Are tariffs going to end after the SCOTUS ? What is next? All tariffs gone ? Not really ...

The Supreme Court is about to decide if “emergency” can mean “import tax”. Are all tariffs going to be removed ? Market is going to crash ?

January 14 is shaping up to be one of those dates where macro Twitter / X pretends the world will end at 10:01am ET.

Here’s the real setup. The Supreme Court said it expects to issue rulings on January 14, but it does not say in advance which cases it will decide. One of the biggest cases still pending is the fight over President Trump’s sweeping “emergency” tariffs imposed under IEEPA. It could drop on the 14th… or it could be later.

If the Court nukes the tariffs, it’s not just a trade-policy headline. It’s potentially a refunds-and-revenue story (think: $100B+), an inflation story, and a “how much executive power is too much?” story.

1) Emergency powers vs. the tariff button: the legal knife fight

Tariffs feel like simple policy. Raise a number, imports get pricier, “protect domestic industry,” roll credits.

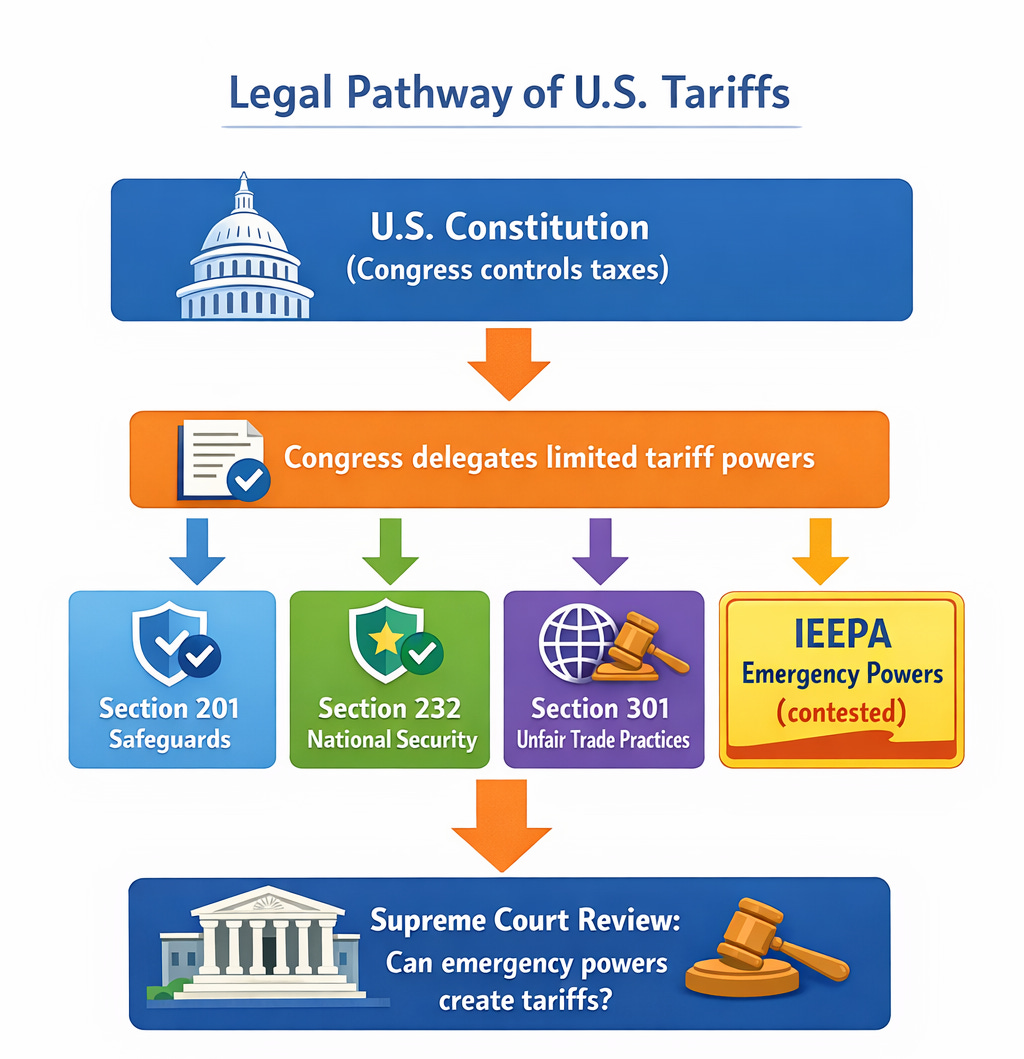

Legally, it’s way messier, because tariffs are basically a tax. In the U.S. system, Congress is supposed to control taxing and trade rules, and then it delegates certain powers to the president through specific statutes. That’s why you keep seeing different “tariff flavors”: Section 201, 232, 301… each has its own rules, process, and limits.

The case sitting at the Supreme Court right now is specifically about IEEPA, the International Emergency Economic Powers Act of 1977. IEEPA is a national-emergency law traditionally used for sanctions and asset freezes, not “tariffs on basically everyone.”

What Trump did under IEEPA

According to the reporting and the court record summaries, Trump used IEEPA to launch two big tariff buckets in 2025.

One bucket is the “trafficking” tariffs, aimed at China, Canada, and Mexico, justified by fentanyl and illicit drugs as the emergency.

The other bucket is the “reciprocal” tariffs, aimed at nearly every trading partner, justified by trade deficits as an “unusual and extraordinary threat.”

Why the courts might wipe them out

Lower courts have already ruled against Trump’s IEEPA tariffs. The Court of International Trade said IEEPA’s language about “regulating importation” does not equal unlimited tariff power, and it also found the trafficking tariffs didn’t properly “deal with” the threat the statute requires.

The administration’s argument is basically: “IEEPA says regulate importation, tariffs regulate importation, therefore tariffs are allowed.” The government also leans on historical precedent like Yoshida (a Nixon-era surcharge case under a related statute) to argue Congress copied language knowing it could support tariffs.

So the Supreme Court decision is not about whether tariffs are “good” or “bad.” It’s about whether Congress clearly gave the president this kind of tariff authority inside IEEPA—and whether “declaring an emergency” can become a workaround for trade laws that have explicit limits.

The key misconception: “Will this ruling delete all Trump tariffs?”

Probably not.

If the Court strikes down the IEEPA tariffs, that hits the big 2025 emergency tariff structure. But other major tariff regimes—like Section 232 (national security) and Section 301 (China unfair trade practices)—sit on different legal foundations and are not automatically erased by an IEEPA ruling.

In fact, the Federal Circuit recently upheld the legality of the big Section 301 “List 3” and “List 4A” China tariffs (the long-running refund litigation). That’s a separate track from the IEEPA case.

2) The tariff map: what’s actually in force right now

There are thousands of individual tariff lines in the Harmonized Tariff Schedule, plus antidumping/countervailing duties (AD/CVD) on specific products. Nobody wants that spreadsheet in a Medium post.

So here’s the practical list: the major programs that materially move costs, margins, and macro.

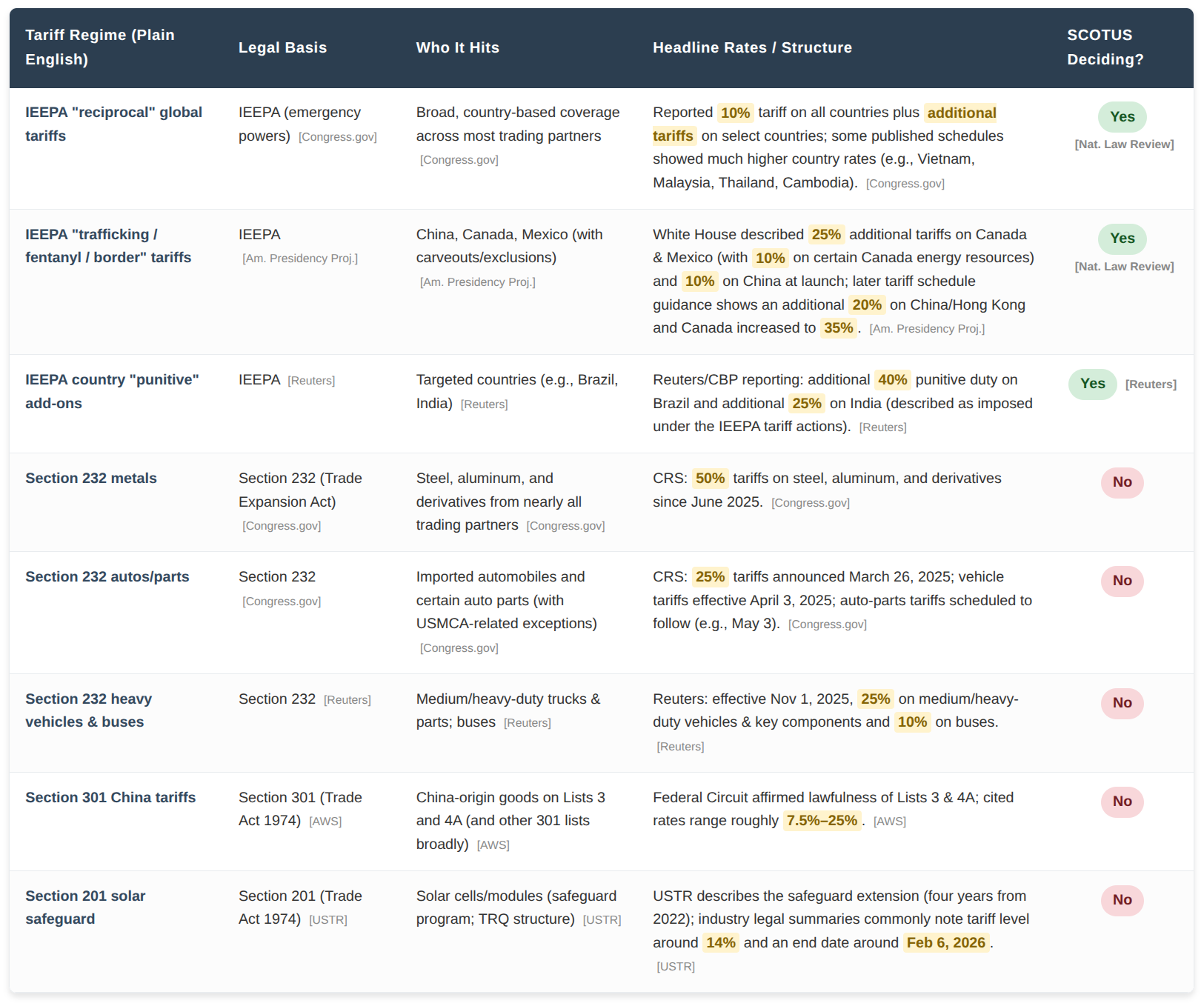

Table: Major U.S. tariff regimes in effect

Now let’s walk through them like a normal person.

“Reciprocal” IEEPA tariffs: the broad blanket

These are the ones that made the headlines because they were aimed at “nearly every foreign trading partner,” with Trump framing trade deficits as the emergency.

They matter less because of the press conference and more because of the boring fine print: exemptions for certain categories, USMCA carveouts, and stacking rules mean the posted rate is not the same as the economy-wide average rate. The Tax Policy Center, for example, estimated the overall average tariff rate “now” around 17% and said removing IEEPA would cut it by about 8 percentage points—meaning the real-world relief is meaningful but not “everything goes to zero.”

Those are the tariffs the Supreme Court could blow up fast if it says IEEPA can’t be used like this.

“Trafficking” IEEPA tariffs: the fentanyl + border emergency bucket

This is the part where tariffs start acting like leverage instead of a trade tool. Trump invoked IEEPA to pressure other countries by raising import taxes, arguing it’s “reasonably related” to stopping fentanyl flows. Challengers argue the statute requires the action to “deal with” the threat, not just create bargaining chips.

On the mechanics: the U.S. tariff schedule itself reflects an IEEPA-based additional 20% on China/Hong Kong goods under a Chapter 99 heading, explicitly stacking “in addition to all other applicable duties,” including Section 301.

Canada is its own saga. The White House said the Canada IEEPA tariff was increased from 25% to 35%, effective August 1, 2025, citing fentanyl and retaliation. Canada has also highlighted that USMCA-qualifying goods got exemptions, which is a huge practical detail because it prevents the tariff from automatically applying to all Canada trade flows.

“Punitive” IEEPA add-ons: Brazil and India

This is basically the IEEPA playbook applied to specific targets. Reuters, citing CBP’s breakdown notes, reported additional 40% on Brazil and 25% on India as separate punitive duties imposed later in 2025.

This matters for markets because these targeted add-ons can hit specific supply chains hard even if the broad “reciprocal” rates get negotiated down.

Section 232 metal tariffs: steel/aluminum as national security

Section 232 is the “national security” lane. It’s been used since 2018 for steel and aluminum, and CRS reports show it was expanded again, including an increase to 50% for most trading partners with some exceptions.

These tariffs are not in the Supreme Court IEEPA case. Even if IEEPA gets cut off, 232 stays unless separately changed.

Section 232 autos: the supply-chain sledgehammer

Autos are politically sensitive and economically huge. CRS notes that 25% tariffs on vehicles and certain parts began in 2025 with carveouts tied to USMCA content rules, and later reporting suggests negotiated frameworks lowered rates for some partners (like Japan and the EU) to around 15%.

Again, not in the IEEPA case. But in the real economy, these are the tariffs that show up in MSRP decisions, dealer inventories, and consumer credit stress.

Section 301: the “China unfair practices” tariffs that refuse to die

Section 301 is the trade enforcement lane. It’s where the big China tariff lists live, and they’ve become sticky across administrations.

The big legal development here is that the Federal Circuit upheld the lawfulness of Section 301 Lists 3 and 4A tariffs in late 2025. So if you’re expecting a Supreme Court decision to erase all Trump-era tariffs, Section 301 is the clearest counterexample: it’s been litigated, and the government largely won.

Even within Section 301, exclusions matter. USTR extended 178 exclusions until November 2026, and Reuters tied that to a broader U.S.-China truce framework.

Section 201 solar: the one with an actual expiration date

This is the tariff program with a calendar countdown. A Federal Register notice explicitly describes the Section 201 solar safeguard as extended through a period that ends February 6, 2026.

CBP quota bulletins show the TRQ structure and the quota period for Feb 7, 2025 through Feb 6, 2026 (including the aggregate quantity level used for administration).

3) So… what are the odds the Supreme Court kills the IEEPA tariffs?

No one knows. If anyone claims they “know,” they’re selling you something.

What we do have are signals.

The first signal is the oral argument vibe. Reporting from the November 5 hearing said both conservative and liberal justices sounded skeptical, pressing the idea that “regulate” isn’t automatically “tax,” and raising separation-of-powers concerns.

The second signal is the market’s attempt to price the outcome. Reuters reported betting-market odds moved against Trump after arguments, with Trump’s chances of prevailing roughly in the 20%–30% range on platforms like Kalshi and Polymarket (methodology and reliability caveats apply, but it’s still a live sentiment gauge).

My non-legal, non-investment take is simple: the base case looks like the Court limits IEEPA for tariffs in some way, because letting the president set import taxes globally with emergency declarations is the kind of power shift that makes justices nervous across ideologies. But the Court could also thread the needle: upholding some narrower “trafficking” pieces while striking or narrowing the “trade deficit = emergency” logic, or dodging the biggest economic shock by narrowing remedies/refunds.

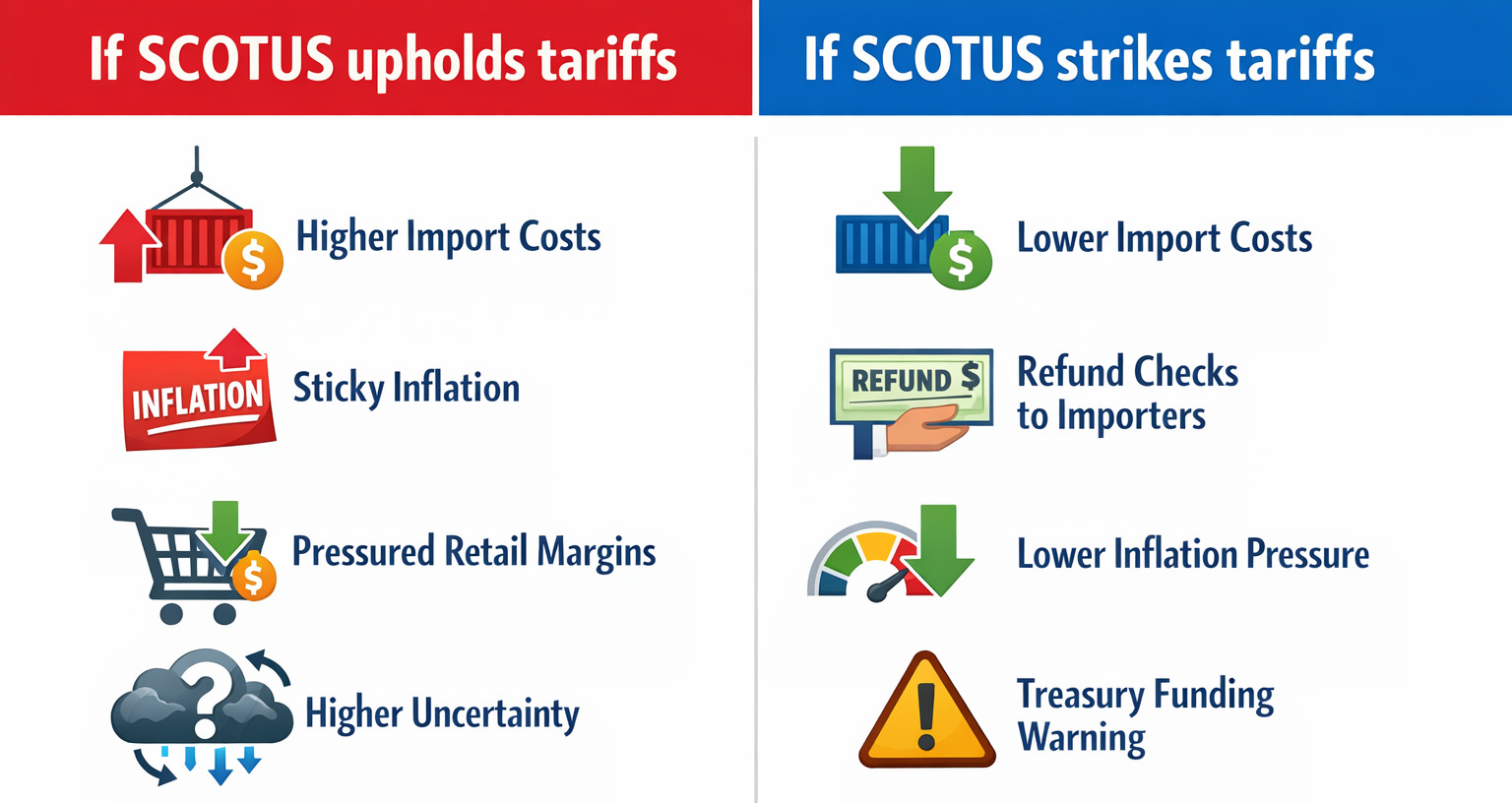

4) If the Court sides with Trump: “Tariffs stay. Inflation stays annoying.”

If the Supreme Court upholds the IEEPA tariffs, it effectively blesses a new macro tool: presidents can turn “national emergency” into a tariff dial.

Macro: higher prices, lower growth, more uncertainty

Economically, tariffs are a border price shock. Research on the 2018–19 tariff hikes found they changed import patterns and prices for affected goods, and studies have argued much of the burden lands on U.S. firms/consumers via higher prices rather than being magically “paid by foreigners.”

Tariffs can hit inflation and growth through multiple channels, and the sign can depend on whether the supply-side cost shock dominates or whether weaker demand dominates. One Fed letter last year lays out exactly that tension: tariffs can raise inflation and unemployment via supply disruptions, but also weaken demand which can damp inflation while raising unemployment.

If you want the cleanest “official” macro warning label: the IMF publicly flagged Trump’s sweeping tariff announcement in 2025 as a significant risk to the global outlook.

Stocks: margin pressure + higher discount rates

Markets already gave us a mini preview. Reuters noted stocks fell nearly 5% when Trump announced tariffs last April, with Treasuries initially reacting like a classic uncertainty shock.

If tariffs persist, the channel for equities is mostly boring and painful: imported inputs cost more, retail goods cost more, consumers get squeezed, and earnings expectations get trimmed. If inflation stays hotter, rates stay higher, and P/E multiples compress.

Some sectors do benefit. Domestic producers protected by tariffs can see pricing power. But “tariffs good for everything” is not how it works in aggregate.

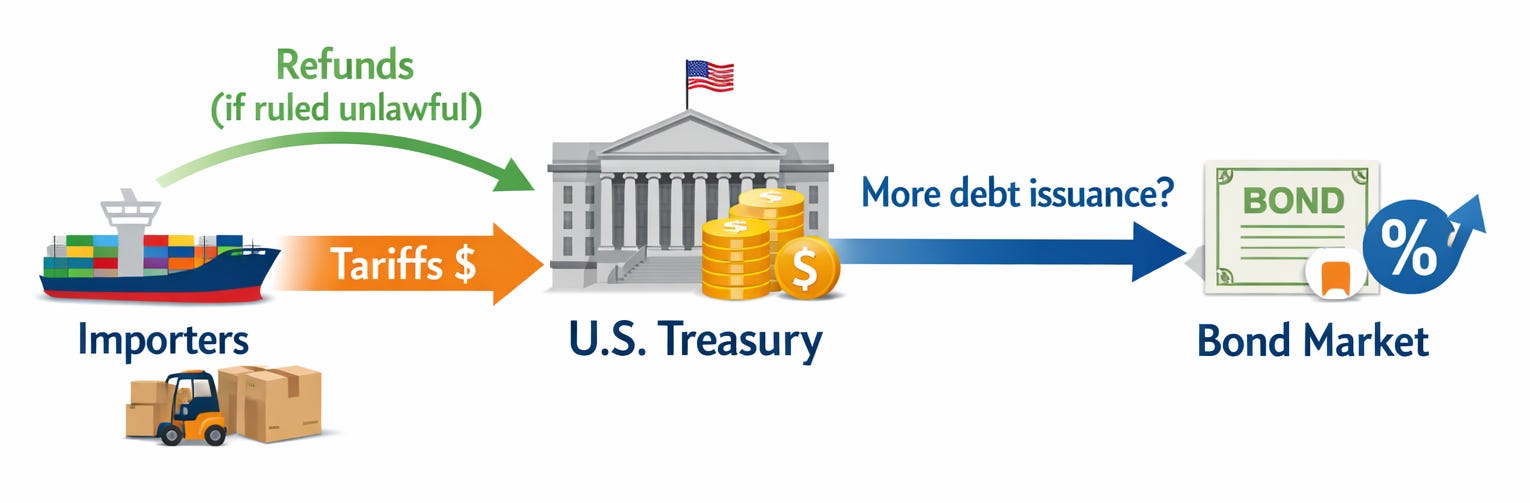

5) If the Court strikes the tariffs: “Relief rally… then the Treasury math shows up”

If the Supreme Court rules the IEEPA tariffs unlawful, you can get a two-stage reaction.

Stage one is the happy stage: costs drop, uncertainty falls, and markets breathe.

Stage two is the spreadsheet stage: refunds, revenue loss, and the government’s financing needs.

The refunds: real money, real fast

CBP’s own tallies (reported by Reuters) put IEEPA-tariff assessments at more than $133.5 billion through mid-December 2025 that could be at risk of refunds depending on how the Court rules and how remedies are handled.

Reuters also reported investor chatter that refunds could mean an inflow of $150B–$200B to importers over the coming months if refunds are required (again: not guaranteed).

That is an immediate, mechanical boost to the balance sheets of tariff-paying importers. Think retail, consumer goods, and electronics—exactly the sectors Reuters quoted strategists calling out.

The revenue hole: not the whole budget, but not nothing

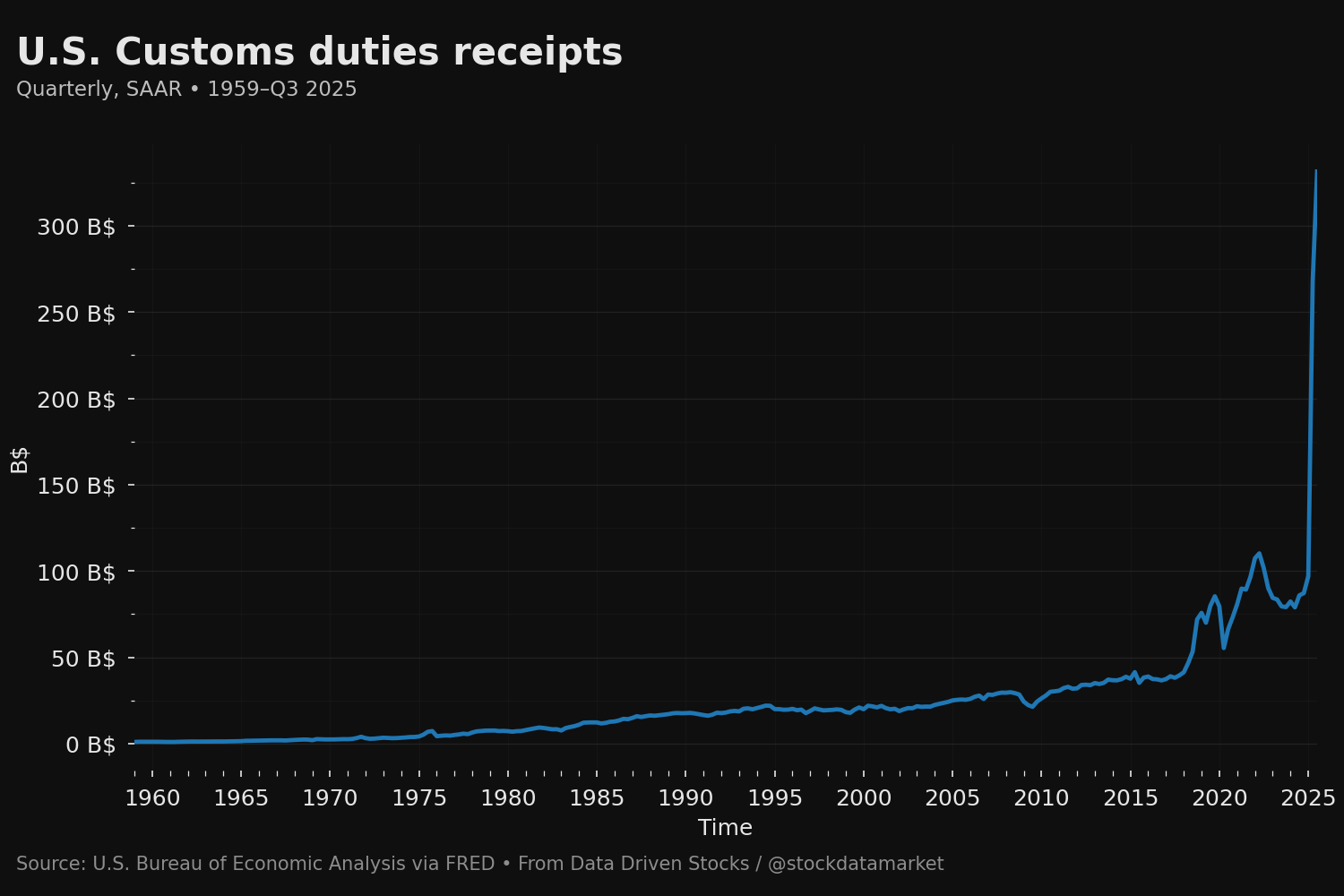

Reuters reported net customs duties hit a record $195 billion in fiscal 2025, with monthly receipts in the “low $30 billion” range afterward.

So yes, tariffs are still small relative to total federal revenue. But in a world where deficits and auction demand matter daily, losing tens or hundreds of billions is not a rounding error.

Liquidity and Treasuries: the weird part

Here’s the key mental model.

When tariffs are collected, cash moves from private-sector importers to the Treasury. If tariffs are reversed, that cash either never leaves (future relief) or comes back (refunds). That’s private-sector liquidity-positive.

But if the government loses tariff revenue and/or pays refunds, it might have to finance that gap. More borrowing can mean more Treasury issuance, which can put upward pressure on yields—exactly the “fiscal fallout” angle Reuters quoted investors discussing.

So you can absolutely get the paradox headline: “Tariff repeal is good for the economy” and “Tariff repeal pushes yields higher” happening in the same week, depending on what dominates: lower inflation expectations vs higher issuance expectations.

Also, even if SCOTUS strikes down IEEPA tariffs, it doesn’t mean the White House runs out of moves. Reuters quoted Nomura’s David Seif saying the administration could turn to other legal routes and still end up with a tariff regime that looks similar by end of 2026 (likely at lower rates). The Tax Policy Center highlighted Section 122 as one possible fallback with a 15% cap and a 150-day time limit unless Congress extends it.