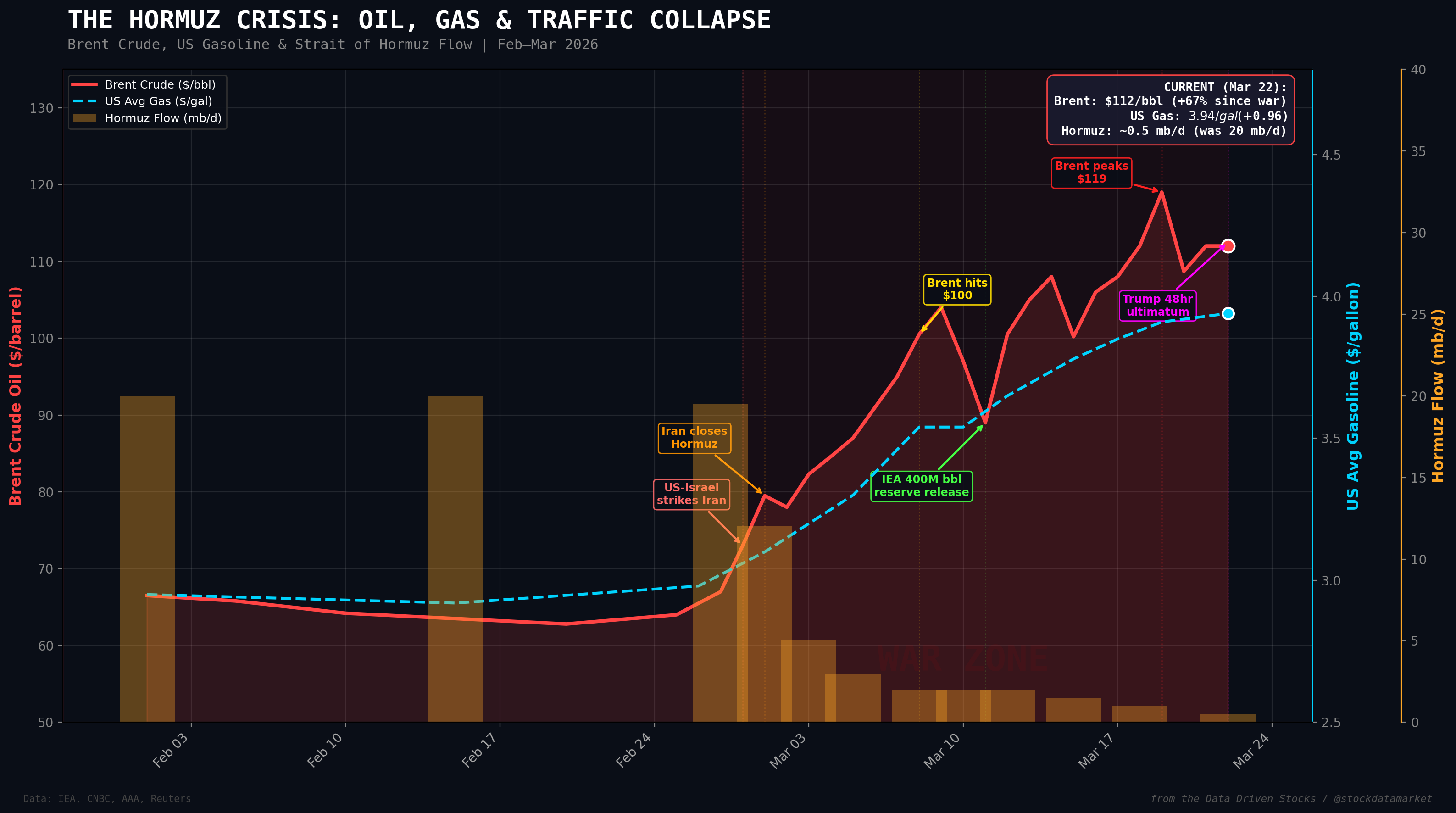

The Hormuz Crisis in one chart — Brent crude, US gasoline, and Strait traffic all moving in the worst possible directions since Feb 28. Data: IEA, CNBC, AAA, Reuters. Chart by Data Driven Stocks / @s…

Continue reading this post for free, courtesy of Data Driven Stocks.