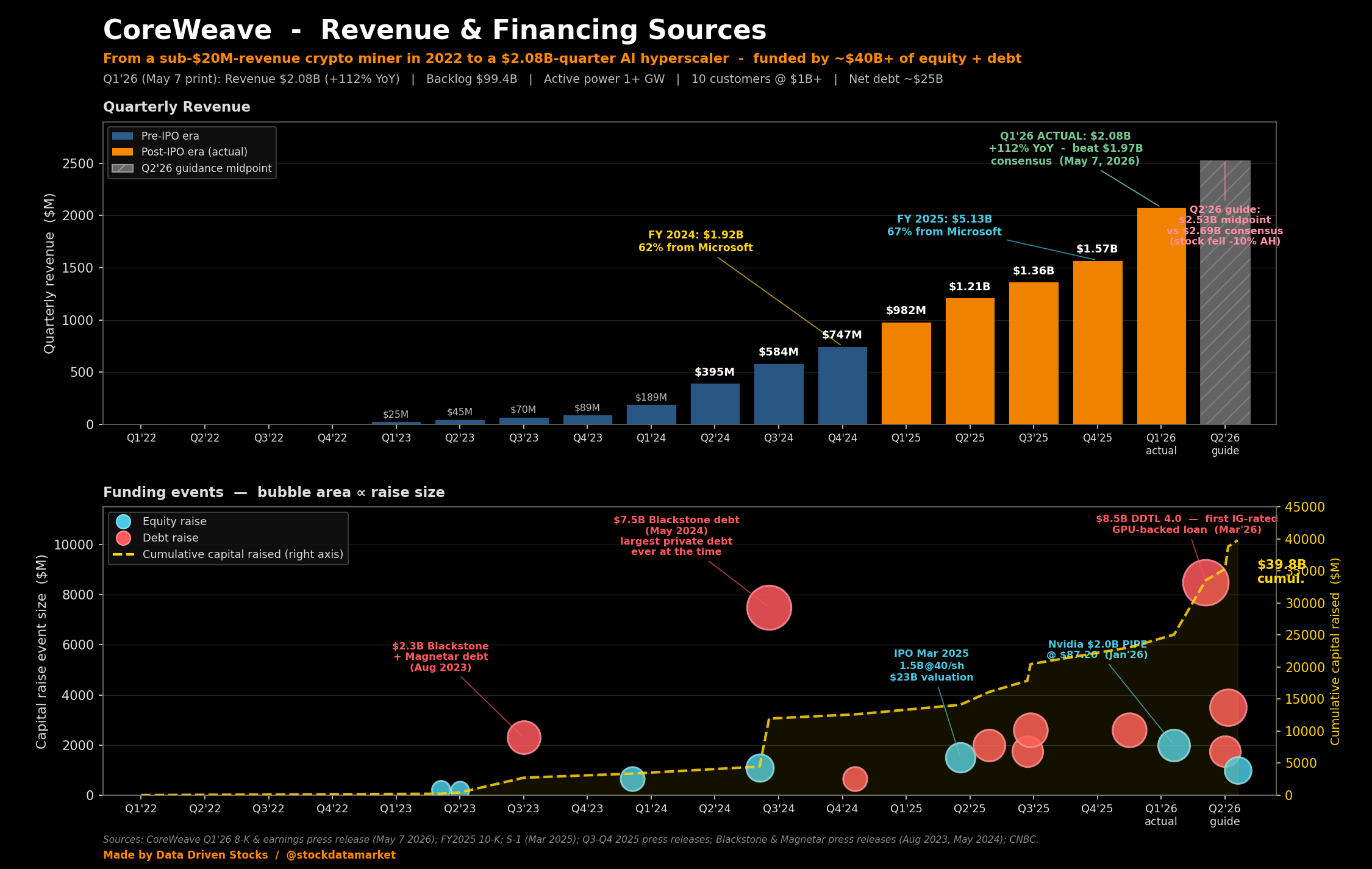

CoreWeave revenue by quarter (top panel) updated through the May 7, 2026 print, alongside Q2 2026 guidance midpoint as a hatched grey bar; financing events on the bottom panel with cumulative capital…

Continue reading this post for free, courtesy of Data Driven Stocks.