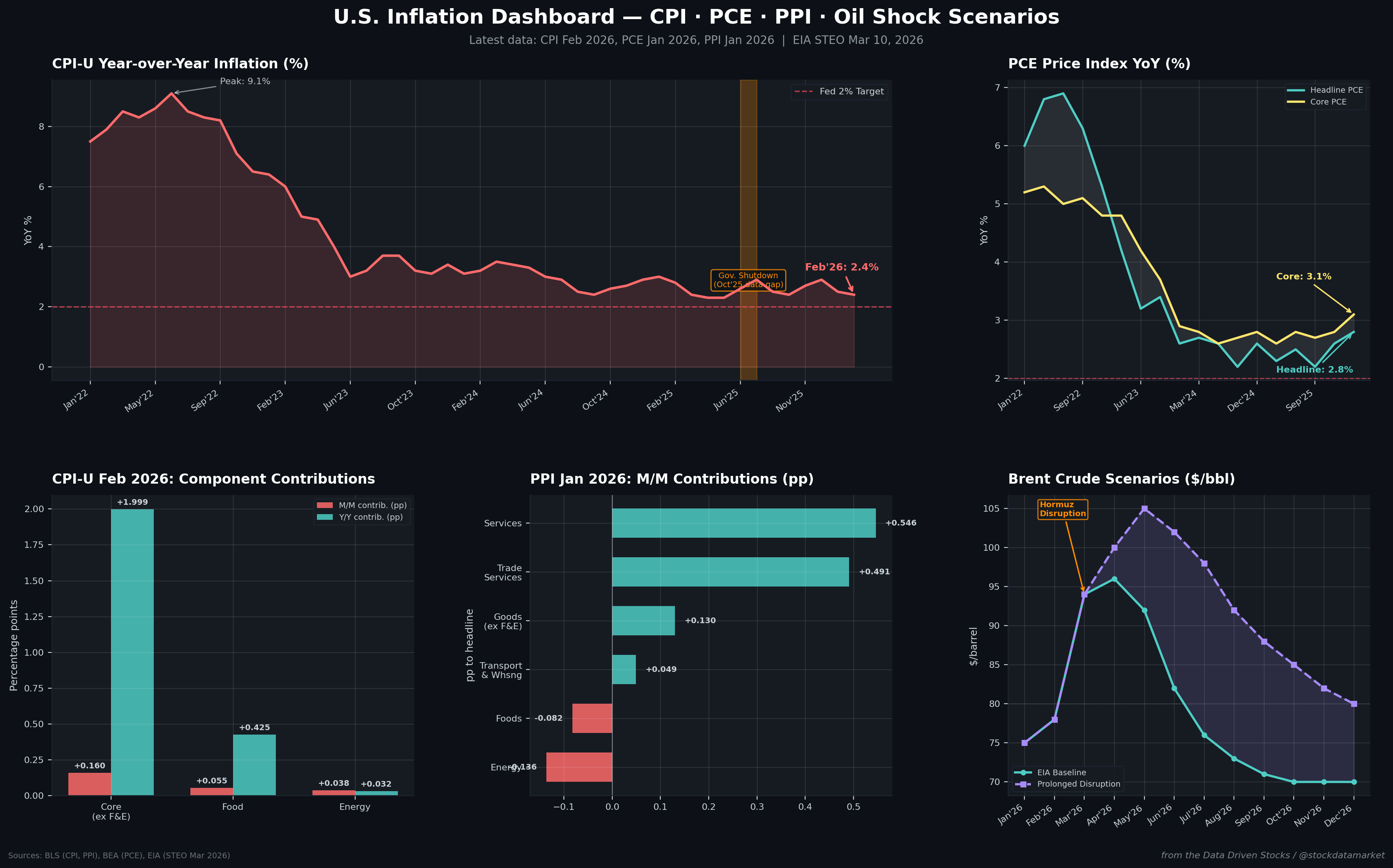

U.S. Inflation Dashboard — A multi-panel view of CPI, PCE, PPI, and Brent crude oil shock scenarios as of March 2026. The disinflation story everyone was celebrating in late 2024 has quietly reversed…

Continue reading this post for free, courtesy of Data Driven Stocks.