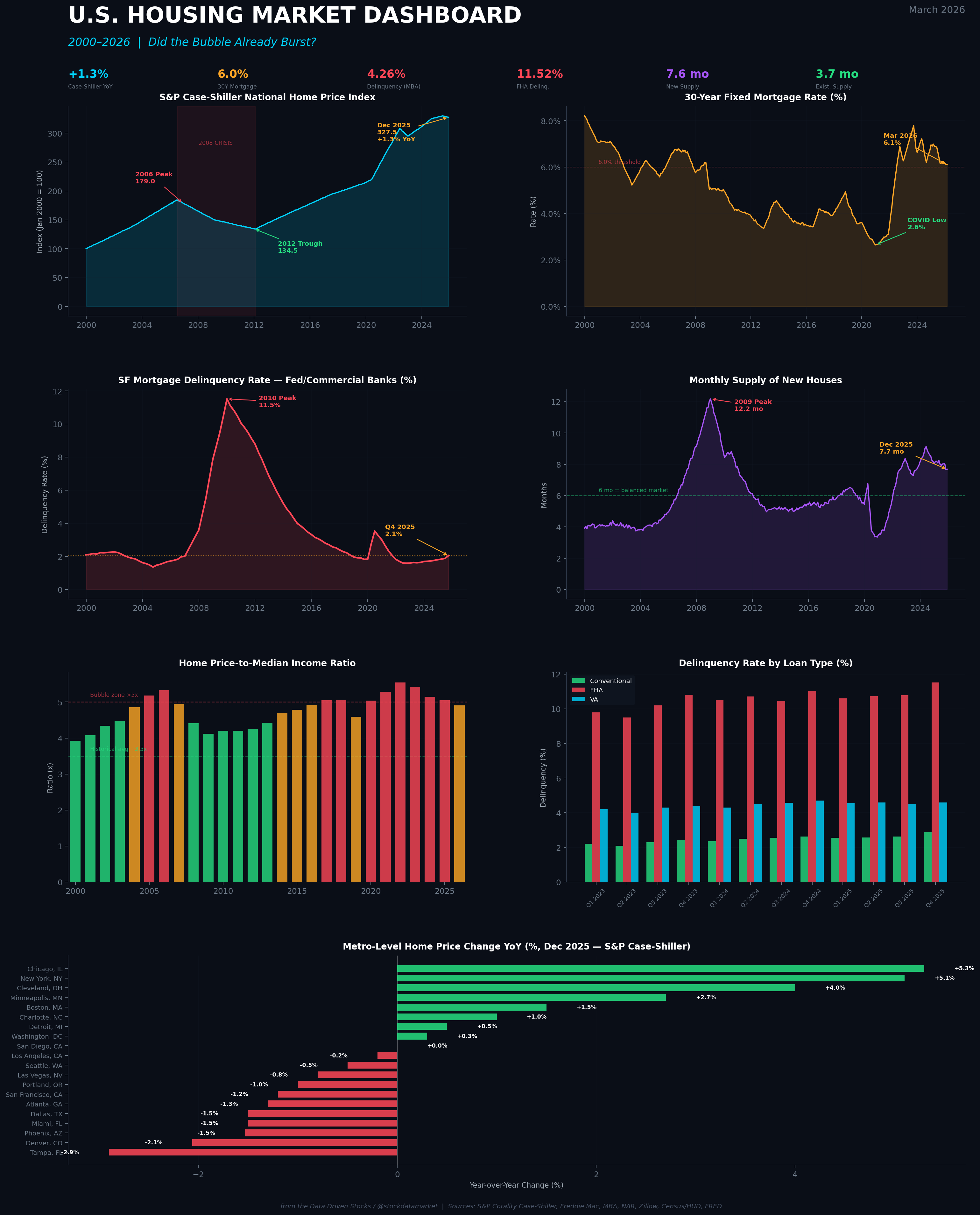

U.S. Housing Market Dashboard (2000–2026) — Six critical metrics at a glance: Case-Shiller home prices, mortgage rates, delinquency rates, FHA stress signals, new home supply, and metro-level price d…

Continue reading this post for free, courtesy of Data Driven Stocks.