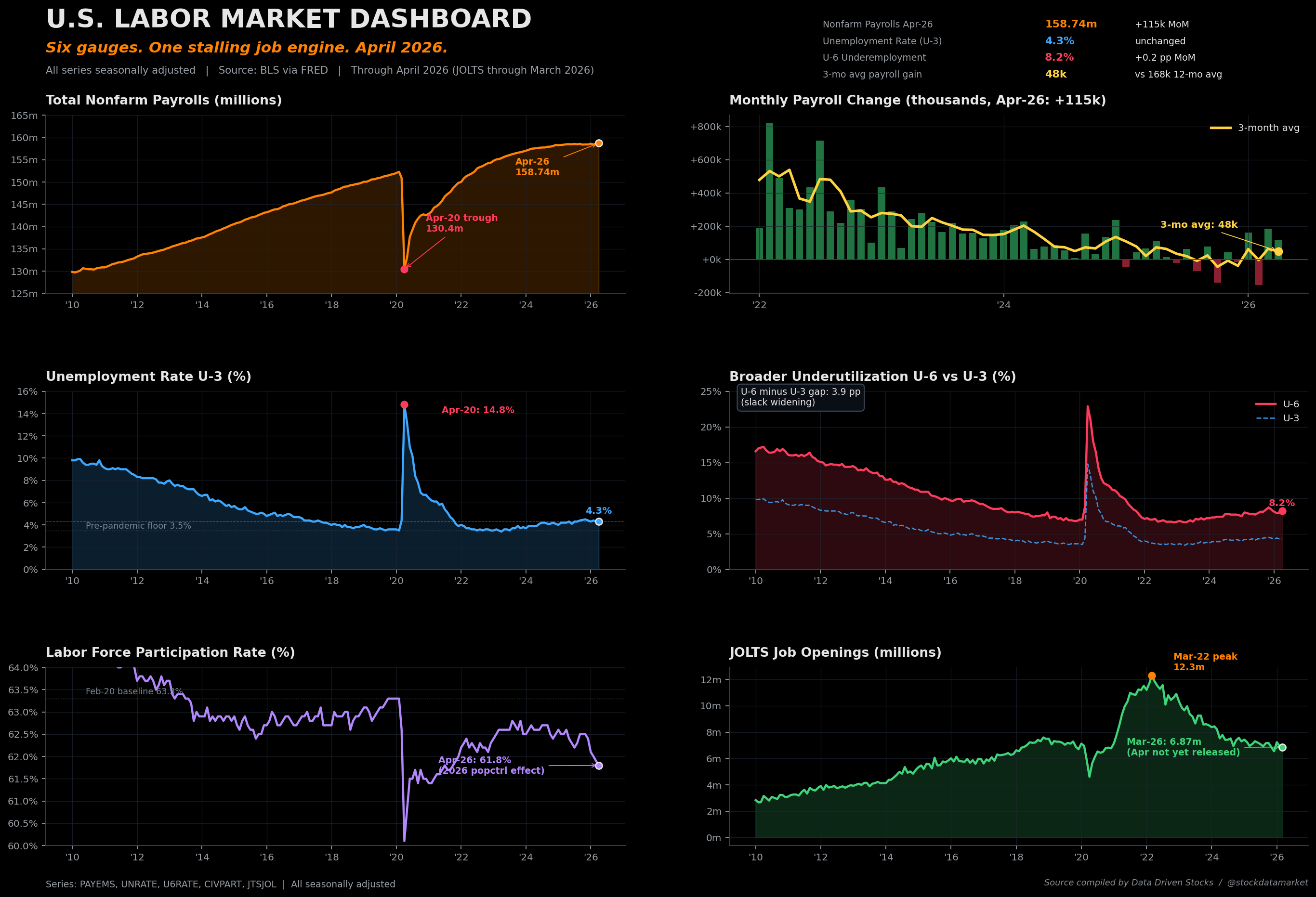

America’s Job Engine Is Quietly Stalling: Inside the April 2026 Payroll Report Wall Street Is Sleepwalking Past

America’s Job Engine Is Quietly Stalling: Inside the April 2026 Payroll Report Wall Street Is Sleepwalking Past. So the job reports are as always rigged