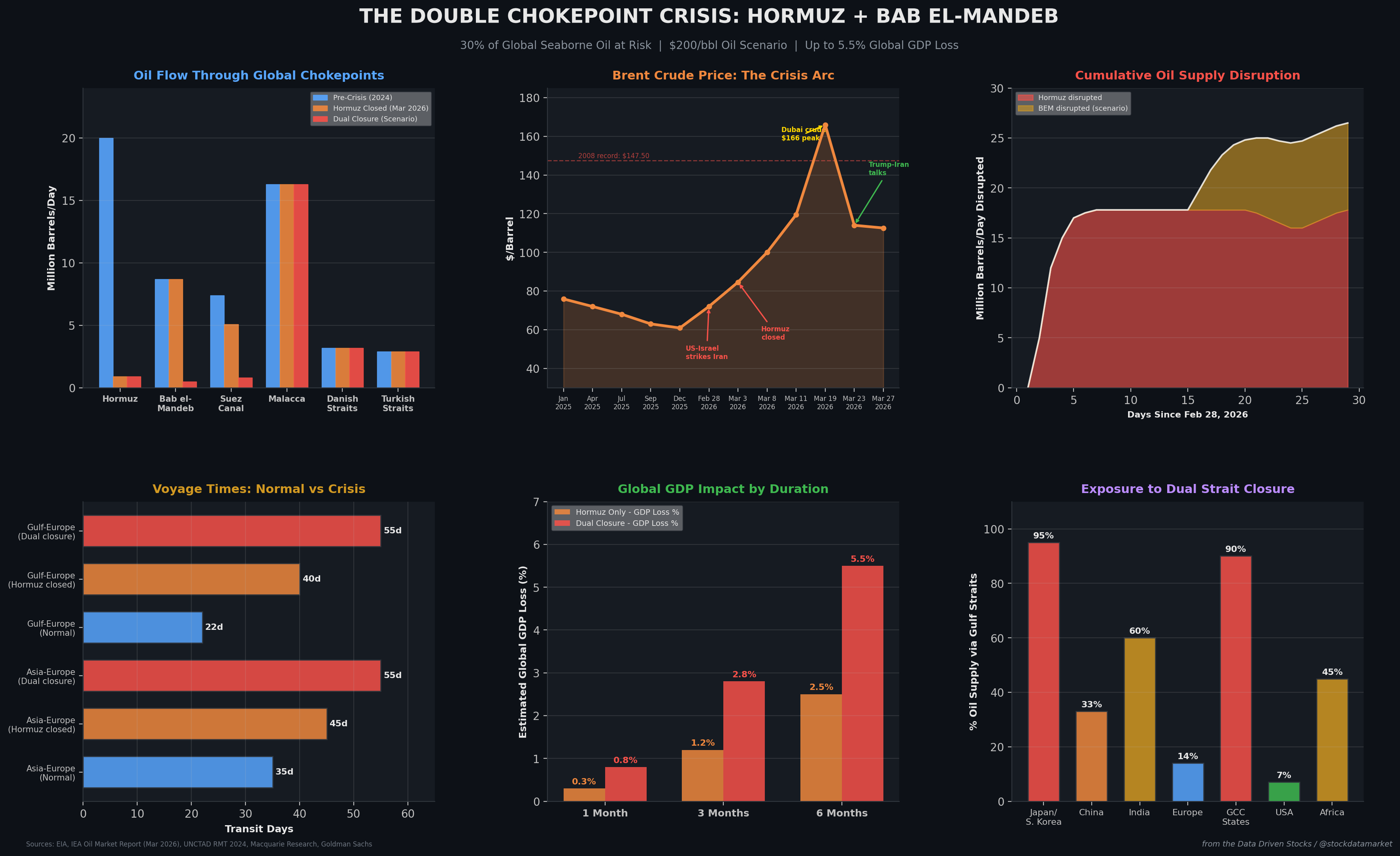

The full picture: six panels showing the data behind the worst-case scenario for global energy. Oil flows, prices, supply disruption, transit times, GDP impact, and regional exposure - all in one das…

Continue reading this post for free, courtesy of Data Driven Stocks.