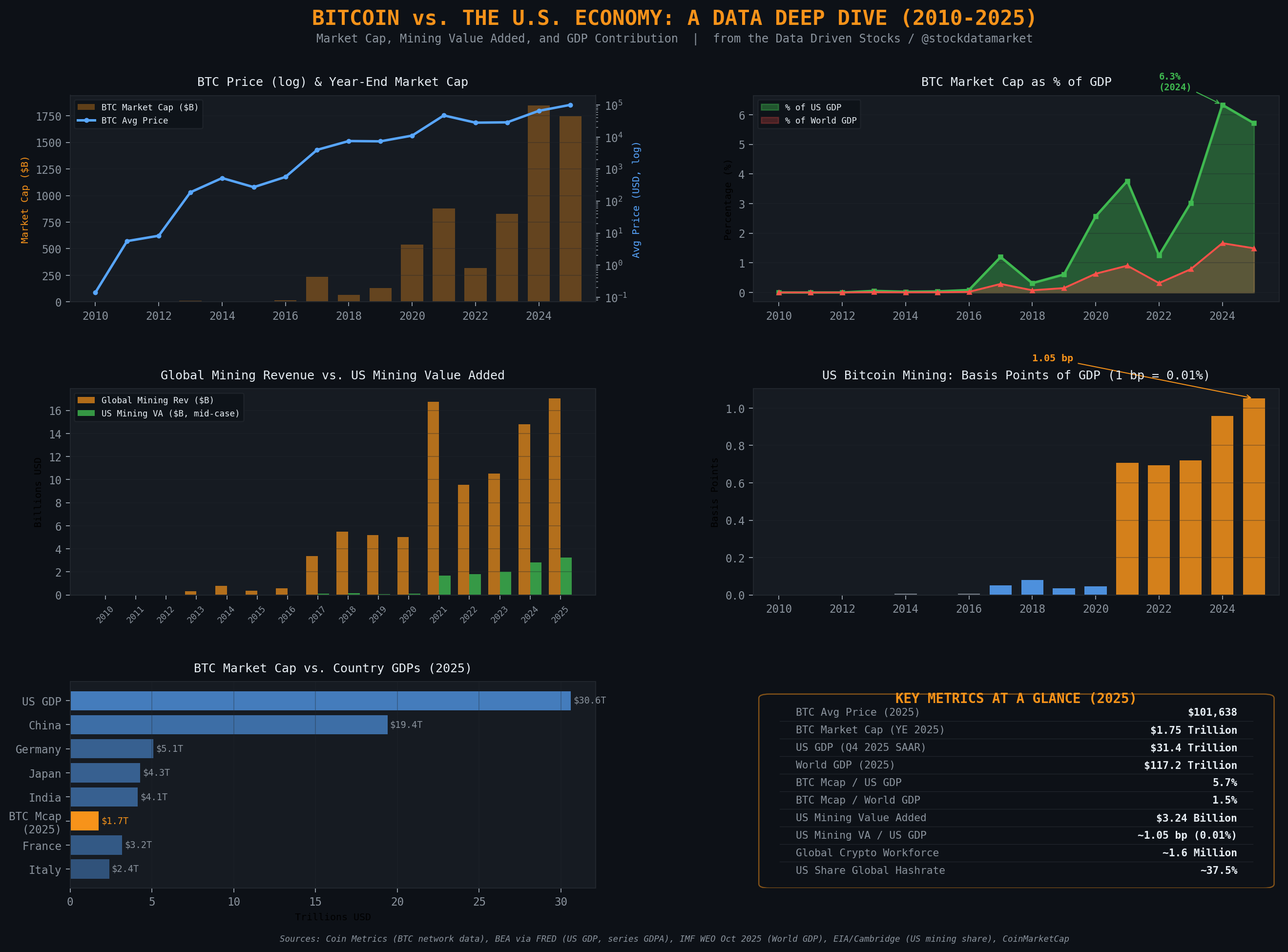

Bitcoin vs. The U.S. Economy: A multi-panel data deep dive covering price, market cap, mining value added, and GDP contribution from 2010 to 2025. from the Data Driven Stocks / @stockdatamarket

Continue reading this post for free, courtesy of Data Driven Stocks.