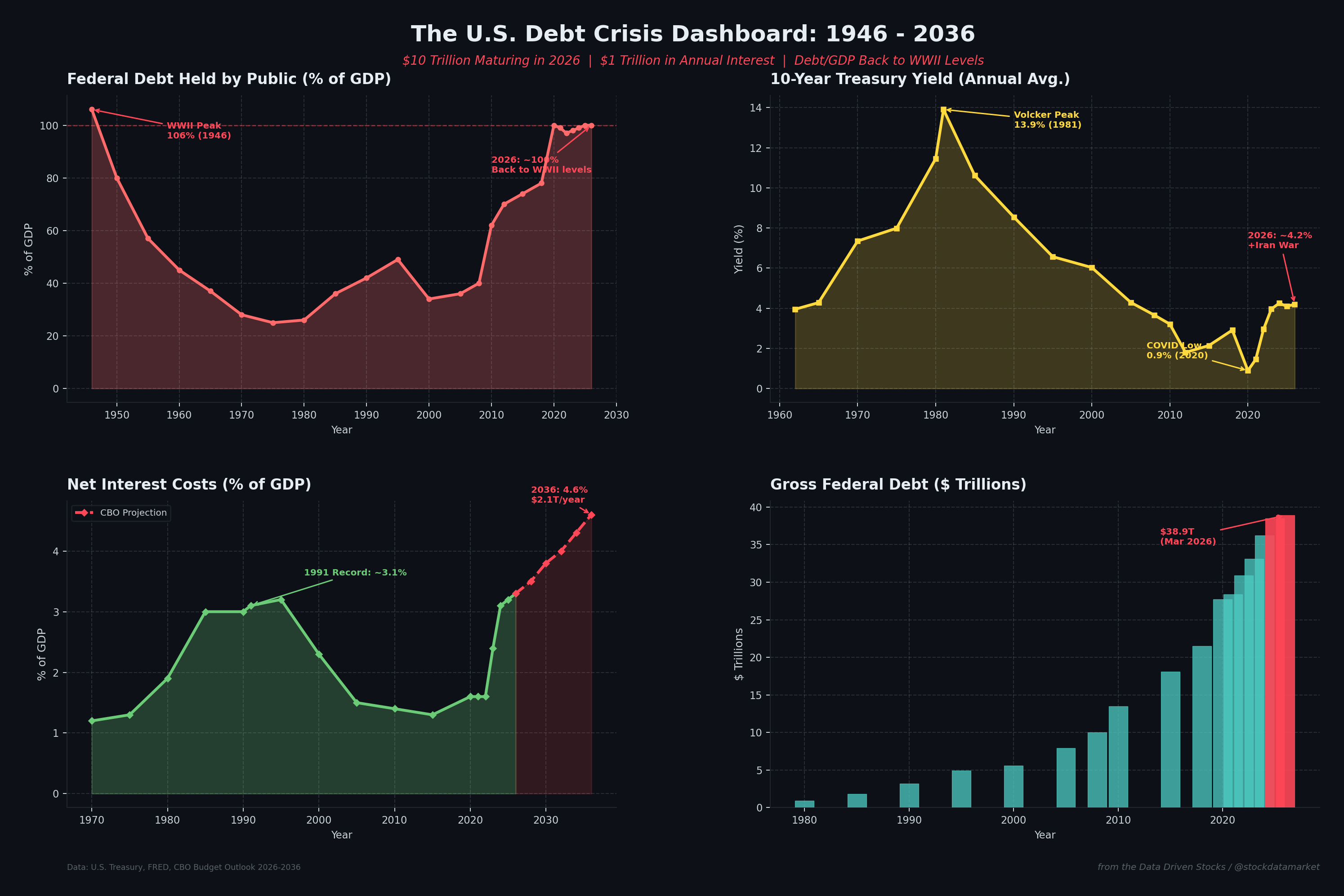

The U.S. Debt Crisis Dashboard: Four decades of compounding fiscal risk converging in 2026. Debt-to-GDP is back at WWII levels while interest costs are approaching all-time highs as a share of GDP. D…

Continue reading this post for free, courtesy of Data Driven Stocks.