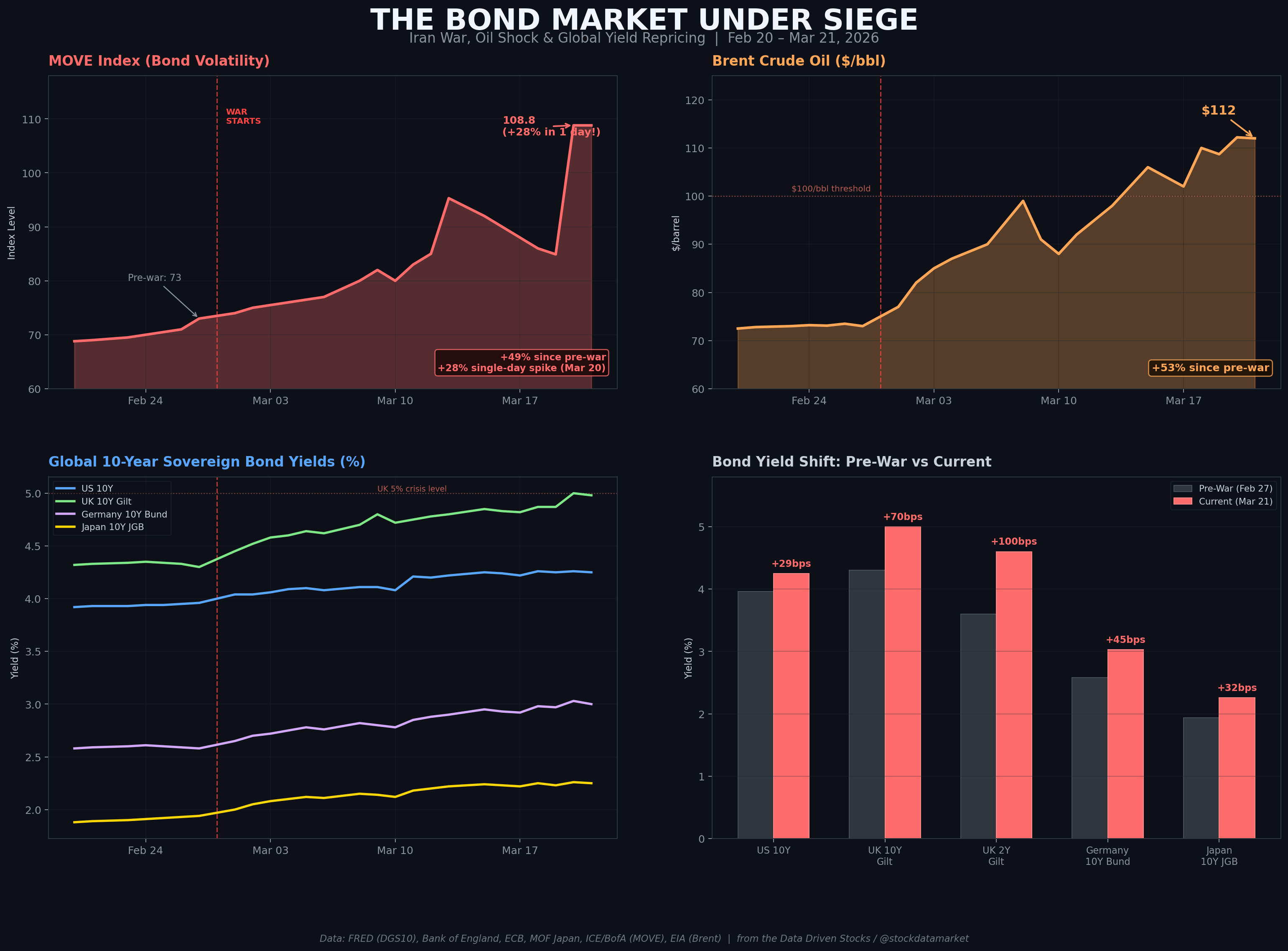

Bond Market Is Eroding, MOVE Index Is Exploding, and the War in Iran Makes It Much Worse

Three weeks into the Iran war, global sovereign debt is repricing at a pace not seen since the 2022 inflation shock. The safe-haven playbook is broken. Here’s what the data says.

If you’re a bond investor in March 2026, the last three weeks have felt …