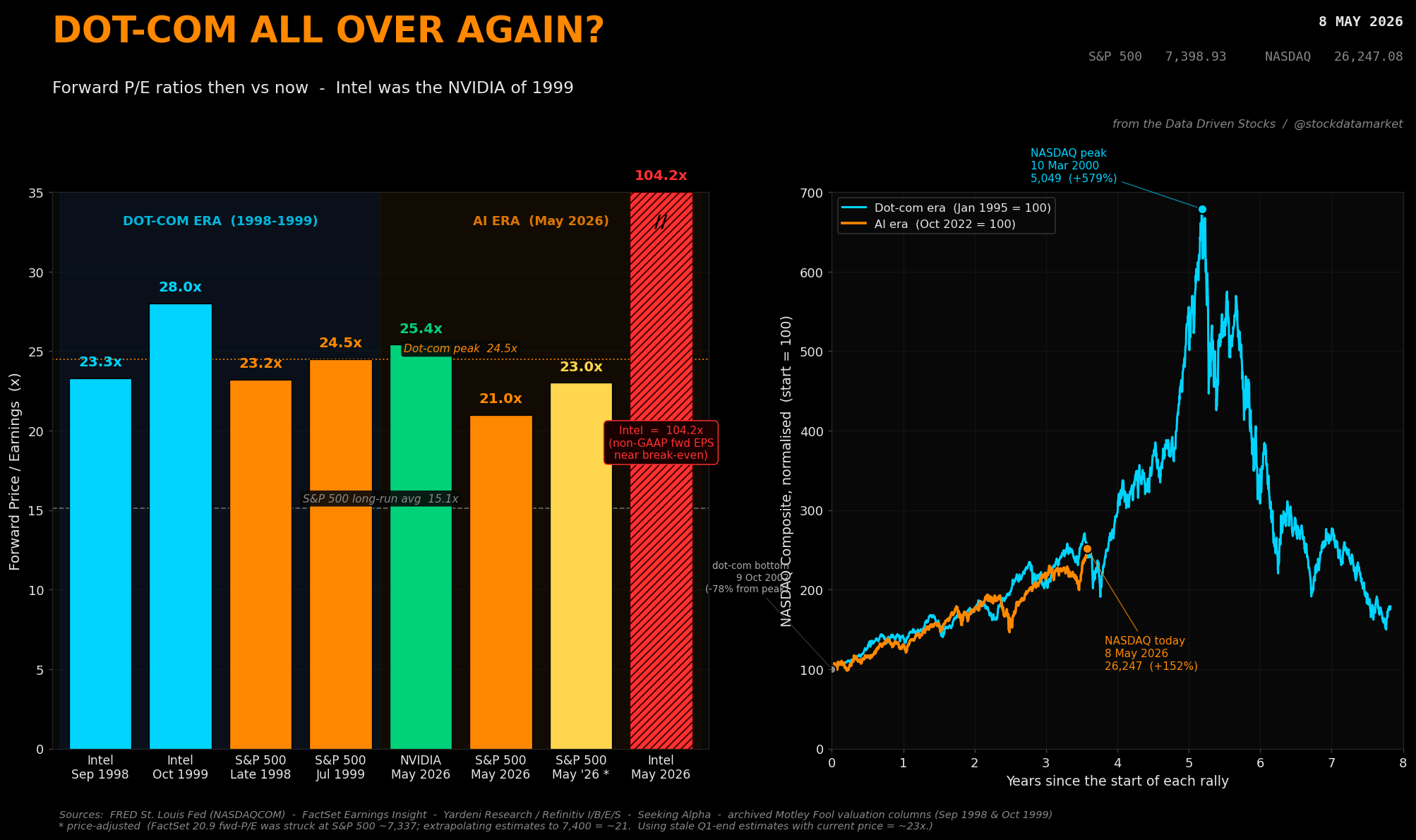

Forward P/E ratios then vs now. Intel was the NVIDIA of 1999. The May 2026 NVIDIA reading sits one rounding error away from the S&P 500’s all-time forward-earnings peak of July 1999.

On April 24, 2026…

Continue reading this post for free, courtesy of Data Driven Stocks.