2008 vs 2026: Is the U.S. Housing Market Heading for a Repeat — Or Is This Something Else Entirely?

Mortgage delinquencies, homeowner equity, subprime exposure, and metro-level divergence — the data tells a story most headlines are missing.

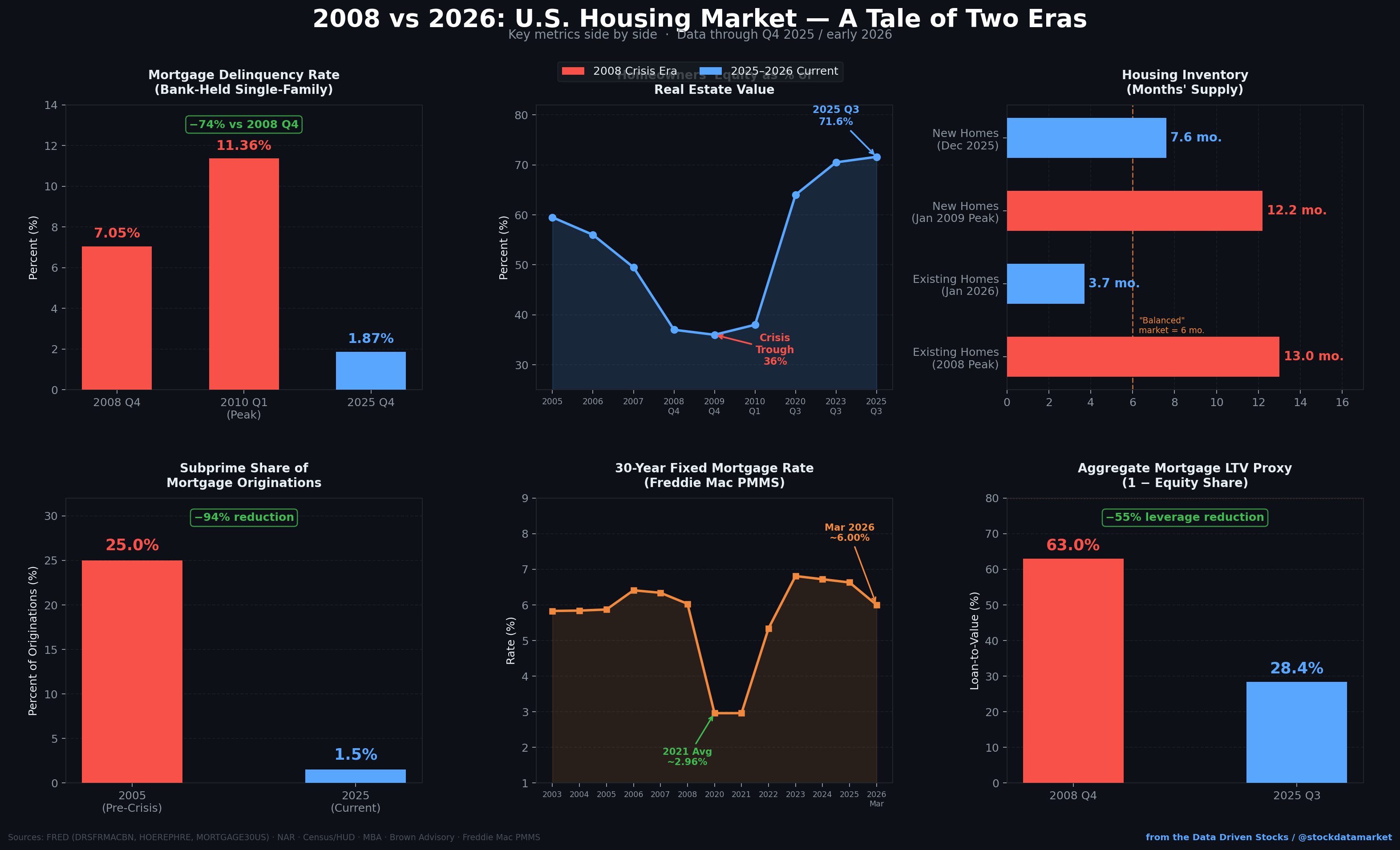

Every time the housing marke…